Conversion of Conventional Multifamily Property into an Affordable Housing Project

Info: 8131 words (33 pages) Dissertation

Published: 9th Dec 2019

The conversion of a Conventional multifamily property into an Affordable Housing project will undertake a number of factors including, location, size, vintage and utilization that the property is currently achieving. In addition, I will need to calculate how much Federal LIHTC credits that I will be able to consume for the redevelopment. Detailed below, I will display the information about the site and a market analysis towards the overall completion of the conversion.

Property Identification

The subject property consists of a 22.000-acre site with a 384-unit apartment complex known as Sendero Ridge. The property is located along the south side of Gold Canyon Drive, just north of North Loop 1604 East, and just west of Redland Road. The address is, 2424 Gold Canyon Road, San Antonio, Bexar County, Texas 78259.

Sendero Ridge consist of nineteen (19), three-story garden-style residential buildings, as well as a single-story leasing office/clubhouse building of similar design. The buildings feature a stucco and fiber-cement siding exterior. The residential buildings feature pitched roofs covered by composition shingles, while the leasing office/clubhouse has a pitched tile roof. Associated on-site improvements include concrete paved driveways, perimeter fencing, and mature landscaping. The property has a reported net rentable area (NRA) of 368,384 square feet and an estimated gross building area (GBA) of 375,684 square feet. The area’s topography is characterized by rolling terrain. There are a few small creeks coursing through the area to facilitate drainage and these areas typically have some flood hazard associated with them.

Under Bexar Zoning and Permitted Uses: Sendero Ridge is zoned within the MF-33 (Multifamily) district permits for multifamily use with a maximum dwelling unit density of 33 units per acre. The ERZD (Edwards Recharge Zone District) restricts certain uses located over the Edwards Aquifer Recharge Zone. City ordinance requires multifamily development to have a minimum of 1.5 parking spaces per dwelling unit, and a maximum of 2 spaces per unit. Based upon a review of the basic zoning ordinance requirements, it appears that the subject’s existing improvements represent a legally conforming use.

Project amenities include two swimming pools, hot tub, sand volleyball court, BBQ grills, covered picnic areas, playground, access gates, carports, detached garages, laundry facility, clubhouse, game room with billiards, media room, business center, and fitness center.

Unit amenities include standard appliances, microwave oven, pantry, walk-in closet, linen closet, garden-style tub, ceiling fans, washer/dryer connections, and patio/balcony with exterior storage. Select units feature track lighting, vaulted ceiling, crown molding, fireplace, built-in bookcase, and/or arched passageway.

According to the central appraisal district, ownership of the subject has been vested in Unified Housing of Sendero RDG, LLC since February 9, 2006, and was purchased from Sendero Ridge, LTD for an undisclosed amount.

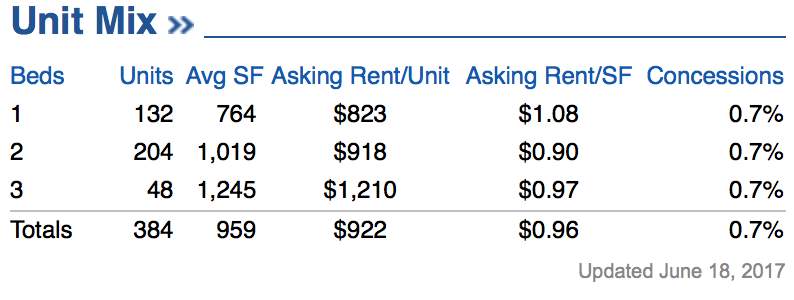

The current unit mix is 34% 1-bedroom, 53% 2-bedrooms and 13% 3-bedrooms. Below is a graph provided by CoStar displaying the current asking market rent, rent per square foot, and average square footage for all units based on unit type.

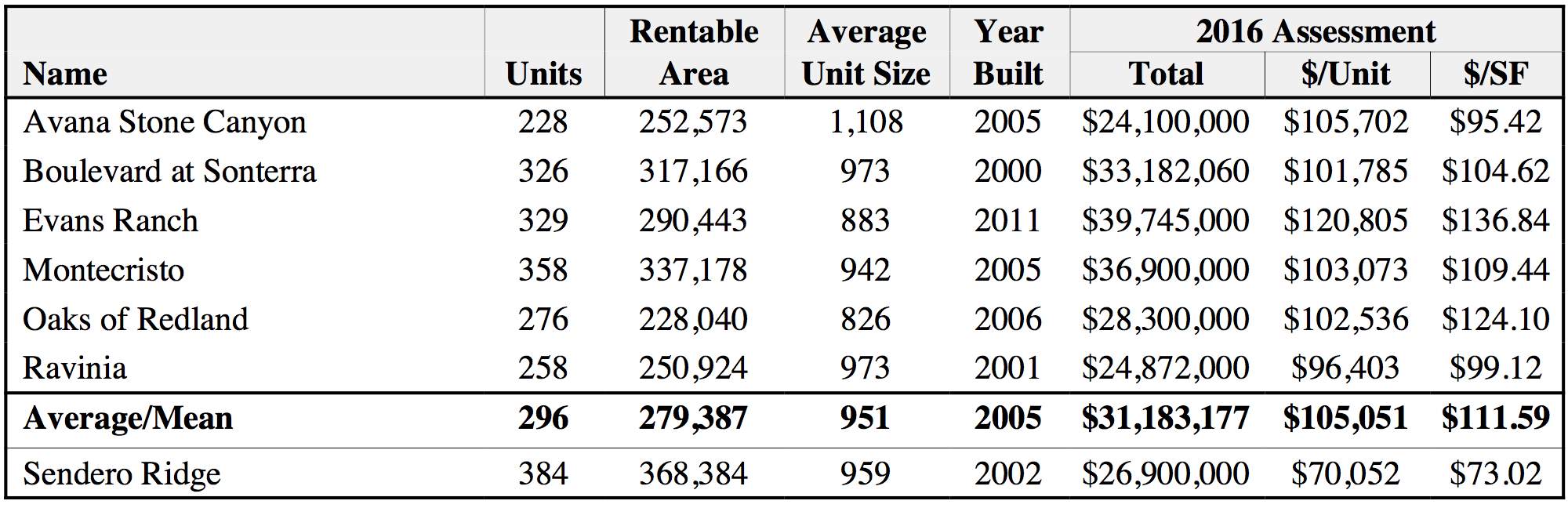

The table below demonstrates the neighboring tax comparables, which were constructed from 2000 through 2011, while the subject property was completed in 2002. The 2016 Bexar County tax assessments for the comparables vary from $96,403 to $120,805 per unit, and average $105,051 per unit; and from $95.42 to $136.84 per square foot, with a mean of $111.59 per square foot. The subject is older than the average property listed however based on the average unit size and total assessed value, these properties present a value add opportunity for a much-needed affordable project. Also, there is an inherent market rent advantage that the property is currently achieving based on the assessed value of 34%. Should the conversion present a greater market rent advantage, then I believe that the nature of affordable housing occupancy plus the sizable market rent advantage will drive down vacancy. Thus, driving up both gross potential rents and net operating income. As a result, a true valuation of the property can increase year over year.

The property’s annual assessment was increased by 4.1% in 2014, and remained flat in 2015 and 2016. The overall increase from 2013 to 2016 is a result of the current recovering market, and is considered reasonable and well supported.

Sendero Ridge’s neighborhood is defined as that area bound by Bexar County Line to the north, Loop 1604 Corridor to the south, Bexar County Line to the east, and Bandera Road to the west. The neighborhood reflects a northerly developing area of San Antonio which is characterized by well above average income levels, and mixed development with a strong and developing residential base and vibrant commercial growth.

The property’s residents currently have multiple access points to several major highways, including Loop 1604, Interstate Highway 10, and U.S. Highway 281. Major area intersections extend across the neighborhood in an irregular pattern, as opposed to an organized grid. Blanco and Bandera Roads are the most noteworthy secondary thoroughfares. Blanco Road cuts through the central portion of the defined area in a north/south direction. Bandera Road, the neighborhood’s western boundary, functions as a portion of State Highway 16. Those areas of the neighborhood within the San Antonio city limits are served by all public utilities. Police and fire service is primarily provided through the City of San Antonio and the Bexar Sheriff’s Department.

The surrounding area neighboring Sendero Ridge is an expanding bedroom community to the San Antonio area with convenient access to the interstate system. Residents of the neighborhood can easily commute to all parts of the metropolitan area. Homes are generally newer with pricing starting at around $250,000 and expanding up into the millions. Housing subdivisions are still under development, especially in the northern portion of the neighborhood. The affluence of the area has resulted in the number of owner-occupied housing units far exceeding other areas of San Antonio.

Every property endures a life cycle which usually consists of four different stages: growth stage, a period during which the neighborhood gains public favor and acceptance; stability, a period of equilibrium without more gains or losses; decline, a period of diminishing demands; and revitalization, a period of renewal, modernization and increase in demand. I believe Sendero Ridge is considered to be within a growth period with notable growth in residential properties over the last several years for both single-family and multifamily facilities. There has been moderate to strong growth of commercial properties throughout the region as well, most notably commercial retail and office properties. The southern portion of the area is more densely developed than the northern periphery. The neighborhood is approximately 40% built-up throughout in the northerly path of growth and includes a complementary mix of residential, commercial, and medical development, generally constructed after 1990. The corridor along Loop 1604 is about 75% built-up and we expect this area to see continued demand in coming years. Demographic projections call for a growing population, characterized by income levels well above the regional average. With this outlook, one can expect continued demand for Class “A” for-rent housing, single-family homes and related commercial development and positive growth is expected in the foreseeable future.

Affordable Housing Opportunities

Increase Developer’ Footprint

The niche market that is Affordable housing has grown since the inception back in 1986. Since then, there have been other statutes set in place to increase the development and construction of affordable housing such as the community Reinvestment Act, that has encouraged lenders to help revitalize the low-to-moderate housing. The federally insured banks are required by law to invest in markets that are stricken with poverty by helping to rebuild the communities with the availability of affordable housing.

Currently, there is a nationwide shortage in affordable housing. This shortage is not limited just to the poverty-stricken families but also for the medical assistants, retail workers, and teachers that are seeking workforce housing. As recent study from Harvard University, showed that in 2014 nearly all the renters in the Seattle metro that earned between thirty (30) to forty-five (45) thousand dollars spent nearly thirty percent (30%) of the household income on housing.

With the rising cost per square foot climbing upwards of twenty percent (20%) according from Apartment Insights. As new properties that are set to come online, the housing construction costs can be equally as high. Which is a common obstacle that affordable and conventional developers run into. This can be even more difficult for affordable builders trying to penetrate a new market. However, with the tax-exempt bonds that are federally funded and tax-exemption programs that incite the development such as real estate abatements, HAP contracts, and various other programs. A builder that looking to increase their overall footprint can look to start leveraging this type of housing.

Reinforce Public Perception

Oftentimes, the outlook of affordable housing developments will bring the association of poor and delinquents. Which is why the resistant to affordable developments are normally met with much disdain. However, affordable housing comes in all size, types and shapes.

The housing complex will be developed to fit their neighborhood which the average person(s) will not be able to differentiate an affordable property to a market property. This will promote a healthy and diverse mixture in each market so that all incomes are not segregated and help drive microeconomics. This is starts from the ground-up, the quality of materials combine with equal construction will help ensure the appeal and quality of the housing. Everyone should have the same quality of living regardless of income. A study has proven that integrated communities perform better economically. As proven by PolicyLink, that a study in Washtenaw County’s GDP would have seen an increase in wages and spending in the community in excess of $1.4 billion dollars if the community was more integrated.

Economic Vitality of an Affordable Portfolio

The performance of an affordable portfolio does better than most would think. First, the given occupancy is normally at or above ninety-five (95%) percent. REIS has predicted that the given supply for affordable property will still be not be enough for the given demand. Also, with the tight margins between income with the set rental restrictions, an affordable property generally has much lower vacancy.

The vacancy is even less when a property has a project-based Housing Assistance Payment (HAP) Contract. These types of contracts will give the developer the ability to finance/refinance their property with the lender having assurance of a steady income stream through the life of the contract. Typical vacancy run between zero (0) and less than three (3) percent. Secondly, with the profits margins being lower than market properties, the foreclosure rates on affordable properties are even less, less than one (1) percent. Lastly, the savvier developers have started to increase their margins by being their own general contractor and property manager at the property to product even more revenue.

Types of Credits

Throughout the process of taking a market property and converting into an affordable multifamily property takes several steps to a full conversion. The first step is understanding what type of conversion the property will be utilizing: 4% or 9% LIHTC. After the establishment of the Tax Reform Act of 1986, which offered an incentive for the increase in developing or major renovation of affordable properties. The tax credits granted to developers who have qualified projects through the competitive application process. In Texas, the Department of Housing and Community Affairs (TDHCA) allocated credits to appropriate projects. The legibility of the any property to be consider as LIHTC, the property is required to undergo a substantial rehab of the property, with Texas defining “substantial” as $6,000 or more per unit or a new construction. The volume of tax credits awarded will be determined by the type of financing, market’s supply of affordable housing units, hard/soft construction cost, and the location of the property itself. The present opportunities that each affordable property brings, is that the affordable properties compared to market properties traditionally maintain higher levels of occupancy and foreclosure rates of less than one (1) percent. Additionally, with the Community Reinvestment Act requiring lenders to participate in providing financing to low-and-moderate income tracts, given the major penalization if a federally insured lender is not in compliance.

As mentioned above there are two different LIHTC tax credits that can be obtained, the 9% tax credits which are depreciable, competitively allocated; the other, a 4% tax credit which is also depreciable and comes with state bond financing, which is capped and allocated by a state agency, which may or may not be very competitive. The 9% credits are typically reserved for new construction or “substantial” renovations. These tax credits are generally credited back to the developer at 9% of the project’s qualified basis. The second type of tax credits 4% deals, are typically used for the new construction and rehabilitation of properties that are being funded alongside bonds that are tax exempt. Similarly, as 9% tax credits, the 4% tax credits are collected annually over a 10 year credit period. To comprehend the method of the LIHTC tax credits, consider the current affordable developments that encompass a qualified basis of $2,500,00. While the development includes a renovation with substantial construction costs, the project will satisfy the limits for the 9% tax credit and produce a cash-flow of credits equivalent to $225,000 ($2.5 million x 9%) per year over the next 10 years, or $2,250,000 in overall proceeds. Using the same scenario for the 4% allocation would be parallel if the project utilized a rehabilitated construction with some form of tax-exempt bonds. Except the developer could become eligible for a generated flow of credits equivalent to $100,000 ($2.5 million x 4%) per year over the next 10 years, or $1,000,000 in overall proceeds. I have concluded that in order to fund the conversion, I (owner/operator) will complete the development using 9% tax credits. As the equity being provided in exchange for the tax credits will help the overall project costs and 9% tax credit deals normally provide the greatest reduction of debt and consequently are able to provide the greatest affordability

In order to ensure that the cost associated with the development of the project, LIHTC eligible costs must be depreciable. Eligible costs include all hard construction costs and most soft costs. The soft costs that are typically eligible are: architectural and engineering cost, developer fees, contractor profits, and construction loan interest. Contingent to the city and/or county, any infrastructure that is built and dedicated to the said city and/or county, can be included as well. The costs that are not eligible would include: land, interest on permanent loans, insurance, and property taxes incurred post completion of construction and any application fees/deposits. Each state awards the credits to developers through a competitive scoring process called a Qualified Allocation Plan (“QAP”).

Recently updated this year, each state will start receiving a LIHTC distribution of $2.35 per person based on their population, with a minimum small population state allocation of $2,710,000. The state allocation limits do not apply to the 4% credits which are automatically packaged with tax-exempt bond financed projects. For example, this year’s allocation for Texas is approximately $65 million dollars. In order for the development to receive an allocation of LIHTC tax credits, the eligibility that are required to be met are determined by the development being able to successfully pass and complete two crucial tests. First, the property must determine what set asides that the property will undertake. As a general rule of thumb, the minimum set asides are as follow; the property will set 20% of the total units at 50% of the area median income or 40% of the total units at 60% of the area median income. There is also a new set aside that is 15% of 40% area median income that will satisfy the first test, however this current set aside has yet to become a relevant option. This test will define what tenants will be able to qualify for the area median income constraints. Secondly, in order to provide housing for the defined tenants with the current asides, the property will be subjected to rental rates to not exceed 30% of the designated set asides as determined by the first test. Once both test have been satisfied, then the property will be able to submit their application for tax credits. However, in order to declare tax credits, the development still needs to be completed and leased to be considered in service.

The tax credits are claimed over a 10-year period and the property is required to maintain affordability restrictions for 15 years to preserve the credits. Thereafter, the affordability restrictions apply for at least an additional 15 years (extended LURA). Once allocated to a project by the state, the Developer must construct the property, certify its cost and lease the units to qualified tenants in order to start the flow of the credits (IRS Form 8609). In order for an investor to use the credit, the IRS requires that the investor have substantial ownership in the underlying real estate associated with the credits. Which the investor will make a capital investment into the partnership that owns the real estate in exchange for a 99.99% limited partner interest and 99.99% of the tax credits. The Developer retains the .01% general partner interest and retains control of the asset. Failing to comply with the LIHTC requirements (affordability restrictions) results in a recapture of the credits, so the private sector is taking the real estate risk, not the government.

Land Use Restrictive Agreement (LURA)

As mention above, the tax credits are claimed over a 10-year period and the property is required to maintain the affordability rental restrictions determined for the initial 15 years to preserve the credits. In this development, I will need to create a Land Use Restrictive Agreement (LURA) on the property.

The Land Use Restrictive Agreement is created and established through public record and runs with the deed in the city and/or county the property is located within. This agreement will set forth the upper limits of the rental rates for either some or all of the units that any development that will constructed in the present or future need to comply with in order for exchange of tax credits. This binding agreement that future owners are subjected to will also transfer to new ownership should the current owner decide to sale the property during the term of the Land Use Restrictive Agreement. The design of the Land Use Restrictive Agreement is to maximize the affordability of the property for the life of the LURA.

The restrictions from the Land Use Restrictive Agreement are generally done over the thirty (30) year time period: the compliance period and the extended use period normally stated within the agreement. The compliance period is the initial term of the agreement which is commonly accepted as the first 15 years of the agreement. This portion of the agreement is monitored and enforced by regulations imposed by the Internal Revenue Service. The second half of the Land Use Restrictive Agreement’s extended use period is an elected option should the owner of the property decided to continue the agreement.

The difference between each period is that during the extended use period, there is no type of penalty assessed on the tax credits after termination. As the initial 10-year period of tax credits are completed and received after the initial compliance period. Should the owner be inclined to terminate the Land Use Restrictive Agreement, then he/she has the option by way of three methods. First, the owner can let the expiration of the Land Use Restrictive Agreement happen naturally through the agreement time period. Second, the owner can go through a qualified termination process. To lift the rental restrictions on an existing property with a LURA in place through the qualified contract process, the LIHTC property owner must exercise his/her option to opt out of the program at the end of the compliance period. In accordance with the process and the state housing agency, the owner will put the property on the market for its qualified contract price. The property must be left on the market for a period of 1 year. If no buyers offer the qualified contract price within the 1 year period, then the state housing agency will lift the affordable housing LIHTC restrictions. The property owner will have to maintain the affordable rent levels from that point in time on existing tenants for 3 years and may not evict tenants without cause. Lastly, the final way out of the LURA is by the lender foreclosing on the property.

I plan on imposing rent restrictions at the property with 50% or 192 units at 60% of the area median income, 25% or 96 units at 80% of the area median income, and the remaining 25% or 96 units at market rates. There will also an income restriction requirement that 75% (288 units) of the units must meet an 80% AMI income threshold. However, this will not affect rents and all of the 60% AMI units will be a subset of the 80% AMI income requirement. The Land Use Restrictive Agreement will go into effect as of the date of acquisition. Per Texas law, I will have three years to bring the property into compliance and still qualify for tax exemption. As such, I plan on phasing in the restrictions over the next 3 years to bring the property into compliance, so that starting in year 4 the property will be fully affordable and in compliance with the LURA.

Tax Abatement

In order to maximize margins, I will also participate in completing a tax abatement that will reduce overall operating expenses and increase total Net Operating Income. In order to achieve the 100% tax abatement, the San Antonio Housing Public Trust Facility Corporation (SAHPTFC) will need to own the land. As a public entity will leased the land back to the developer through a long-term ground lease that will extend past the life of the current loan. Public entities are allowed to enter into such arrangement per Texas Tax Code 11.11. Also, the San Antonio Housing Public Trust Facility Corporation will also need to serve as a sole member as a general partner. I will remain in control and have consent rights over any material action.

San Antonio Housing Public Trust Facility Corporation mission is to be able to provide affordable living for the low-to-moderate families in the surrounding area. The San Antonio Housing Public Trust Facility Corporation was established in 1988 and has transacted in similar deals where they are the general partner. These numerous partnerships have made the San Antonio Housing Public Trust Facility Corporation one of the most prosperous housing authorities in the state.

In addition to the Tax Abatement, all properties that are located in the state of Texas will be subject a Franchise Tax. The “Margin Tax”, is a levy imposed on a taxable entity that is organized and formed in the state that is conducting business. These businesses included but not limited to: corporation, S corporations, professional corporations (PCs), partnerships (LLCs), trusts, joint ventures, banks, state banking associations, saving/loan associations, and other legal entities that conduct business in Texas. Entities excluded from the definition of “taxable entity” and not subject to the Franchise Tax include: sole proprietorships (except for single member LLCs), general partnerships that are organized and ran by a person(s), living estates, real estate mortgage investment conduits (REMICs) and certain qualified real estate investment trusts (REITs); a nonprofit self-insurance trust created under Chapter 2212, Insurance Code; a trust qualified under Section 401(a), Internal Revenue Code; a trust exempt under Section 501(c)(9), Internal Revenue Code; and unincorporated political committees.

In the Summer 2015 Legislative Section, House Bill 32 was passed to provide Franchise Tax Relief. HB 32 reduces the franchise tax on Texas businesses by 25 percent, increases the revenue threshold for businesses to use the E-Z rate from $10 million to $20 million and reduces the E-Z rate from 0.575 percent to 0.331 percent. The recent changes implemented by the state indicate that Franchise Tax is calculated by first determining Total Revenue. Next, the Margin is determined, which is 0.331% of revenue between $1,030,000 and $19,999,999 and 0.525% of revenue over $20,000,000.

Apartment Market Analysis

The property is located in the San Antonio-New Braunfels MSA, also known as “Greater San Antonio.” The metro area’s population at 2.39 million in 2016, up from a reported 2.14 million in 2010—making it the 25th largest metropolitan area in the U.S. and the third-largest in the state. The MSA is also the third-fastest growing large metro area in the state, according to the North Texas Commission. The MSA covers 7,387 square miles and consists of 8 contiguous counties: Bexar, Atascosa, Bandera, Comal, Guadalupe, Kendall, Medina, and Wilson.

Inventory

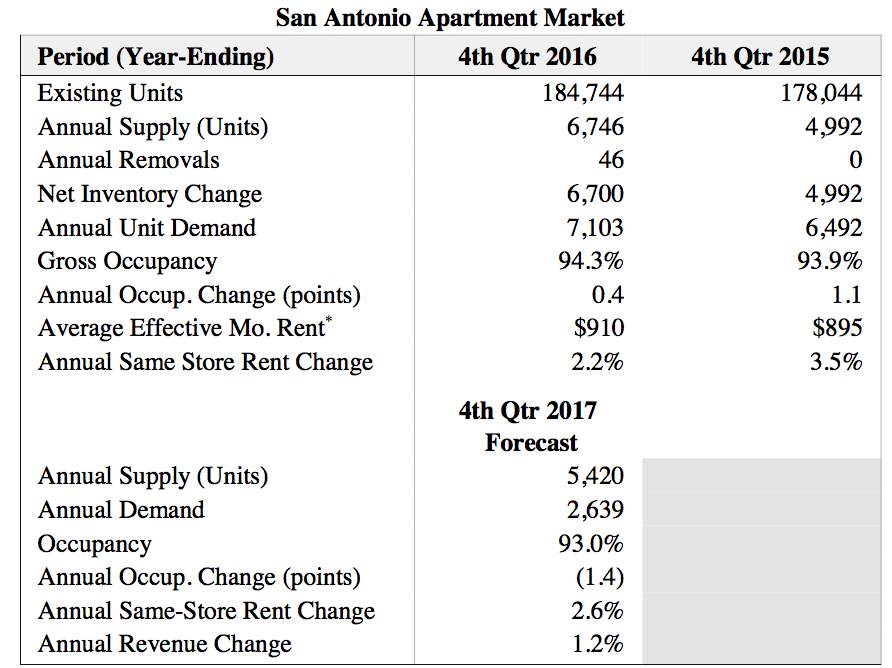

The San Antonio area apartment inventory has grown to 184,744 units as a result of 6,746 units being delivered (and 46 being removed) over the fourth quarter of 2016. This delivery tally expanded the inventory base by 3.8%. During 2016’s fourth quarter, the metro added 684 units. Additionally, the fourth quarter saw 7,133 new units underway. Inventory has expanded at an annual rate of roughly 3.0% to 4.0% in each of the past fifteen quarters, as completions totaled roughly 4,500 to 7,200 units. The 5,420 units slated to be delivered by 2017’s fourth quarter will expand the apartment base in San Antonio by 2.9% upon delivery. Identified projects and permit volumes suggest that supply should taper over the next year.

Occupancy

Overall occupancy in San Antonio, as of the fourth quarter 2016 stood at 94.3%. This is a marginal uptick of 0.4 point(s) from the year prior, hovering at or above San Antonio’s historical norms but low among Texas metros and in the national picture. Occupancy has remained around 93% to 94% over much of the past five years. In terms of occupancy by age of community, that properties built in the 1990s (94.9%) pulled up San Antonio’s overall rate, followed closely by properties built in 1980s with a rate of 94.7%. The properties built in 2000 or later achieved a rate of 94.4%. The properties built in 1970 or earlier posted a rate of 94.1% while vintage pre-1970s properties showcased the weakest average rate of occupancy at 91.4%.

Rental Rates

As of 2016’s fourth quarter, rents for all existing product in San Antonio averaged $910 per month, or $1.073 per square foot. Same-store prices in San Antonio decreased by -0.8% in fourth quarter 2016. Annually, rent growth in San Antonio registered at 2.2%. Annual rent growth has measured roughly 3.0% to 4.0% in seven of the past eight quarters, in line with or slightly above the average of 2.8% over the past three years. Class A and B units continue to drive rent growth in San Antonio, though competition from new supply has weighed on increases in newer product. Most submarkets have seen improved performances, with the largest increases seen in the low supply areas north of downtown, inside Loop 1604, and on the metro’s west side.

Absorption/Demand

San Antonio’s apartment supply topped demand levels during 2016’s fourth quarter, 684 units to 246 units. We note however that on an annual basis the metro posted absorption of 7,103 units, which outpaced new completions (6,746 units) delivered in the past year.

Over the coming year ending in fourth quarter 2017, the San Antonio area is forecasted to have a demand of 2,639 units; with 5,420 units projected for delivery this translates into a negative absorption of about 2,781 units, and an anticipated occupancy rate of 93.0%.

Apartment Market Summary

The San Antonio metro has traditionally been a moderate-growth metro with a local economy that is heavy on government-related jobs but not on large private-sector employers. San Antonio’s largest employers are heavily concentrated in either the public sector or in healthcare, stable anchors which help during economic downturns, but limit upside potential during prosperous times. However, economic activity and job growth levels have picked up to strong levels in the past three years and a wider variety of companies is emerging. Meanwhile, larger companies are beginning to concentrate in the central business district as office development continues in the area.

Still, economic progress and population growth don’t translate into housing demand as quickly in San Antonio as they do in other metros that have given Texas a fast-growth reputation. Rather, those trends translate to consistency within the San Antonio apartment market. While usually moderate, apartment demand has risen to solid levels in response to new supply. Overall, high-supply submarkets generally drive absorption, but with sustained supply, occupancy rates in those areas have faltered. Metro-level occupancy continues to trail most other major Texas metros and the U.S. norm. Likewise, rent growth levels in San Antonio have typically underperformed. San Antonio’s market dynamics are unlikely to significantly evolve in the near term, resulting in a modest-to-moderate long-term outlook for revenue growth.

Demand fell short of supply levels in San Antonio during 2016’s fourth quarter. While 684 units came online, just 246 units were absorbed. In turn, occupancy dipped 0.2 points quarter-over-quarter, landing at 94.3%. On an annual basis, demand (7,103 units) exceeded net new supply (6,700 units), pushing occupancy up 0.4 points year-over-year. On the pricing side, apartment operators in San Antonio lowered rents 0.8% in fourth quarter 2016. Year-over-year, rents were up 2.2%, falling short of San Antonio’s five-year average of 3.0%. The San Antonio apartment sector boom in 2011 and 2012 leading to some optimism that the market was emerging into something more than a low-risk, low-reward market. But after a lull in the following two years, such optimism was deflated. San Antonio’s apartment market typically regresses back to its consistent patterns with occupancy around 93% to 94% and annual rent growth around 2.5% to 3.5%.

Demographics

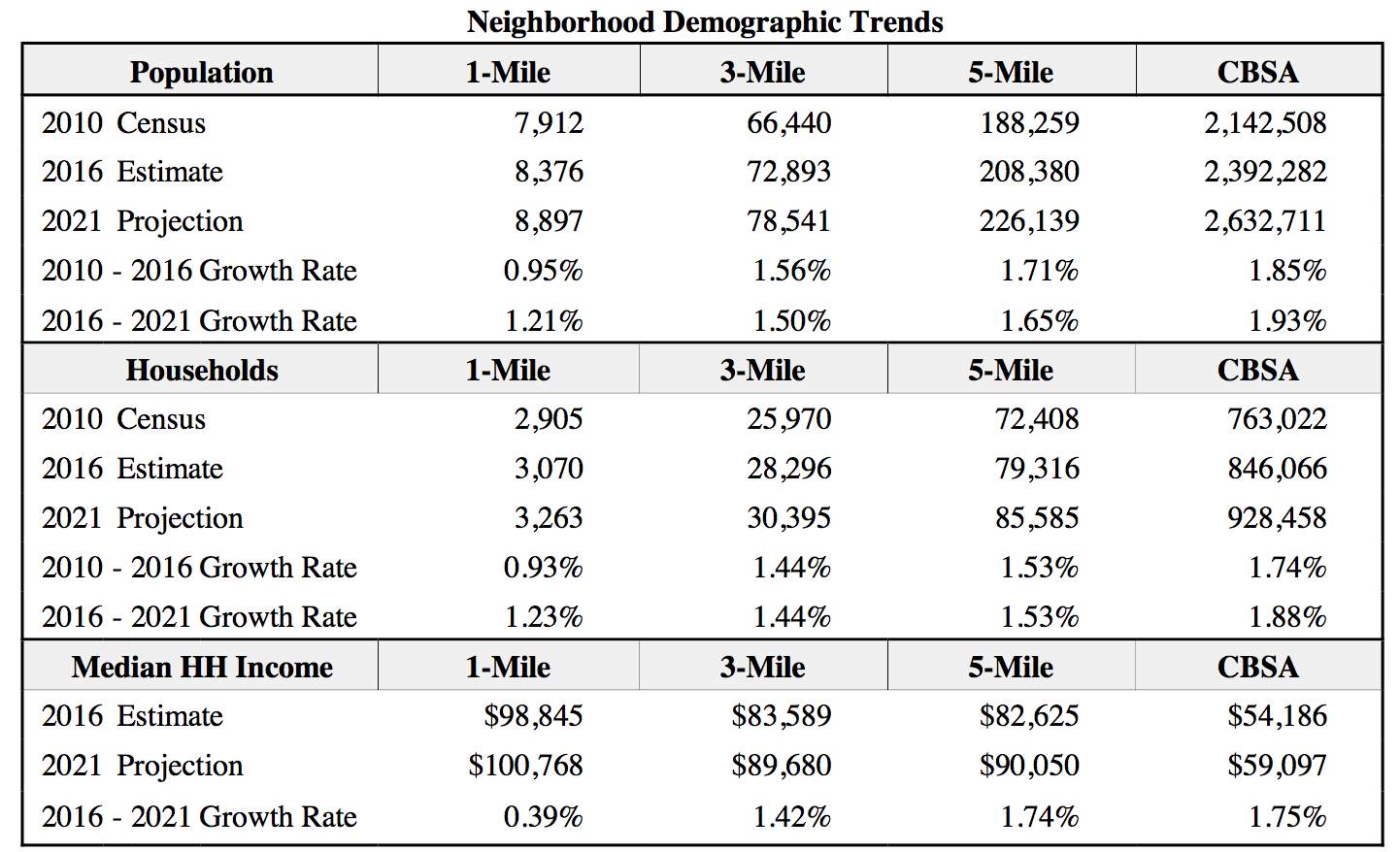

The following table summarizes population, household and median income trends within 1-, 3-, and 5-mile radii of the subject, as well as comparative figures for the CBSA:

As shown, from 2010 to 2016 the population within a 5-mile radius of the subject grew from 188,259 to 208,380, expanding at an average compounded rate of 1.71% annually. Over the same period, the number of households increased at a slower rate of 1.53% (indicating an increase in the average household size). Looking forward, the projections from 2016 to 2021, annual population and household growth (within a 5-mile radius) will average 1.65% and 1.53%, respectively, compared to CBSA growth rates of 1.93% and 1.88%. Over the same period, the median household income is projected to increase by 1.74% to $90,050, which is 52.4% above the forecasted CBSA median of $59,097.

Market Rent Analysis

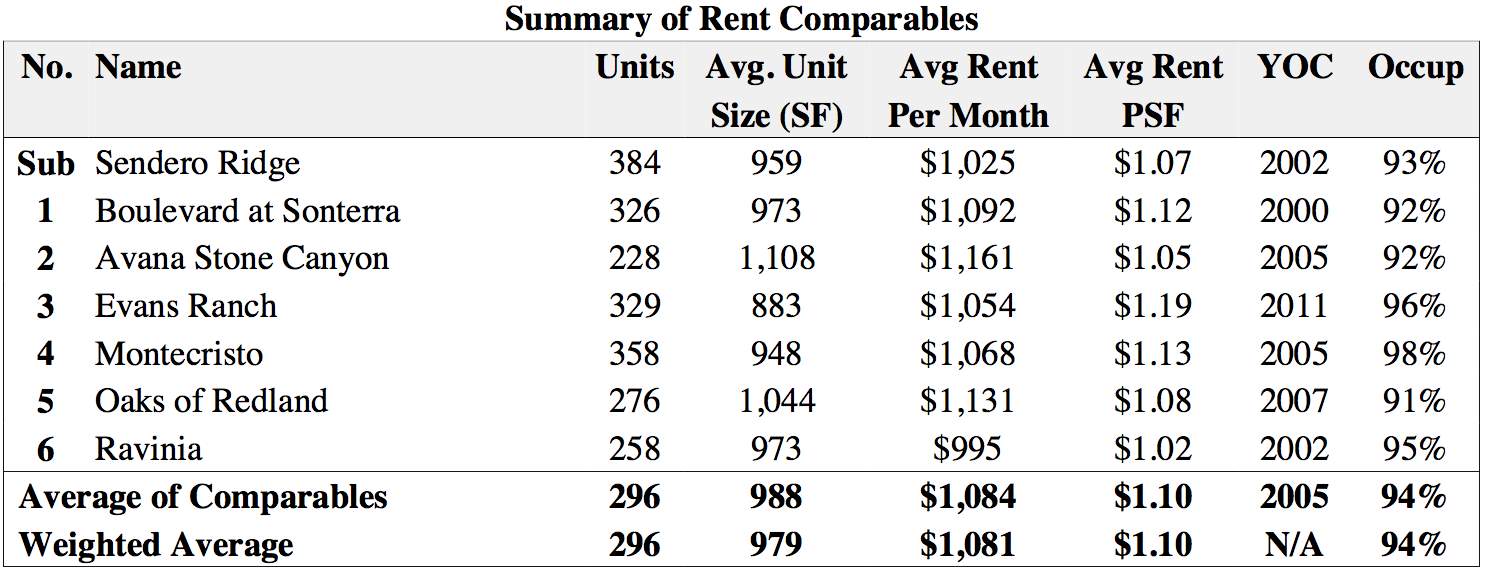

Relative to the market rent comparables below, the subject’s average monthly rent appears to be within the range and slightly below the mean on both a per unit and per square foot basis. Many of the properties within the table show that the immediate market has typically been providing a market rent with no additional lease discount, beyond student or preferred employer discounts. Only one of the rent comparables is offering a lease concession with Oaks of Redland providing a $500 discount off the first month’s rent on select units (roughly a 3-4% discount).

Among the subject’s direct competitors, occupancy levels ranged from 91% to 98%, and average 94%. Occupancy rates slipped in this area in 2009/10, but have been fairly strong throughout 2016 and early 2017. Asking rental rates range from $1.02/SF to $1.19/SF, with an average of $1.10/SF. Rents were reported to have increased at the subject and most of the competitors during 2016, with most of the leasing professionals we surveyed indicating that rents are expected to increase slightly over the next year. Overall, the subject appears to be performing in-line with the nearby similar quality properties on an occupancy level and rental rate basis, after consideration of varying discounts, amenities, unit size, parking amenities and quality differences. In summary, the subject’s market area appears to have recovered to a relatively high-occupancy level and should report growth in effective rental rates over the next few years.

Property Takedown

The hardest and normally the most complicated hurdle to complete is acquiring the property. The intentions to take the property from a market property into an affordable housing complex can often lead to alternative solutions in order to achieve the acquisition. Below I show display my determination on purchase price.

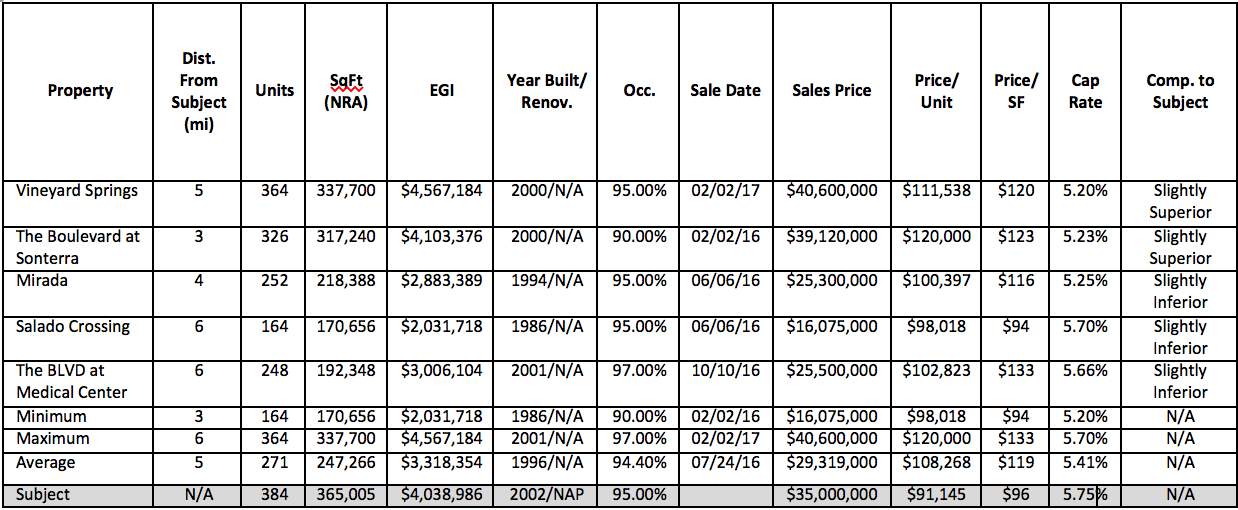

Frequently, developers will use similar comparables in the neighboring area in order to convince the current owner that despite their assumed valuation of the property. The changes in the market will either drive up or drive down true valuation. In each of the sales comparables that I have pulled from the market, each property will have similar characteristics as the subject property. The sale prices of the comparables ranged from $98,018/unit to $120,000/unit with an average of $108,268/unit. I placed the greatest emphasis on comparables 1 and 3 due to the minimal adjustments of the properties. Overall, I have concluded that the range of the comparables and reflect the Sendero Ridge’s quality, condition and location.

Sale Comparable 1

Vineyard Springs is considered to have similar location attributes when compared to the subject, which is located about 5 miles east of this property. The comparable has an average unit size of 928 square feet, which is considered similar to the subject’s average unit size of 959 square feet. The sale is a class A-property, which is similar to the subject. Sale No. 1 was built in 2000 and is in average condition. After evaluating the amenities, which are considered superior, I conclude that when considering the economic and physical factors, this improved sale is superior overall and warrants an adjustment to the sales price. This has been estimated at -5%, resulting in an adjusted.

Sale Comparable 2

Sale Comparable 2

This property is considered to have superior location attributes when compared to the subject, which is located approximately 3 miles east of this property. The comparable has an average unit size of 973 square feet, which is similar to the subject’s average unit size. The sale is a class A- property, which is similar to the subject in terms of overall quality and appeal. Sale No. 2 was built in 2000 and is in average condition. After evaluating the amenities, which are superior, I have concluded that when considering the economic and physical factors, this improved sale is superior overall in relation to the subject.

Sale Comparable 3

This property is considered to have similar location attributes when compared to the subject, which is located approximately 4 miles northeast of this property. The comparable has an average unit size of 867 square feet, which is inferior to the subject’s average unit size of 959 square feet. The sale is a class A- property, which is rated similar to the subject. Sale No. 3 was built in 1994 and is in average condition. After evaluating the amenities, which are considered similar, I have concluded that when considering the economic and physical factors, this improved sale is inferior overall in relation to the subject.

Sale Comparable 4

Salado Crossing, located at 13230 Blanco Road, is considered to have similar location attributes when compared to the subject, which is located approximately 6 miles northeast of this property. The comparable sale has an average unit size of 1,041 square feet, which is considered superior when compared with the subject’s average unit size of 959 square feet. The sale is considered a class B- property, which is recognized as inferior to the subject. Sale No. 4 was built in 1986 and is in good condition. After evaluating the amenities, which are considered inferior, I have concluded that when considering the economic and physical factors, this improved sale is inferior overall.

Sale Comparable 5

BLVD at Medical Center is considered to have superior location attributes when compared to the subject, which is located about 6 miles northeast of this property. The comparable has an average unit size of 776 square feet, which is considered inferior to the subject’s average unit size of 959 square feet. The sale is a class A- property, which is similar to the subject. Sale No. 5 was built in 2001 and is in average condition. After evaluating the amenities, which are considered similar, I have concluded that when considering the economic and physical factors, this improved sale is inferior overall.

The sale price per square foot indicator is applicable to each of the properties. However, it is a common element which is general in nature and takes into account all influences without specifically identifying their impact. Price variations are general attributable to a number of factors including Sendero Ridge’s quality of construction, average unit size, location, and amenities. The comparable sales displayed above price on a per square foot basis ranging from $94 to $132.

The sale price per unit indicator is also applicable to each of the properties. However, like the per square foot indicator, it is a common element which is general in nature without specifically identifying their impact. Many of the same influences that affect the sale price per square foot also affect the sale price per unit. Among the comparables presented, the sale price per unit ranges from $98,018 to $120,000.

In addition to the method of comparisons above, the effective gross incomes of Sendero Ridge fall within reason of the sale comparables. The noted effective gross incomes above is utilizing the proposed unit mix as mentioned above; 50% of the units at 60% of the area median income, 25% of the units at 80% of the area median income, and 25% of the units at market rental rates. Given that the property will transition into an affordable property, the property is still able to remain competitive in nature against other market properties.

This indication will help in the determination of a final cap rate. The subject compares very well with the selected sales generally falling within the range with respect to the various physical characteristics that are easily quantified such as project size, average unit size, and age. The proximity to the subject is rated as similar to the sales, with all six sales being within six miles of the subject. During the time period of the sales presented cap rates have remained relatively stable though the recent sales. Overall, I believe that the selected cap rate of 5.75% for the subject should be slightly above the mean, while placing notable weight on Sales 1, 2 and 3, and Sale 5. I have concluded that the rate should be most similar to Sales 1, 2 and 3, prior to considering an upward adjustment of roughly 25 points based on the recent increases in financing costs and an additional 25 points based on the property being affordable.

Overall, I have submitted a $35 million dollar bid into the seller with my determinations of value of the property given all of the factors presented. I am pleased to announce that the bid was successfully and the seller has given me a 90-day closing period with a 30-day option period. I will be using the 5.75% cap rate throughout the process.

Rehabilitation Menu

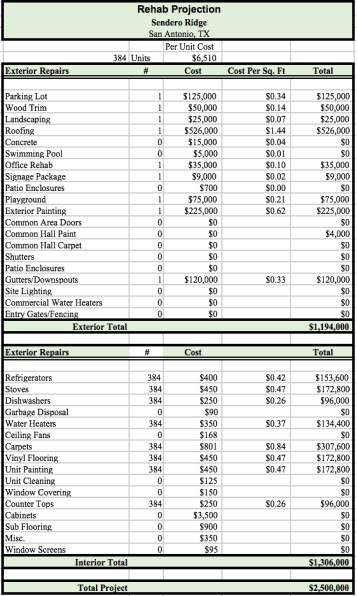

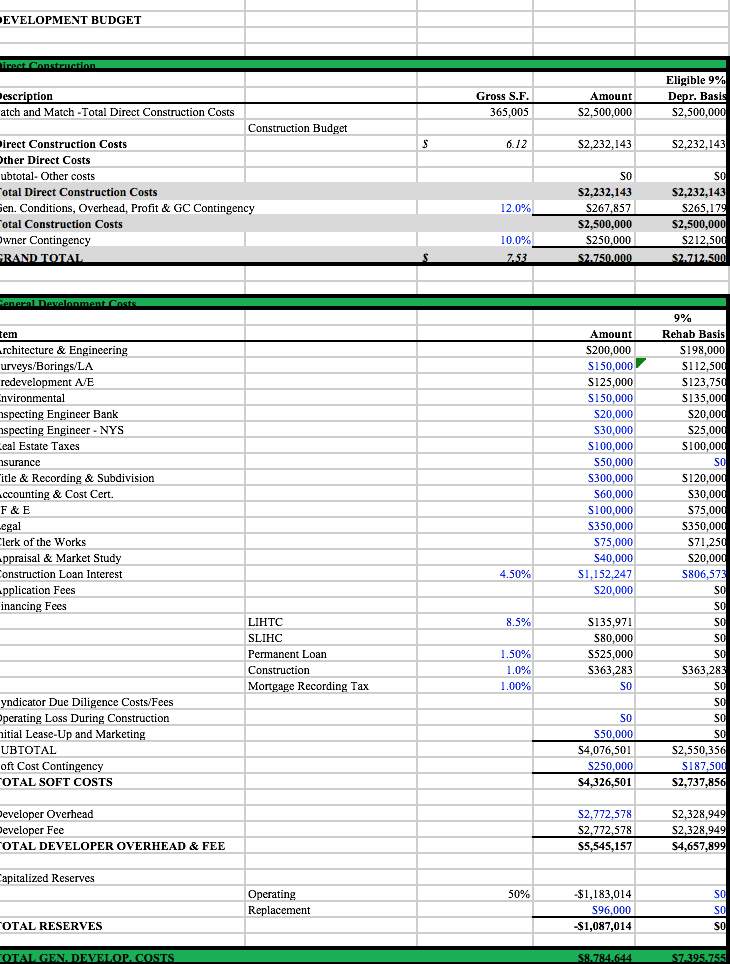

For the property to be considered for new tax credits, I determined that the only option was to complete a substantial rehab at the property. In the state of Texas, substantial rehab is anything over $6,000 per unit. Currently the cost per unit is at $6,510. Given the age of the property, I found that I had to consider any cost that I would need to complete before the exiting the property within the 15-year holding period. This included: the resurfacing the parking lot, updating the wood paneling, landscaping, roof replacement, minor office rehab, updated signage, installation of a new playground, exterior painting, full gutters/downspouts, and replacements of appliances (refrigerators, stoves, dishwashers, and water heaters) with Energy Star appliances. The total rehabilitation will total approximately $2.5 million dollars .

Budget

The continuation of the Rehab Menu flowed into the Development Budget. Total direct cost of construction was matched dollar-for-dollar as dictated by the qualified eligible costs of a 9% tax credit deal. However, the reduction of non-qualified costs was estimated at $267,857 which netted a new overall eligible cost of $2,232,143. General development cost follows as such:

- Unless specified, the given estimates are of the market:

- The Architecture and Engineering cost was an estimated 8% of direct construction

- Federal LIHTC Fees are 8.5%, totaling $135,971

- State LIHTC Fees are an even $80,000

- The Permanent loan fee is 1.50% or $525,000

- Construction loan fees totaled 1.00% or 363,283

Work Cited

- www.sanantonio.gov.

- http://property2.costar.com/Property/Detail/Detail.aspx?ID=6040860&Results=0

- https://www.realpage.com/mpf-research/the-nations-10-busiest-submarkets-for-construction-far-northwest-san-antonio-texas/

- https://www.realpage.com/mpf-research/can-san-antonios-apartment-sector-catch-texas-peers/

- https://www.realpage.com/mpf-research/apartment-market-update-mpfs-greg-willett-apartment-demand-kicks-san-antonio/

- https://se.reis.com/custom-report

- http://www.bcad.org/index.php/LowIncomeCapitalizationRates

- http://www.statutes.legis.state.tx.us/Docs/TX/htm/TX.11.htm

- http://www.bcad.org/clientdb/?cid=1

- https://www.realpage.com/mpf-research/rent-growth-square-footage-tx/

- http://www.tdhca.state.tx.us/multifamily/bond/docs/FAQs.pdf

- https://tn.gov/assets/entities/tacir/attachments/Tab_6_-_Attachment_2_-_The_Appraisal_Journal_of_the_Appraisal_Institute.pdf

- http://www.freepatentsonline.com/article/Appraisal-Journal/130971011.html

- https://www.huduser.gov/publications/pdf/what_happens_lihtc_v2.pdf

- https://www.fdic.gov/bank/historical/managing/history1-15.pdf

- http://www.crefcoa.com/land-use-restrictive-agreement.html

- http://www.nreionline.com/multifamily/outlook-positive-affordable-housing

- http://www.seattletimes.com/business/real-estate/four-approaches-to-affordability/

- https://www.multihousingnews.com/post/lihtc-properties-continue-strong-performance/

- http://www.ewashtenaw.org/government/departments/community-and-economic-development/housing-and-community-infrastructure/affh/frequently-asked-questions_web2016.pdf

- http://www.housingfinance.com/finance/the-ins-and-outs-of-financing-sec-8_o

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "Property"

Property refers to buildings and structures, owned by an individual, group of people, or an organisation. There are three types of property, including public property, private property, and collective property.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: