A Study of the Australian Home Loan Market

Info: 7661 words (31 pages) Dissertation

Published: 3rd Feb 2022

Abstract

This study aims at considering the major issues that the Australian Home Loan market is facing and recommends certain strategies that would help the borrowers to overcome the issues and distress faced by the Australians. In order to carry out this particular study, a detailed investigation has been made on the present Australian market in terms of its mortgage or loan provided to the borrowers. In order to gain useful information and understanding on the same, several news articles and reports have been analyzed. The entire research is based on the findings of the secondary research only because there was no such scope of primary research. The issue that has been identified in the study is that whenever a home buyer is rushing in the property market, the homeowners have to face certain issues related to the mortgage or the loans that they have to take from the banks. The issue has been faced by the Australian since a decade when the Australian Prudential Regulation Authority started releasing its data in the year 2008. The situation has worsened due to the increased power of the Big Four Banks of Australia that have dominated the Australian market largely.

It has been found that the major concern related to the home loan is the switching cost that the borrowers have to pay when they switch their home loans. In order to avoid the extra charges that the consumers have to pay in the name of the switching costs the approach of home loan portability can be taken into consideration. Home loan portability is the feature that is the left over from the mortgages that is used to overcome the exit fees. The fees are charged by the lenders when there is a simple switching of the home loans from the existing loans.

Table of Contents

Click to expand Table of Contents

Chapter 1: Introduction

Chapter 2: Research methodology

2.1 Introduction

2.2 Research paradigm

2.3 Research approach

2.4 Research Purpose

2.5 Research Strategy

2.6 Data Collection Method

2.7 Data Analysis

2.8 Ethical Issues

Chapter 3: Findings of the literature review

Chapter 4: Data analysis and interpretation

4.1 Introduction

4.2 Structure of the market share of the Australian home loan industry

4.3 Housing index of the Australian Home loan industry

4.4 Mortgage lending

4.5 Home loan distribution of the state

4.6 Contribution of Banks and Non-banks in the home loan industry

4.7 Major reasons for the switching over of the home loans

Chapter 5: Conclusion and recommendations

Recommendations

References

Chapter 1: Introduction

The Australian house loan market has been in a turmoil situation due to a number of factors. The Reserve Bank of Australia has serious concerns regarding the house loans in the recent time. The danger that they used to face earlier has increased to a large extent. The Australian economic indicators shows serious concerns on the issues related to the property market (Favilukiset al. 2017). If the apartment markets in Brisbane and Melbourne is taken into account, the resilience of the Australian market is in great threat when the property market of Australia is concerned. In addition to this, the Big Four Banks of Australia have always put pressure on the borrowers with their different schemes and increasing rate of loans. This has automatically created major issues in the home loan market of Australia.

This study aims at considering the major issues that the Australian Home Loan market is facing and recommends certain strategies that would help the borrowers to overcome the issues and distress faced by the Australians.

Research project description

In order to carry out this particular study, a detailed investigation has been made on the present Australian market in terms of its mortgage or loan provided to the borrowers. In order to gain useful information and understanding on the same, several news articles and reports have been analyzed (Lou and Yin 2014). The entire research is based on the findings of the secondary research only because there was no such scope of primary research. In order to carry out the study, a detailed literature review had been conducted that helped to identify the issues and problems faced by people when it comes to home loans or mortgage. It is on the basis of the secondary research and the outcome of the literature review, the complete analysis of the study has been made on the basis of the outcome.

Research aims and objectives

- To examine the switching costs that Australian homeowners have to pay for their home loan

- To analyze the market structure of Australian loan market

- To find out the relationship between switching cost and entry/exit conditions

- To understand the long-term effect of the removal of unfair switching costs

Rationale of the research

The issue that has been identified in the study is that whenever a home buyer is rushing in the property market, the homeowners have to face certain issues related to the mortgage or the loans that they have to take from the banks. The issue has been faced by the Australian since a decade when the Australian Prudential Regulation Authority started releasing its data in the year 2008 (Randolph et al. 2013). If the Australian loan market is considered, similar situations have been faced by the borrowers and the loan takers. One of the major issues that these people have to face is the increasing rate of switching cost. Australians consider this switching cost to be a burden for then because without any proper reason they have to bear extra expenses.

This is an issue because the number of Australians who are depended on the home loan market is huge and at the same time the numbers of Australians who are purchasing homes are also increasing (Priemusand Whitehead2014). In addition to this, the economy of Australia is also in a stable position as well that has degraded the overall market of Australia. This is the reason that the outrage of the people has increased by many folds when it comes to charging high amount of money for the same of home loans.

This study shall focus on the current market structure of Australia and the other concerns related to the mortgage and the home loans that the Australians have to face in the recent time. The study shall also focus on the major factors that are responsible for the degrading condition of the home loan market and how the government of Australia has been dealing with these issues. The short term and long term impact of these issues will be highlighted. On the basis of the detailed analysis, certain recommendations shall be made that would eventually help the overall loan market to consider the declining situation and come up with better practices that would help to improve the present situation and create better opportunities for the Australians as well.

Chapter 2: Research methodology

2.1 Introduction

In this given chapter the researcher has provided in-depth knowledge about the Research Design and method that is being used in order to fulfil the purpose of the study and collect valuable information relevant to the research topic. Proper justification has also been provided about the particular research method and design that is being selected during each step and that can help in contributing to the research conclusion of the research topic related to various aspects of the Australian home loan industry. The data that are being collected are properly analysed using suitable data analysis technique that can help to make proper interpretation and conclusion and thereby fulfil the objective of the research.

2.2 Research paradigm

According to the work of Macke and Gass (2015), there are two types of research philosophy and paradigm. There is the positivism philosophy which helps to examine the existing problem of the research area and also highlight up on the facts and information that are available and aims to improve upon the area of the research and also make further compare to the area of the research with the help of the existing data and information. On the other hand, the interpretivist philosophy aims to improve upon the subject area of the research using the experience encountered by human related to the subject area of the research.

The given research work really use both kind of philosophy in order to ensure that all the relevant information related to the Australian home loan market and also the experience encountered by the customers of banks and other Financial Institutions are properly analysed in order to evaluate the present scenario of the home loan industry.

2.3 Research approach

It is evident from the fact that there are two types of research approach that are used by the investigators in major research work and dissertations in order to properly evaluate and deal with the objective of the research. There is the deductive approach of research that can help the investigator to concentrate on top down knowledge of the subject area and is thereby prepare a hypothesis after proper review of the existing literature (Taylor et al. 2015). However it is important to have proper authenticity in order to ensure that only the correct form of data are being used. There is also the inductive form of research approach, which can propose new theories and hypotheses relevant to the research topic. The inductive approach can be used by the researcher on the other hand to reduce new theories and hypothesis that is relevant to the research topic. It tries to use all the relevant information related to the research topic area and also make proper interpretation in order to deduce the new hypothesis.

In the given research work the deductive approach is more appreciable as it will help to use all the existing information and theories related to the scenario of the Australian home loan market. It is also possible to make proper evaluation of the current scenario of the home loan market and therefore have proper conclusion that can help the observer to understand the various aspects of the home loan industry.

2.4 Research Purpose

It is important to apply the perfect research techniques to fulfil the purpose of the research that can help to identify and establish relationship related to various aspects of the research. There is the exploratory research purpose, which focuses on the background area of the research topic and therefore makes significant contribution in understanding of the relevant topic related to the research area. There is also the analytical purpose that focuses on the association between various dependent and independent variables related to the research work and also help in understanding of the uncontrolled variables that can help to explore the research problem and thereby fulfil the objective of the research (Vaioleti 2016).

In the current research work, the investigator will use both kind of research purpose which will help to ensure that all the background information related to the Australian home loan market and also the dependent and independent variables of the financial terms are properly utilised in order to make perfect evaluation and understanding of the current scenario related to the Australian home loan market.

2.5 Research Strategy

The research strategy is the overall Framework that can be used by the investigator in order to fulfil the purpose of the study and also collect relevant information. According to Panneerselvam (2014), the survey an interview or one of the popular mode of strategy that can be used by the research are in order to design the overall research work and that is one of the most cost effective strategy.

In the following research work however the investigator has followed the secondary method of strategy where the existing knowledge is being used without the use of proper survey and interview. By properly analysing the relevant existing literature of the Australian home loan market it is possible to analyse the current scenario compared to that of the past condition of the Australian home loan industry.

2.6 Data Collection Method

This is one of the most important parts of all research methods which help the researchers to collect relevant information and data related to the subject of the research area. Without proper information or data it is not possible to properly evaluate the subject area of the research that can help to determine and understand the subject area of the research. It is also important to have it element method of Data Collection that can help in contributing to the objective of the research. The data collection method also depends upon the budget that is available for the researcher in order to carry out the entire research work.

Bauer (2014), has mentioned about the two major types of Data Collection method that are used in all type of Investigation in order to collect relevant and authentic data. There is the primary method of Data Collection at the researcher collect data in the form of survey and interview from the subject area of the research and also the sample size. Proper questionnaires need to be design in this kind of Data Collection method which will ensure that maximum amount of information can be collected from the sample size.

The current research work relevant to the Australian home loan market will however focus only on the secondary method of Data Collection that help to gather information from the secondary source that help to gather information from the secondary sources which include all the previous research work and reports relevant to the subject area of the research. The researcher has focused on all the financial report of the Australian home loan market and also the budget planning method that has provided valuable information related to the performance of various Financial Institutions and banks of the Australian home loan industry.

It is also important to have a proper sampling method that can help the researcher to use the proper exclusion and inclusion criteria (Palinkas et al. 2015). This will help to ensure that only the relevant data are being collected that can help to properly evaluate the current scenario of the Australian home loan industry. The researchers had mainly aim to focus on the statistical information that has properly able to understand all the relevant information related to the Australian home loan market.

2.7 Data Analysis

The researchers have used qualitative data analysis method in order to properly evaluate all the secondary information that is collected from the financial reports and journals of the Australian home loan market. Proper interpretation of all the relevant secondary information is also made in order to ensure that the objective of the research is fulfilled and proper recommendations can also be provided accordingly (Gale et al. 2013).

2.8 Ethical Issues

In order to maintain the authenticity and validity of the data that are being collected the researchers have ensured that the entire Peer reviewed journals and reports are being used as the source of secondary information. The researcher had also taken proper consent and permission from the copyright holders of the reports and journals in order to ensure that no unfair advantages are being taken while collecting the information for the research.

Chapter 3: Findings of the literature review

It has been clearly identified that the big four banks in Australia, namely, Westpac, the Commonwealth Bank, ANZ and the NAB plays a significant role in the Australian economy and they have the financial stability that would eventually support people’s home loan and keep their home safe. It has been found that these 4 Big Banks hold nearly 85% of the entire home loan share between them. The home loan rate varies between 5.2% to 5.3% p.a.; however, the rate might vary according to the schemes and offers offered by these Banks (Shaoet al. 2015). As point out by Menget al. (2013), that seeing the rise of home loan rate by Commonwealth Bank and the ANZ, the other two banks also announced its hike in the rate. The reason behind this increase has been stated as the rising cost and the regulatory responsibilities that these Banks have to perform. However, in clarification they have also declared that they have been seeking better ways to minimize the rate of the loan for the Australian Families who have been trying to pay off their loans (Stewartet al. 2013).

The Big Four Banks have collectively reached a whopping $98 million as they hit the investors with their out of cycle hike in their loan rates. The Reserve Bank of Australia has also deterred the banks to lift their huge rate of loans and how these banks have been giving pressure on the borrowers (Stebbingand Spies-Butcher2016). With the announcement of the profit margins by the major Banks, the scenario was clear among all that the Banks have been merely utilizing the money of the borrowers in order to increase their profit margin. On the other hand, the borrowers are left with no other options but to lend money for the sake of getting a home loan from these Banks (Badevet al. 2014).

If the switching cost that the consumers have to pay for the home loan is taken into consideration, it has been observed that most Australians move their home at least twice in every 15 years of their stay. If the standard loan term is taken into account, it lasts for at least 30 years. Therefore, easily it can be stated that the Australians are shifting twice in the duration of each home loan. This is the reason that the Australians have to take the burden of mortgage at the time of shifting in order to avoid the cost and hassle that they have to face at the time of shifting their houses or residents (Knowleset al. 2017).

The home loan market structure is taken into consideration, the first thing to mention is that residential mortgage and home loans are important loans in the Australian market because the Australian are found to purchase a home for their living. As a part of their purchase making decision, taking mortgages fall under the dominant liability of the people. If the residential mortgage debt to the GDP of the country is taken into account, it has been found that Australia falls under those countries that have highest rate of home ownerships including the other countries like Germany and UK (Norris 2016).

The main Australian cities like Brisbane and Melbourne sees a major threat to the resilience of the Australian financial system in the overseas. In addition to this, it has also been found that the loan borrowers at times also aim at providing the loan before the time but they had to face certain issues in that also. In this respect, Mooreet al. (2014) commented that the economic distress that Australia has been facing is not as high compared to the other countries like America but the situation seemed to degrade to a large extent. The economic downturns have created a tightened situation for the lenders and the borrowers. All these chaotic situations has definitely certain short term and long term effect on the overall loan market of Australia and this could be the situation where the Australians have to suffer (Delfaniet al. 2014).

The long term impact of the degrading condition of the loan market can also lead to situations like low employment rates or changes in the average income level of the people putting every person in a stressed situation. As it has been evident that the house prices have continued to grow in Australia by approximately 2-3% and the housing prices is still growing without any consideration. This is the reason that the turmoil in the housing loan market has been increasing. On one hand, the bank rates of home loans have been increasing and on the other, other economies have found to experience similar rate cuts as well.

As stated by Greenwaldet al. (2014), the banks have relatively reduced the interest on low and high loans to the valuation ratio and the style ratio. This clearly increased the risk of mortgage among the borrowers. As it has been evident, that the mortgage borrowers are usually ahead of their payment, the borrowers are found to face certain other challenges as well (Odekan 2015). When the borrowers want to make repayment, they are generally found to make offset accounts that include a redraw facility that is used when a new property is used. Therefore, it can be easily said that the prepayments options quickly deplete the increased leverage and create difficult situations among the borrowers at the time of making repayments (Hill and Syed 2016).

If the overall housing loans of Australia are taken into consideration, the role of the Big Four Banks cannot be denied. The dominance of these banks has increased to a great extent because these banks are often backed by the real estate business firms of Australia as well. This clearly indicates the increasing demand of the home loan market and the alternatives to the available lending to the large firms. The home loans have increased to a large extent by almost $8 billion since 2016 in which 39% is the mortgage loan that the Australians pay for their home loans (Rogerset al. 2015). Even in the current high rate of the home loans, the numbers of people who are taking loans are increasing at a rapid rate.

Therefore, there is no doubt that the Banks would not lose their customers in the current situation even if they increase the rate of the loan. However, the pressure created by the lenders and the situations have created such a condition for the borrowers that it has become really difficult for them to consider the situation and tackle the home loans (Jordàet al. 2015). In fact, it has also been observed that the borrowers are facing high level of health issues as well. Thus, there is a clear evidence of the fact that the high rate of home loan and the mortgage rate is indeed a problematic situation for the Australians.

It has to be kept under consideration that the home owners do not only have to pay the loans or the mortgage rate but there is certain other taxes as well that they have to pay as well. The taxation treatment of housing is creating negative impact on the major contributors. As it has been evident that the roaming charges that the Australians have to pay is considerably higher than their expected rate (Wood et al. 2013). This also creates a systematic risk in both the banking sector and the housing market. This has created huge debts on many households as well and the families have to suffer at last. Therefore, there is a great distress from all over the situations. When the home owners are not able to pay their loan back, at the worse situations they are simply thrown out of their houses. This creates worse situations and the property market goes into major speculations without any considerable aspect (Karunarathneand Gibson2014).

Chapter 4: Data analysis and interpretation

4.1 Introduction

In the current section, the researchers have discussed about the data that is being obtained from the secondary sources. Proper interpretation and discussion is being made that will help in the overall process of making conclusion of the research work by fulfilling the overall objective of the research. The researchers have used various relevant charts and graphs that are collected from the secondary sources in order to make proper data interoperation and qualitative data analysis is used for the given section.

4.2 Structure of the market share of the Australian home loan industry

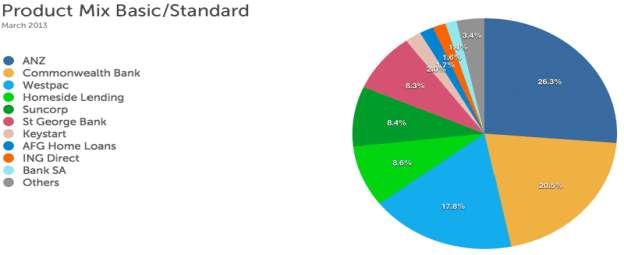

Figure 1: Structure of the market share of the Australian home loan industry in 2013

Source: (Badev et al., 2014)

There are nearly 40 private and public banks that are active within the banking industry of Australia. From the data that is presented above, it is however clear that ANZ bank has been the biggest shareholder in the Australian home loan market. As of financial year 2013 the ANZ Bank at 26.3% of share in the Australian home loan industry which is followed by Commonwealth Bank with a share of 20.5% and Westpac Bank that has a share of 17.8%. Has these three Bank has been the pillar of Australian home loan industry and has occupied more than 50% share within the Australian home loan industry. The Home side Lending group and Suncorp are few of the other major banks with the share percentage of 8-9% (Badev et al., 2014).

It is clear from the above data that there is a tough competition in the Australian home loan industry and the Three major banks have gain a significant competitive advantage that has helped them to capture more than 50% of the home loan market share. These banking institutions has been able to established themselves as one of the reputed organisation to provide home loan the Australian people and is also able to have the power to make significant policy changes within the home loan industry. The business policies that will be implemented by these banking institutions will have significant impact on all the debaters in the Australian home loan market.

It is also evident from the above data that all the other banking institutions in the home loan industry needs to improve upon their loan policy in order to increase the market share and also make significant impact in the respective industry. These minor banking institutions is not able to provide home loans at much quicker rate compared to that of the giant organisations.

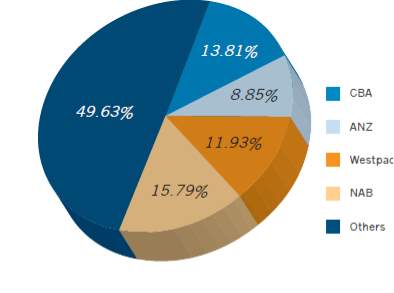

Figure 2: Structure of the market share of the Australian home loan industry in 2015

(Source: Badev et al.,2014)

The above data represents the share of home loan industry in the Australian market in the financial year of 2015. It is clear from the data that NAB is the single largest shareholder in the Australian home loan industry with a percentage of 15.79% that is followed by Commonwealth Bank of Australia with percentage of 13.81%. The ANZ Bank has occupied 8.85% and that of Westpac is 11.93%. Therefore it is clear from the above data that the home loan industry in Australian market has undergone significant changes within the period of 2 years (Badev et al.,2014). The NAB Bank has been able to gain significant improvement within the 2 years and ANZ has lost significant market share due to the fact that they are not able to retain the regular customers.

The Commonwealth Bank and Westpac has also lost significant market share within the 2 years due to the fact that other minor Institutions of Banking industries have been able to make significant changes within the respective industry and is thus able to capture the market share of these banking giants. It is therefore clear that these major banking organisations have not been able to make modification in their policies of loan providing according to the changes of financial criteria and demand of the Australian home loan market.

4.3 Housing index of the Australian Home loan industry

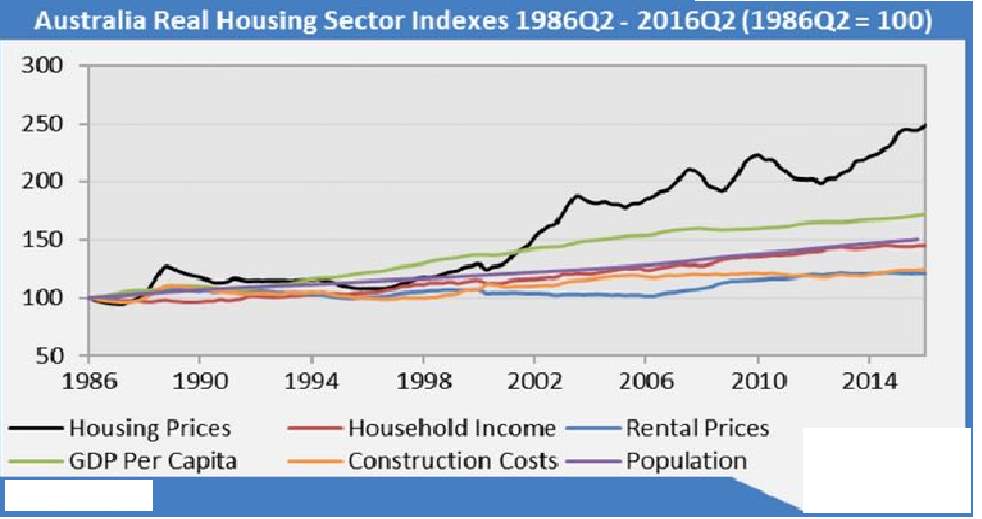

Figure 3: Housing index of the Australian Home loan industry

(Source: Troshani and Rao 2015)

The above data clearly represents the changes in the index of housing sector of Australian home loan Industry that is believed to be one of the major contributors to the growth of the Australian home loan market and also been one of the major reasons for the growth of various organisation and banks within the past 5 years. The data clearly have indicated the Rise of the growth of various sector compared to that of the housing and construction prices that have raised from the year 1986 to 2014. It is clearly evident that in the year 1986 the pricing index of household income was very much similar to the construction cost and Housing prices along with the per capita income of the Australian people. However as the population began to rise the housing and construction cost have raised significantly at a much faster rate compared to that of the total household income or rental prices.

In spite of various ups and downs in the housing sector index within the past 10 years as of 2014 the housing index sector is almost 250 which was just somewhere around 100 in 1986. Hence it is clearly evident from the fact that the cost of housing and construction hasrisen significantly which has been a major challenge for the Australian people to afford their own home within their own financial limit. Hence, they have to depend on financial institution and banking organisation to get the financial support in the form of home loan in order to afford the resident of their choice (Troshani and Rao 2015).

It is also clear from the data that the rental prices have not undergone vast change within the last 20 years as the pricing index have remained somewhere around 100. Therefore it is evident from the data that most of the Australian people with poor financial condition will prefer to stay on rental houses and not to prefer buying their own homes.

4.4 Mortgage lending

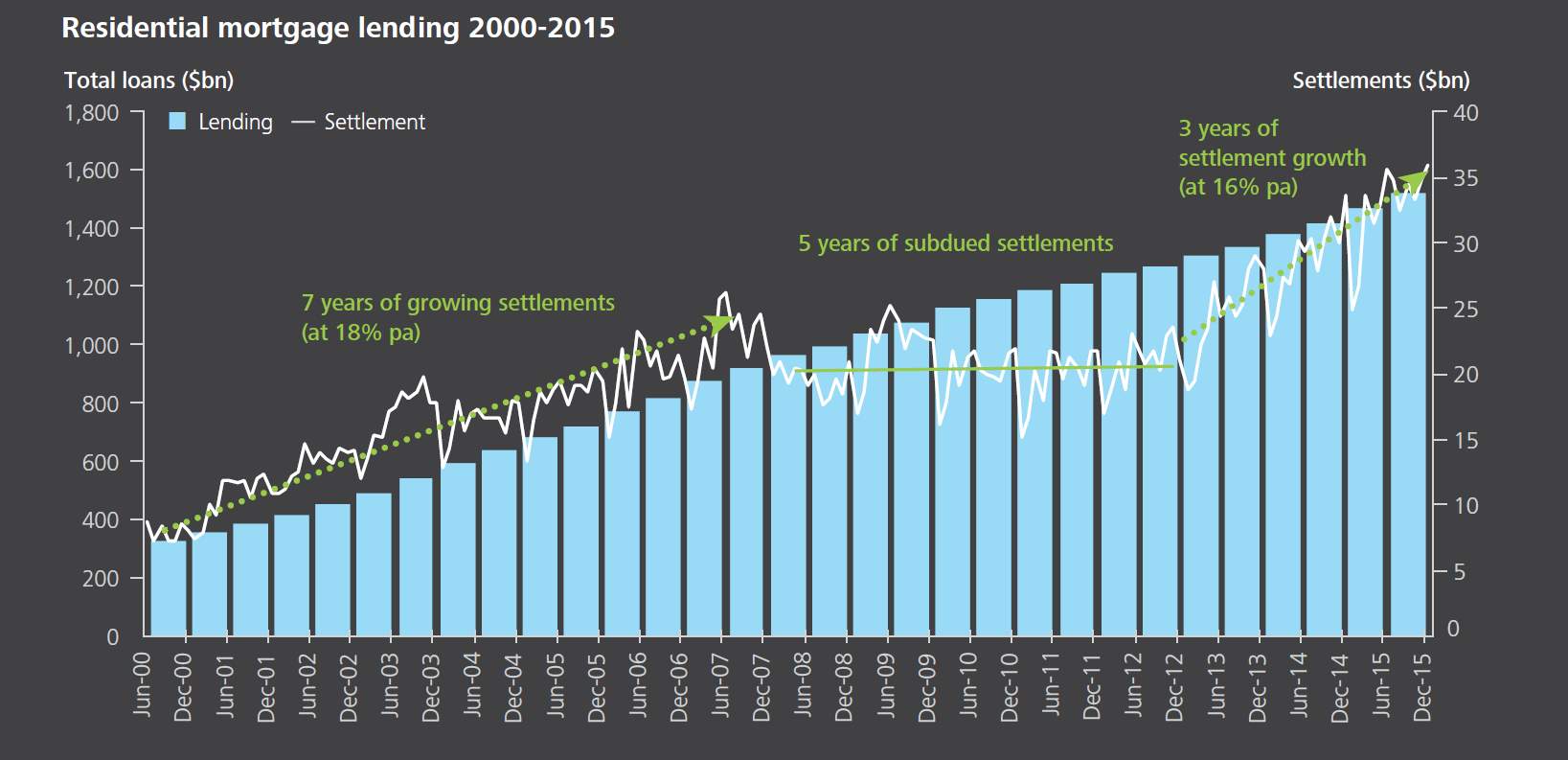

Figure 4: Growth rate in the mortgage amount

(Source: Rogers 2017)

The mortgage market of the Australian home loan industry has been able to continue high delivery rate that has been a major contributor for the growth of the Australian home loan industry and has been able to attract new stakeholders. As of the financial year of October 2015, the total mortgage rates in Australia have increased to 1.5 trillion dollars with the annual growth rate of 7% per annum. The settlement rate has also made a new record with 36 million dollars that is the contribution to 60% of the earnings of all the major banks in the Australian home loan industry. From the given data it is clear that the performance of the mortgage and lending industry have improved significantly within the past 15 years.

However in the middle period of 5 years between 2007 to 2012 due to the global financial crisis there has been subdued settlement in the Australian home loan market and interest rate have remains constant due to the fact that the banking institutions were not able to discover alternative solutions for the financial crisis. However lowering the interest rate and progress in the employment that has raised the level of income of Australian has been the major contributor for boosting up the Australian home loan market from the year 2013 and it has reached the rate of 16% per annum from 2013 to 2015.

Hence, a sharp increase had taken place within these 2 years that is the major contributor of the Rise of the industry. However, it could not fully recover to the rate that was 18% for the first 7 years that is present within the financial report (Rogers 2017).

The data also suggest that few of the major contributors to the growth of the home loan industry includes the unemployment rate, official cash rate and the rate of rise of inflation that has been constant at a rate of 2.5% from the year 2000 to 2016.

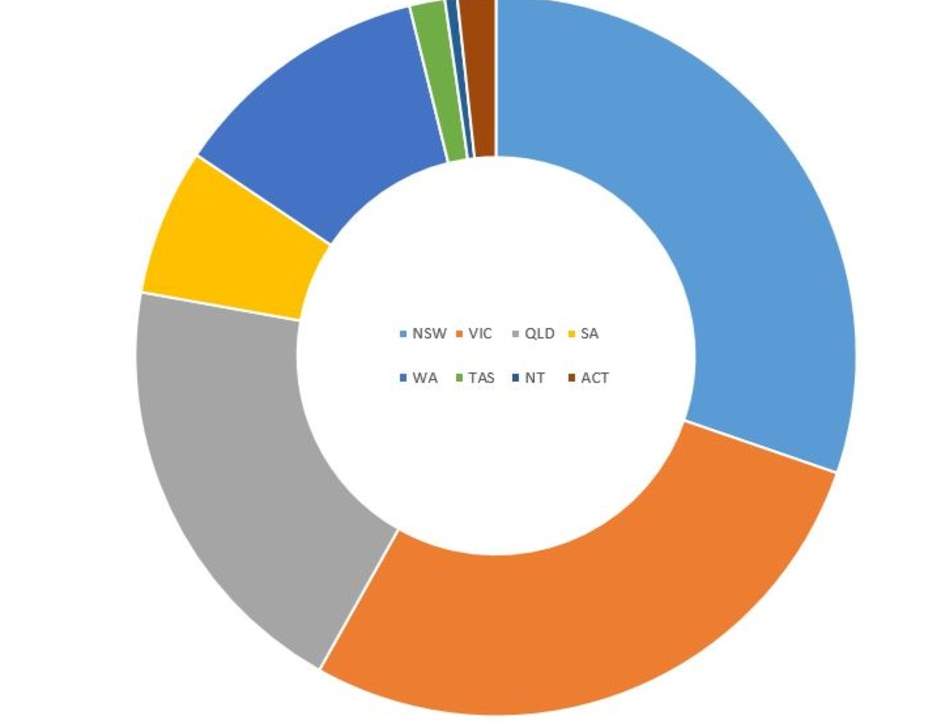

4.5 Home loan distribution of the state

Figure 5: State wise distribution of loan industry

(Source: Bokpin 2013)

The above data represents the distribution of the contribution of various states of Australia in the home loan industry. It is clear that Victoria and New South Wales are the major contributors with percentage occupancy of 30% and 28% respectively (Bokpin 2013). The southern parts of Australia along with Australian Capital Territory are also few of the major contributors within the home loan market. However it is clear that most of the banking institutions and other financial organisation that are contributed in the Australian home loan industry have their base in New South Wales and Victoria which will allow them to have a healthy business and make significant contribution in the Australian home loan industry.

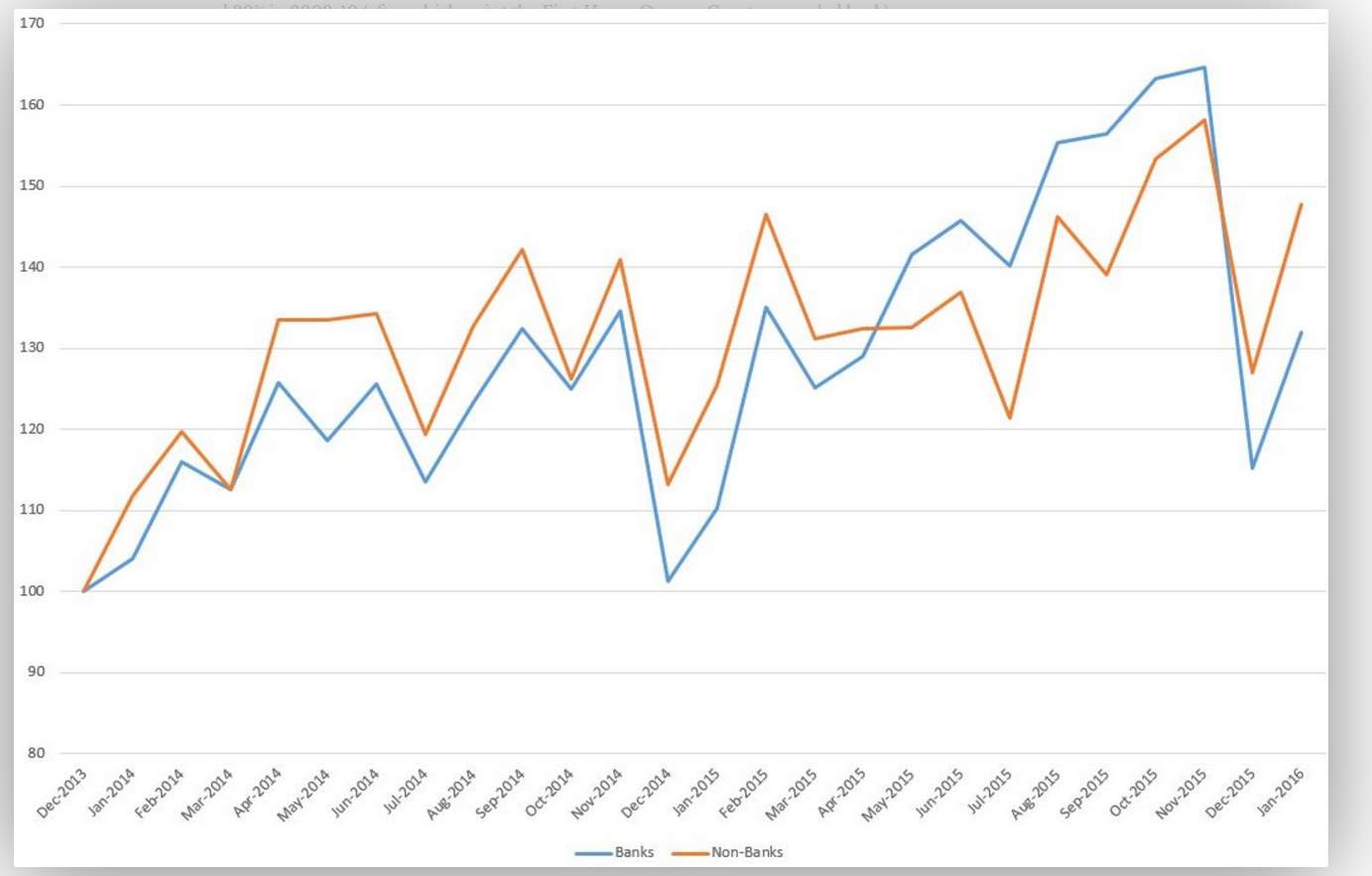

4.6 Contribution of Banks and Non-banks in the home loan industry

Figure 6: Comparison of contribution of bank and non-bank organization in the home loan industry

(Source: Watkins et al. 2014)

It is clear from the above data that the performance of the banks compared to that of the othernon-banking institutions are lower in the Australian home loan market. Therefore in can be interpreted that within the past few years the Australian people are relying more on the non-banking institutions rather than the major banks to get home loans. The lower rate of mortgage by the non-banking institution is one of the major causes that people have switched on to other Financial Institutions in order to get their home loans supply. Moreover due to the fact of lower processing time people are preparing the non-banking institutions to get approval of the home loans (Watkins et al. 2014).

The lower rate of switching cost from banking to other Financial Institutions has increased most of the home loan seekers change their creditor source that will help them to have lower rate of interest and also pay lower rate of interest. However in some cases it has been found that lower rate of switching cost have ultimately resulted in higher rate of interest of the home loans that has enabled the home loan industry to have a sharp change within the last few financial years.

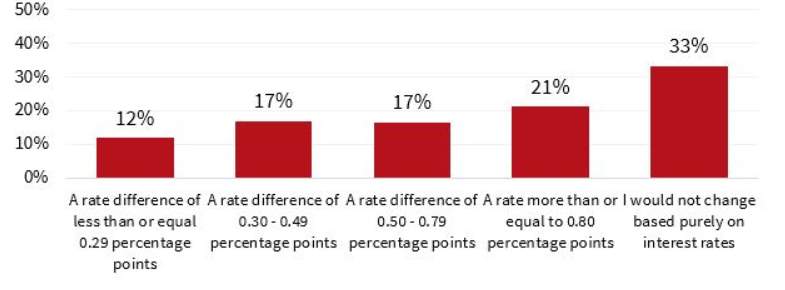

4.7 Major reasons for the switching over of the home loans

Figure 7: Contributing reasons for switching over of home loan

(Source: Yates 2014)

There are various reasons that have contributed for switching over of creditor within the Australian home loan market. From the above data it is clear that lower rate of interest has been the major contributor that has caused 33% of the people to switch over the source of home loan (Yates 2014). Lower rate of percentage difference and also interest rate of individual choice I also few of the major contributors they have encouraged the Australian customer to switch over they are source of home loan.

Chapter 5: Conclusion and recommendations

The analysis made on the home loan market of Australia has made it clear that the country has been facing major issues when it comes to the concerns related to the loan market and the interest rate that they have to pay when they take home loans. The situation has worsened due to the increased power of the Big Four Banks of Australia that have dominated the Australian market largely. It has been found that the major concern related to the home loan is the switching cost that the borrowers have to pay when they switch their home loans. It has been found that at least once or twice in 15 years, Australians shift their home and that requires a shift in their home loan as well. However, the increased rate of interest that the consumers actually have to pay is creating great concerns. It has also been found that the increasing tension among the people is creating health issues among them as well. All these aspects are creating great concerns among the Australians and the government as well. Therefore, there is urgent need of considering certain ways that the government shall made in order to improve the situation.

Recommendations

In order to avoid the extra charges that the consumers have to pay in the name of the switching costs the approach of home loan portability can be taken into consideration. Home loan portability is the feature that is the left over from the mortgages that is used to overcome the exit fees. The fees are charged by the lenders when there is a simple switching of the home loans from the existing loans. This is the process where the consumers are allowed to transfer their loan from the previous one to the new one. There are definitely certain advantages of the same that would eventually help the consumers to combat against the increasing indecency that they have to face when it comes to settling down their loans. With this approach, it would become possible to avoid the break costs at the time of refinancing a fixed rate of the home loan. This is the simple way, when the banks simply transfer the existing loan to the new loan, with proper security. In addition to this, the accounts of the consumers also remain same without any change.

The other means of reducing the risk of the increasing turmoil of the home loan market can be done by allowing a diversification and risk transfer of the banks to the other international banks as well. However, it has to be mentioned here that these approaches were previously made as well but the same was not successful due to the reluctance of dealing with the global crisis. Most importantly, certain policies and regulations need to be incorporated as well in the overall home loan market of Australia that would definitely create a greater dominance in the market and would keep the home loan market confined within the limits of the government policies. This could not be regarded as the failure of the Australian Banks or the Australian economy but serious steps need to be taken in order to shape the existing situation of the home loan market. The market would definitely be competitive but it should not be the reason behind the degrading condition of the market and the challenges that the borrowers are facing in terms of clearing their loans.

References

Badev, A.I., Beck, T., Vado, L. and Walley, S.C., 2014. Housing finance across countries: New data and analysis.

Badev, A.I., Beck, T., Vado, L. and Walley, S.C., 2014. Housing finance across countries: New data and analysis.

Bauer, G.R., 2014. Incorporating intersectionality theory into population health research methodology: Challenges and the potential to advance health equity. Social Science & Medicine, 110, pp.10-17.

Bokpin, G.A., 2013. Ownership structure, corporate governance and bank efficiency: an empirical analysis of panel data from the banking industry in Ghana. Corporate Governance: The international journal of business in society, 13(3), pp.274-287.

Delfani, N., De Deken, J. and Dewilde, C., 2014. Home-ownership and Pensions: Negative Correlation, but no Trade-off. Housing Studies, 29(5), pp.657-676.

Favilukis, J., Ludvigson, S.C. and Van Nieuwerburgh, S., 2017. The Macroeconomic Effects of Housing Wealth, Housing Finance, and Limited Risk Sharing in General Equilibrium. Journal of Political Economy, 125(1), pp.000-000.

Gale, N.K., Heath, G., Cameron, E., Rashid, S. and Redwood, S., 2013. Using the framework method for the analysis of qualitative data in multi-disciplinary health research. BMC medical research methodology, 13(1), p.117.

Greenwald, D.L., Lettau, M. and Ludvigson, S.C., 2014. Origins of stock market fluctuations (No. w19818). National Bureau of Economic Research.

Hill, R.J. and Syed, I.A., 2016. Hedonic price–rent ratios, user cost, and departures from equilibrium in the housing market. Regional Science and Urban Economics, 56, pp.60-72.

Jordà, Ò.,Schularick, M. and Taylor, A.M., 2015. Betting the house. Journal of International Economics, 96, pp.S2-S18.

Karunarathne, W. and Gibson, J., 2014.Financial literacy and remittance behavior of skilled and unskilled immigrant groups in Australia. Journal of Asian Economics, 30, pp.54-62.

Knowles, S., Phillips, G. and Lidberg, J., 2017. Reporting The Global Financial Crisis: A longitudinal tri-nation study of mainstream financial journalism. Journalism Studies, 18(3), pp.322-340.

Lou, W. and Yin, X., 2014.The impact of the global financial crisis on mortgage pricing and credit supply. Journal of International Financial Markets, Institutions and Money, 29, pp.336-363.

Mackey, A. and Gass, S.M., 2015. Second language research: Methodology and design. Routledge.

Meng, X., Hoang, N.T. and Siriwardana, M., 2013. The determinants of Australian household debt: A macro level study. Journal of Asian Economics, 29, pp.80-90.

Moore, T., Horne, R. and Morrissey, J., 2014. Zero emission housing: Policy development in Australia and comparisons with the EU, UK, USA and California. Environmental Innovation and Societal Transitions, 11, pp.25-45.

Norris, M., 2016. Varieties of home ownership: Ireland’s transition from a socialised to a marketised policy regime. Housing Studies, 31(1), pp.81-101.

Odekon, M., 2015. Booms and Busts: An Encyclopedia of Economic History from the First Stock Market Crash of 1792 to the Current Global Economic Crisis. Routledge.

Palinkas, L.A., Horwitz, S.M., Green, C.A., Wisdom, J.P., Duan, N. and Hoagwood, K., 2015. Purposeful sampling for qualitative data collection and analysis in mixed method implementation research. Administration and Policy in Mental Health and Mental Health Services Research, 42(5), pp.533-544.

Panneerselvam, R., 2014. Research methodology. PHI Learning Pvt. Ltd..

Priemus, H. and Whitehead, C., 2014. Interactions between the financial crisis and national housing markets.

Randolph, B., Pinnegar, S. and Tice, A., 2013. The first home owner boost in Australia: a case study of outcomes in the Sydney housing market. Urban Policy and Research, 31(1), pp.55-73.

Rogers, D., 2017. Becoming a super-rich foreign real estate investor: Globalising real estate data, publications and events. In Cities and the Super-Rich (pp. 85-104). Palgrave Macmillan US.

Rogers, D., Lee, C.L. and Yan, D., 2015. The politics of foreign investment in Australian housing: Chinese investors, translocal sales agents and local resistance. Housing Studies, 30(5), pp.730-748.

Shao, A.W., Hanewald, K. and Sherris, M., 2015. Reverse mortgage pricing and risk analysis allowing for idiosyncratic house price risk and longevity risk. Insurance: Mathematics and Economics, 63, pp.76-90.

Stebbing, A. and Spies-Butcher, B., 2016.The decline of a homeowning society?Asset-based welfare, retirement and intergenerational equity in Australia. Housing Studies, 31(2), pp.190-207.

Stewart, C., Robertson, B. and Heath, A., 2013. Trends in the funding and lending behaviour of Australian banks. Reserve Bank of Australia, pp.37-43.

Taylor, S.J., Bogdan, R. and DeVault, M., 2015. Introduction to qualitative research methods: A guidebook and resource. John Wiley & Sons.

Troshani, I. and Rao, S., 2015. Enabling e-business competitive advantage: Perspectives from the Australian financial services industry. International Journal of business and Information, 2(1).

Vaioleti, T.M., 2016. Talanoa research methodology: A developing position on Pacific research. Waikato Journal of Education, 12(1).

Watkins, J.G., Vasnev, A.L. and Gerlach, R., 2014. Multiple Event Incidence And Duration Analysis For Credit Data Incorporating Non‐Stochastic Loan Maturity. Journal of Applied Econometrics, 29(4), pp.627-648.

Wood, G., Parkinson, S., Searle, B. and Smith, S.J., 2013. Motivations for equity borrowing: A welfare-switching effect. Urban Studies, 50(12), pp.2588-2607.

Yates, J., 2014. Protecting housing and mortgage markets in times of crisis: a view from Australia. Journal of Housing and the Built Environment, 29(2), pp.361-382.

Appendix

Fig: Big four standard variable rates comparison

Fig: Rate of Australian houses in Sydney and Melbourne

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "Banking"

Banking can be defined as the business of a bank or someone employed in the banking industry. Used in a non-business sense, banking generally means carrying out activities related to the management of one’s bank accounts or finances.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: