Strategic Position of Bank of America

Info: 3585 words (14 pages) Dissertation

Published: 2nd Sep 2021

Tagged: FinanceBusiness Analysis

1. Executive Summary

The Bank of America over the years has been the subject of criticism and scrutiny. With reports of negative income and a 48% decline in stock price. (Dhulekar, Hensaw and Levy, 2013, p. 9).

The Bank of America is facing strategic challenges. To deal with high exposure to mortgage related losses, lawsuits and the slow recovery from the USA economy it needs to position its self for survival (Dhulekar, Hensaw and Levy, 2013, p. 9). Management needs to fully recover their financial position as of before the recession occurred in order to compete against the major competitors who have already financed and paid off their TARP. Management also need to understand the effectiveness to continue merging or acquiring other banks including expanding into other locations given that their financial recovery is slow.(Milner et al., 2013)

Given its depths and complexity of its problems, the scope of this analysis focuses on business segments and where the Bank of America can make changes to defend its strategic position (Dhulekar, Hensaw and Levy, 2013, p. 9).

The Bank of America can make changes to defend its strategic position, but it’s needs to understand its competitive markets and strategic segments and how best to position itself for recovery.

In order for the Bank of America to defend it’s strategic position, two strategic options have been proposed for consideration that can assist and stabilise profits and repair the bank’s mortgage lending investment. ( Dhulekar, Hensaw and Levy, 2013, p.9)

Option 1. Diversification

Acquire new products to offer its customer in order to differentiate from its competitors and earn new market shares and grow the market.

Option 2 Global expansion

The Bank of America can easily spread their activities outside of the United States of America (USA) and grown in the market. They can achieve this by developing products, services with foreign banks and achieve better margins in emerging countries, whereby benefiting from economies of scale, there are fewer competitors and taxes.

In addition to the above, the Bank of America needs to put more focus on mobile banking because they are good at it. Emerging countries have trouble accessing banks and agencies, so mobile banking such as Bank of America is very desired by customers.

2. Identification of Key Strategic Issues and Problems

The Bank of America needs to understand: (Milner et al., 2013)

- Where is the bank heading;

- How to avoid/prevent future exposure during economic crisis;

- Understand what the financial landscape will look like when the economy recovers;

- Where will the bank’s opportunity lie; and

- How will the bank position its self strategically to complete successfully and grow?

Political: Bank of America faces pressure of paying back the Federal Reserve TARP funds following a bail out during the financial crisis (Dhulekar, Hensaw and Levy, 2013, p.14)

Economic: Unemployment in the USA is constant at around 8%-10%. The high unemployment rate will result in high savings, low spending, and low borrowings (Neeraj Dhulekar,Chris Hensaw,Ethan Levy, 2013, p.15)

Technological: Bank of America has the best technological advances in the industry, e.g advanced bill-payment options for customers, apps for smartphones, advanced ATM technology allowing customers to deposit without envelopes (Dhulekar, Hensaw and Levy, 2013, p.15)

Legal: Bank of America faced investigations from the Securities and Exchange Commission (SEC) of the large bonus paid at Merrill Lynch, which upset their shareholders. A law suit settlement was reached to shareholders in the amount of $150 million (Dhulekar, Hensaw and Levy, 2013, p. 15)

Its main stakeholders are investors, shareholders and its customer base (depositors). However, its biggest financial revenue and profit takings come from mortgage loans to investors making it the largest mortgage provider in the USA following the acquisition of Countrywide Financial in 2007. A wrong direction in management could potentially increase in debt and have a ripple effect on the USA economy.

Management needs to fully recover their financial position as of before the recession occurred in order to compete against the major competitors who have already financed and paid off their TARP. Management also need to understand the effectiveness to continue merging or acquiring other banks including expanding into other locations given that their financial recovery is slow.

Lessons learned must be a key focus for management and understand where they went wrong in the past, namely:

- Do not overestimate the value of assets;

- Do not loan to households that cannot afford to repay;

- Implement systems to track loans to understand if customers are paying back and do they qualify for loans;

- Build trust with shareholders;

- Understand risk and different country legal systems will be a major factor for success;

- Understand political processes;

3. Diagnosis: Analysis and Evaluation

“Bank of America is the world’s largest bank based in Delaware and operating under USA. federal law with its headquarters based in Charlotte, North Carolina. It serves individual customers, small and middle enterprises, and large corporations in 175 countries. Bank of America business lines includes banking, investing, asset management, and risk management products and services. In United States alone, BOA had 59 million customers served through 6000 retail banking offices, 18000 ATMs, and online banking. As of June 30, 2008 it had total consolidated assets of $ 1.7 trillion, deposits of $ 785 million, and stockholders’ equity of $ 163 billion)” (Yulianto and Adrian, 2017, p.2)

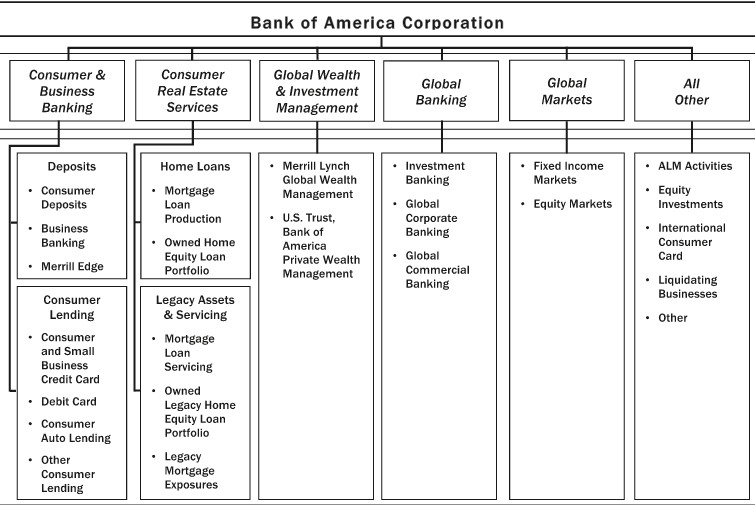

Its product lines consist of:

Fig. 1. Bank of America Corporation Product Lines. (Kilpatrick, 2015)

“Bank of America’s strategy over the past 5 -10 years has been based on expanding its product line by merging and acquiring Countrywide to expand its mortgage portfolio and Merrill Lynch to expand its investment banking customer base and product line. Their strategy has been based on personalisng its products across customer segments as a key driver for positioning. However the financial crisis had impacted and its strategy and put the bank into a complex and costly mess” (Dhulekar, Hensaw, amd Levy, 2013,p. 37)

a) Internal Analysis

I. Business Definition and Mission

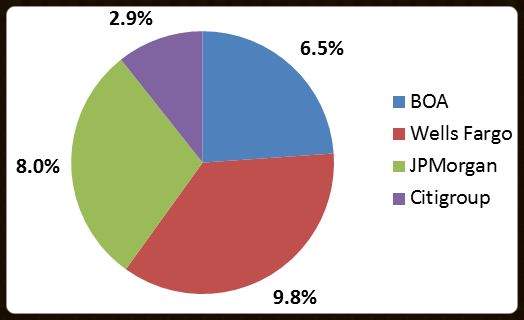

“The Bank of America is a multinational institution which provides it’s customers services in investment and wealth banking. It has a net asset base of $2.2B and ranked the fourth (4) largest bank in the USA with a total capitalization value of over $2B”. (Dhulekar, Hensaw and Levy, 2013, p.9)

Figure 2: Financial market share (Kilpatrick, 2015)

“It main purpose is to make opportunity possible for all customers and client and every stage of their life. Its objectives are to services it three customer group, offer all of its capabilities in the US and investment capabilities world wide” (Kilpatrick, 2015)

II. Bank of America VIRO Analysis

“Bank of America competitive advantage lies in its effective strategic planning process, huge asset base with regards to infrastructure, technology and talent, sophisticated financial technology and IT and its ability to leverage the government relationship for favorable macro- economic conditions”(Kilpatrick, 2015).

| Value | Rare | Difficult to Imitate | Organization | |

| Loyal Customers | √ | x | x | √ |

| Banking Security | √ | x | x | √ |

| Corporate Culture | √ | x | x | √ |

| Online/Mobile Banking | √ | x | x | √ |

| Reward Program | √ | x | x | √ |

| Brand Name | √ | x | x | √ |

| Line of Products | √ | x | x | √ |

| R & D | √ | x | x | √ |

| Reputation | √ | x | x | √ |

| Location | √ | √ | √ | √ |

Figure 3. Bank of America VIRO Analysis (Kilpatrick, 2015)

III. Bank of America Value Chain

(See Exhibit 1)

IV. Strengths and Weakness from Internal Analysis

The key strengths are:

- Significant presence throughout the world

- Asset rich and extensive underwriting portfolio

- Known brand

The key weaknesses are:

- Years of scandals have damaged the reputation and brand

- Lost money over the years

- Customers were not in-favor of the Countrywide acquisition

V. Recent Merger/Acquisition/Divestment Activity

Over the last ten (10) years the Bank of America has adopted a strategy based

on acquisition and merges. In July 2008 the Bank of America acquired Countrywide in order to gain entry and expand its mortgage product line and on 1 January 2009 acquired Merrill Lynch to gain entry and expand the investment product line (Dhulekar, Hensaw and Levy, 2013,p. 37)

The strategic merges where seen as an important strategic move by the Bank of America. Its customers were losing faith with the bank given the low uncertainties of the economy and market (Dyer H., 2005).

By acquiring Merrill Lynch, the bank was able to expand its investment portfolio and increase its global presence. However some may argue that the United States Government forced the Bank of America to acquire Merrill Lynch to avoid the same outcome and faith that occurred to the Lehman Brothers.

The key initiatives from the acquisition meant that the Bank of America could offer its customer base a greater investment product which prior to the acquisition was week. In addition Merrill Lynch brought its large resource and extensive technology and infrastructure capabilities.

The acquisition of Countrywide provided the Bank of America with an entry into the mortgage service markets and expanded its capabilities in that a market.

b) External Analysis

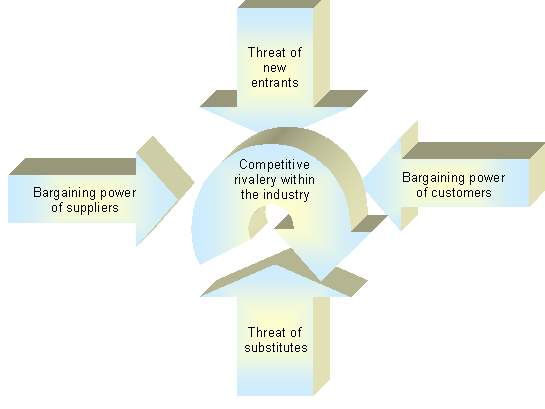

I. Five Force Analysis

Based on the Bank of America’s mortgage business as being the case for its financial problems at the time of the analysis, the analysis only takes into consideration the mortgage segment evaluate its attractiveness to formulate recommendations for moving forward.

Figure 3: Porter’s Five Forces Diagram (Kilpatrick, 2015)

Threat of Rivalry: “Threat of rivalry is high with low diversity among competitors. High barriers to entry and low demand in current economic situation which forces incumbents to compete and cut costs”(Dhulekar, Hensaw, Levy, 2013p. 12 & 13).

Barriers to Entry. “ Barriers to entry are moderate-high. There are increasing government regulations and demands for low cost operations make the industry less attractive” ”(Dhulekar, Hensaw, Levy, 2013p. 12 & 13).

Supplier Power: “ Cost savings are important and drivers the importance of having good technology and innovation place “”(Dhulekar, Hensaw, Levy, 2013p. 12 & 13).

Buyer Power: “Given that switching costs are highly competitive, this allows buyers to shop around ”(Dhulekar, Hensaw, Levy, 2013p. 12 & 13).

Threat of Substitute: “This is low because small banks cannot not complete for loan serving with larger banks”(Dhulekar, Hensaw, Levy, 2013p. 12 & 13).

II. PESTLE Analysis

Following on from the 2008 financial crisis, the markets experienced a global downturn which resulted in the collapse of the USA housing market. A number of major banks went into bankruptcy, stocks were greatly devalued and the government had to step in to stabilise collapse through bank obligation assurance ( Dhulekar, Hensaw, Levy, 2013, p. 19)

| Political factors:

|

Economic factors:

|

| Social factors:

|

Technical /Technological factors:

|

| Legal factors:

|

Environmental factors:

|

III. Competitor Analysis

The Bank of America’s main competitors are as follows.

JP Morgan Chase

“With $2.22 trillion in assets reported in its 2011 third-quarter earnings, Bank of America now ranks second behind JPMorgan Chase, whose assets total $2.29 trillion. JPMorgan Chase also ranks first in terms of branches and total deposits. In September 2008, JPMorgan Chase acquired the investment bank Bear Stearns and Washington Mutual, the largest savings and loans institution in the USA” (Dhulekar, Hensaw and Levy, 2013, p. 19)

Citicorp

“ Citicorp and Travelers Group merged in 1998 to give birth to what is today the third largest bank in the USA with assets of $2.00 trillion”(Dhulekar, Hensaw and Levy, 2013, p 19 & 20)

Wells Fargo

“Wells Fargo acquired Wachovia in 2008 and is now the fourth largest bank in the USA. with assets of $1.3 trillion” (Dhulekar, Hensaw and Levy, 2013, p. 20 & 21)

IV. Opportunities and Threats from External Analysis

Opportunities

- Global and USA presences

- Through acquisitions has expanded its products

Threats

- More players are entering the market place

- Impacts the Global Financial Crisis

- Damage to reputation

SWOT/TOWS Matrix

S-O

- Are able to leverage from extensive market share to offer more products and provide greater shareholder return

- Ability to leverage off of extensive Government Relationships

W-O

- Provide new technology products like mobile and internet banking

- Change branding and image

S-T

- Greater flexibility to generate revenue from extensive product offerings

- Large asset portfolio to offset government tariffs and charges

W-T

- Unknown markets as part of global expansion

- Improve their reputation and provide training the staff

4. Recommendations

The right strategy for the Bank of America will be critical and it must be consistent with the current banking environment and their own competitive advantages and resources. its long-term objective is to grow increase annual earnings and revenue (Milner et al., 2013)

The bank of America needs to consider two strategic options based on our analysis as discussed in this paper.

Option 1. Diversification

Acquire new products to offer its customer in order to differentiate from its competitors and earn new market shares and grow the market in acquisition.

Option 2 Global expansion

The Bank of America can easily spread their activities outside of the USA and grown in the market. They can achieve this by developing products and services with foreign banks achieve better margins in emerging countries than in their own thanks to the economy of scale, there are fewer competitors and taxes.

In addition to the above, the Bank of America needs to put more focus on mobile banking because they are good at it. Emerging countries have trouble accessing banks and agencies, so mobile banking such as Bank of America is very desired by customers (Milner et al., 2013)

References

Dyer H., K. . and S. H. (2005) When to Ally and When to Acquire, Harvard Business Review. Available at: https://hbr.org/2004/07/when-to-ally-and-when-to-acquire.

Kilpatrick, A. (2015) Bank of America Final Presentation by Amanda Kilpatrick on Prezi. Available at: https://prezi.com/nrundmjduscp/bank-of-america-final-presentation/.

Milner, S. et al. (2013) Bank of America ( in 2010 ) and the New Financial Landscape Commercial National Bank and Bank of Italy.

Neeraj Dhulekar, Chris Hensaw, Ethan Levy, L. S. (2013) ‘Bank of America’s _Project New BAC_ – For Good or for Bad 2’.

Yulianto, K. and Adrian, H. (2017) Bank of America – Merrill Lynch Acquisition During Global Financial Crisis. Available at: https://agent909.files.wordpress.com/2017/03/bank-of-america-e28093-merrill-lynch-acquisition.pdf.

Exhibit 1: Value Chain Analysis – Bank of America

Firm

Infrastructure

HRM

Technology

Development

Risk Management

Sales

Products

Marketing

Transaction

Service

Physical and Information Technology

Talent/Competent/Skilled and trust

Technology and infrastructure development – e.g. online banking and mobile banking

Manage risks and establishing risk management guidelines

Image

Brand

Reputation

Growth

Expansion

New Markets

Foreign exchange

Wealth services

Loans

Deposits

Online/Internet

ATM’s

Fast clearances

Customer base

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "Business Analysis"

Business Analysis is a research discipline that looks to identify business needs and recommend solutions to problems within a business. Providing solutions to identified problems enables change management and may include changes to things such as systems, process, organisational structure etc.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: