The Decline of the Ghanaian Mining Industry: Lessons from the Rest of Africa

Info: 9913 words (40 pages) Dissertation

Published: 10th Dec 2019

Tagged: EconomicsInternational Studies

Table of Contents

3.3.1 Investment/Development Agreements

3.4 General Economic Environment

table of figures

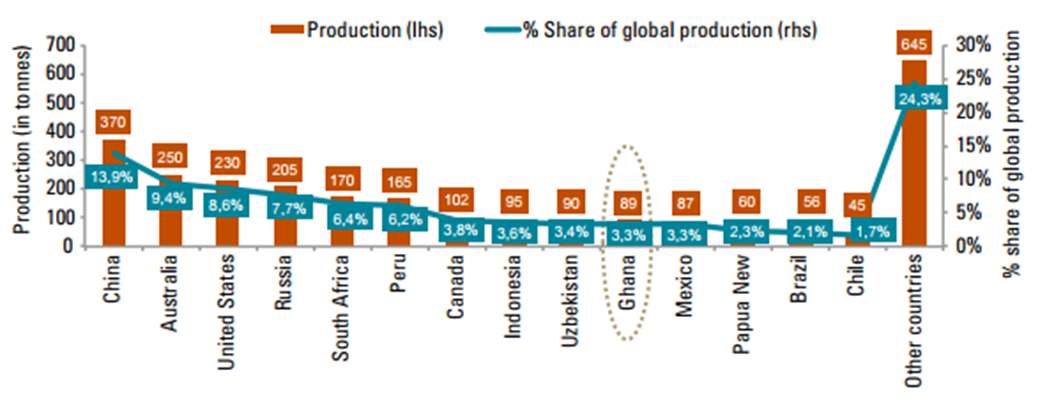

Figure 1: Top gold producing countries

Figure 2: Total Mineral revenues & gold revenues

Figure 3: Top five FDI flows in africa

Figure 4: Employment law legislation

List of tables

Table 1: Noteworthy exploration sites in africa

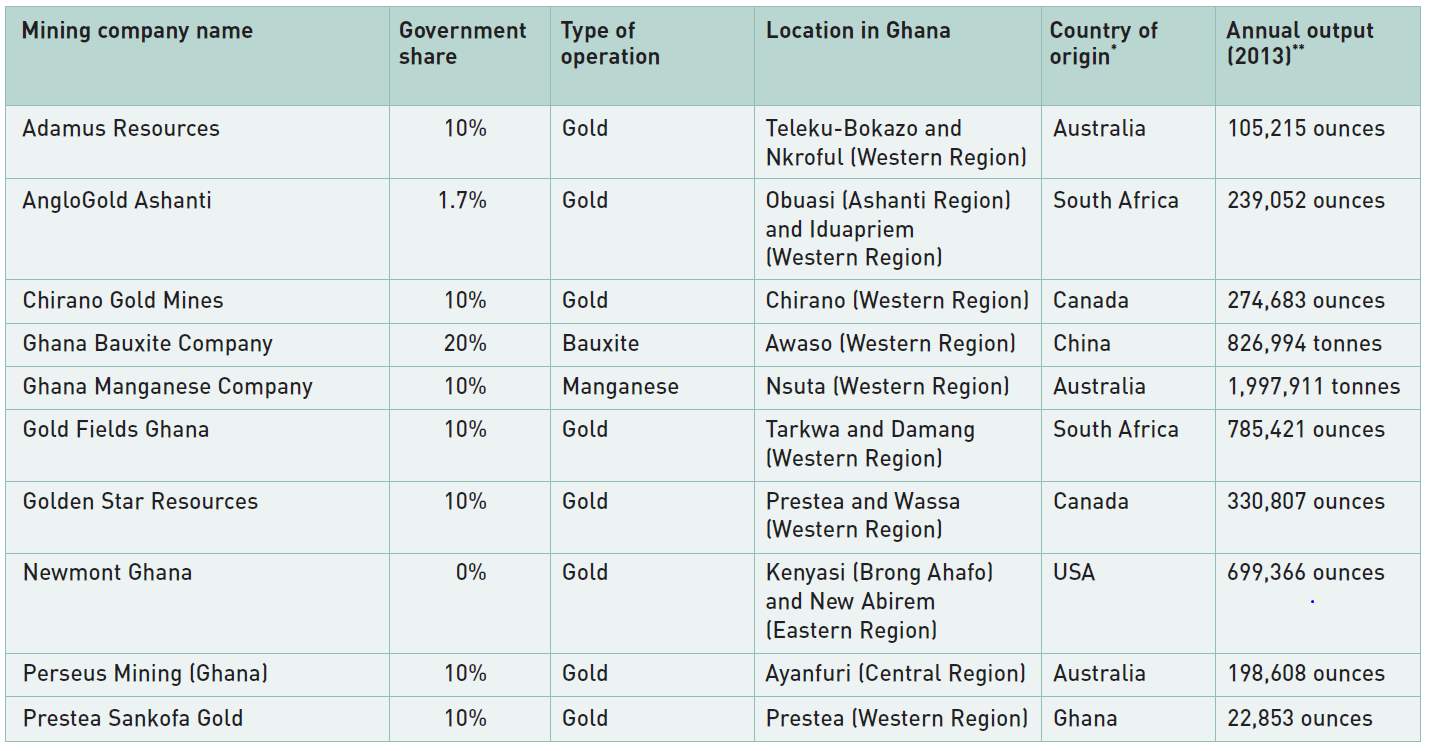

Table 2: Ownership of Major Mining Operating Companies in Ghana

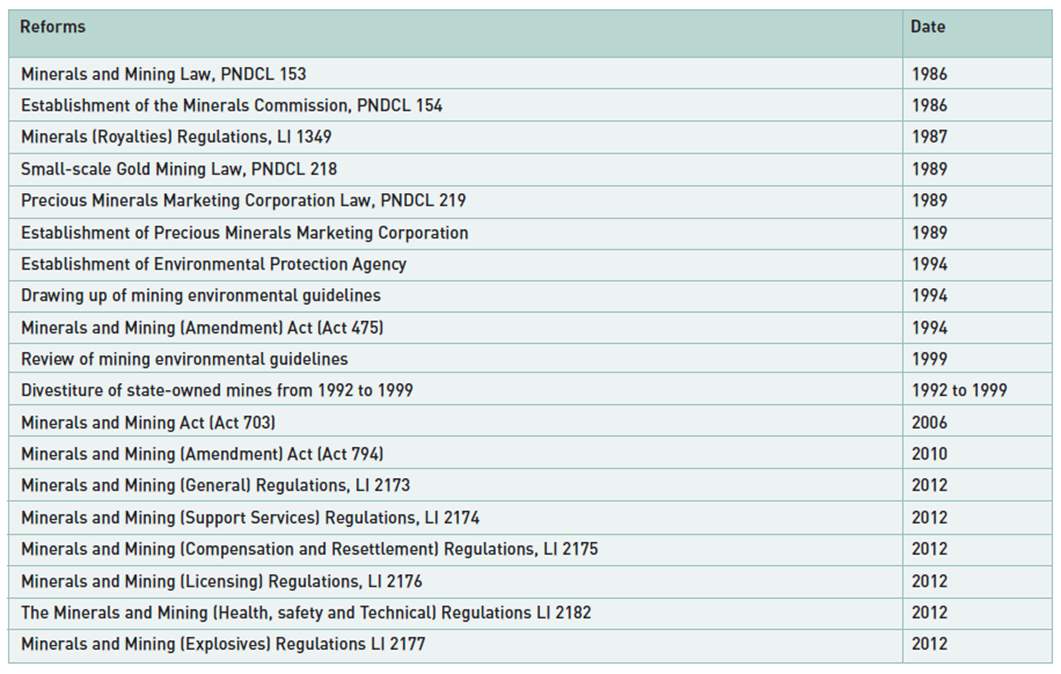

Table 3: Legislation and reforms governing the mining industry in Ghana

Table 4: Comparison of investment environment in Ghana & Côte d’Ivoire

1 Executive summary

This project will take the form of a case study of the Ghanaian mining industry. In particular, the paper will look at the various policy changes made and how investors in the Ghanaian mining industry have reacted to those various changes. In addition, the case study will also look at the same policies across different African countries in terms of which countries have taken the right or wrong approaches in the particular area of interest.

My project took the form of a case study of the Ghanaian mining industry.

In particular, I looked at the various policy changes made and how investors in the Ghanaian mining industry have reacted to those various changes.

Furthermore, I looked at the same policies across different African countries in terms of which countries have taken similar or completely different approaches in the particular area of interest.

And so my project is more of a response from a representative entity in the Ghanaian Chamber of Commerce to the Ghanaian Government and the Minerals Commission in particular.

2 introduction

- Ghana has one of the oldest mining industries in Africa with gold mining as well as the trading of gold with North Africa dating back to the Middle Ages and as a result, various European countries had interests in Ghana (ICMM&GCM 2015). After Ghana became a British Colony in the nineteenth century, it was known as the Gold Coast, due to its abundance of gold. Ghana subsequently obtained independence from the British in 1957, and became the first sub-Saharan colony to do so.

Source: (KPMG 2014)

- Gold continues to be the core of the mining industry in Ghana with Ghana being ranked the 2nd largest gold producer in Africa, and the 10th largest gold producer in the world with 3% of global gold production in 2015 (OBG 2017). In addition, there is large scale mining of diamonds, manganese and bauxite (KPMG 2014). Industrial minerals including brown clays, kaolin, silica and mica have also been mined historically to a lessor extent to supply local industries (OBG 2017). Ghana also has under-explored iron ore, limestone, columbine-tantalite, feldspar, quartz and salt deposits as well as smaller deposits of ilmenite, magnetite and rutile (OBG 2017). Furthermore, recent discoveries in Ghana have highlighted development potential for the mining of copper, nickel, zinc and chromium along with immense potential in solar salt production (OBG 2017).

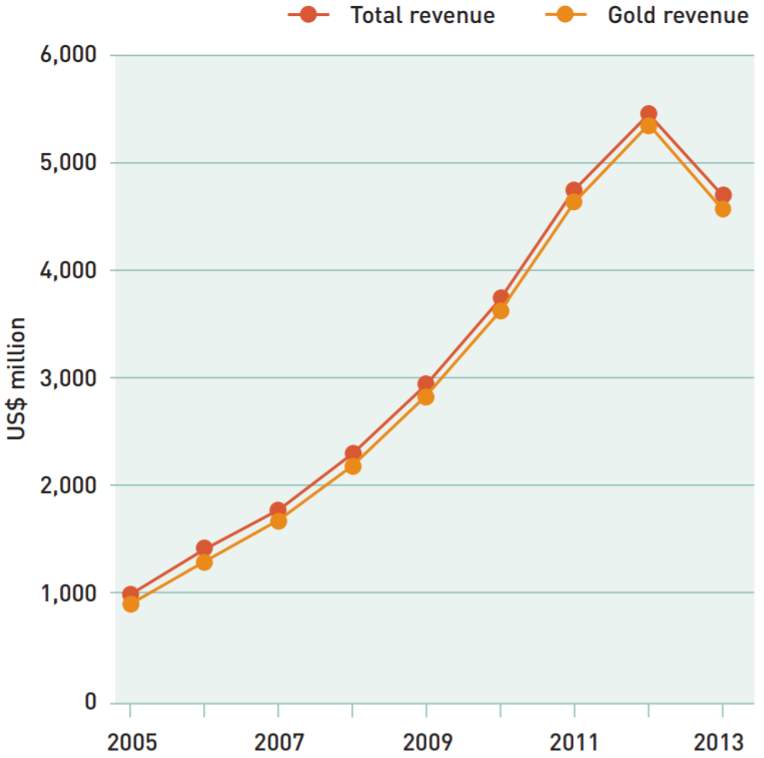

- Whilst numerous minerals are mined in Ghana, gold contributes over 95% of the country’s total mineral revenue (ICMM&GCM 2015), as illustrated by the figure below. In fact, in 2016 gold accounted for 97.3%, manganese 1.9%, bauxite 0.7% and diamonds 0.03% of gross mineral revenue (GCM 2016). Open pit as well as underground mining are the main mining methods utilised in the country, whilst alluvial mining is the main mining method utilised by artisanal and small scale miners (GCM 2016). In 2016 the mining and quarrying sector was the leading source of direct domestic revenue after fiscal receipts increased from GHC 1.35 billion in 2015 to GHC 1.65 million in 2016, amounting to 22% growth (GCM 2016). This represented GHC 399.9 million, GHC 696.6 million, GHC 550.7 million and GHC 0.54 million in pay as you earn (“PAYE”), corporate income tax, royalties and other taxes respectively (GCM 2016).

- Figure 2: Total Mineral revenues & gold revenues

Source: (ICMM&GCM 2015)

Furthermore, the mining industry was the country’s leading export earner in 2016 after increasing its gross merchandise exports from 32.2% in 2015 to 45.4% in 2016 (GCM 2016). Along with slowing down the rate of the Ghanaian cedi’s depreciation relative to other traded currencies in 2016, this increase in mineral export revenue was the key driver for the positive outturn in Ghana’s balance of payments (GCM 2016). In 2016, the producing member companies of the Ghana Chamber of Commerce repatriated 70.9% of their realised mineral revenue amounting to US$2.3 billion (GCM 2016). US$1.8 billion of this was repatriated through commercial banks whilst US$0.5 million was repatriated through the Bank of Ghana, the central bank (GCM 2016).

These member companies utilised 31% of their mineral revenue, US$1.01 billion, on local purchases whilst US$216.8 on consumable imports for the production process (GCM 2016). Member expenditure on local purchases by member increased from 21.4% of mineral revenue in 2013 to 31% in 2016 following a commitment by members to support local businesses (GCM 2016). Member expenditure as a percentage of mineral revenue on diesel and electricity rose from 20% in 2015 to 20.7% whilst employees, capital expenditure and state expenditure represented 13.4%, 13.9% and 9.9% of the realised mineral revenue respectively in 2016 (GCM 2016). Furthermore, member expenditure on dividends to shareholders represented 1% of the total revenue in 2016 whilst US$12.2 million was spent on community development initiatives (GCM 2016). Member entities employed 11,438 employees in 2016 and 98.34% of these employees were Ghanaian with the balance being expatriates (GCM 2016).

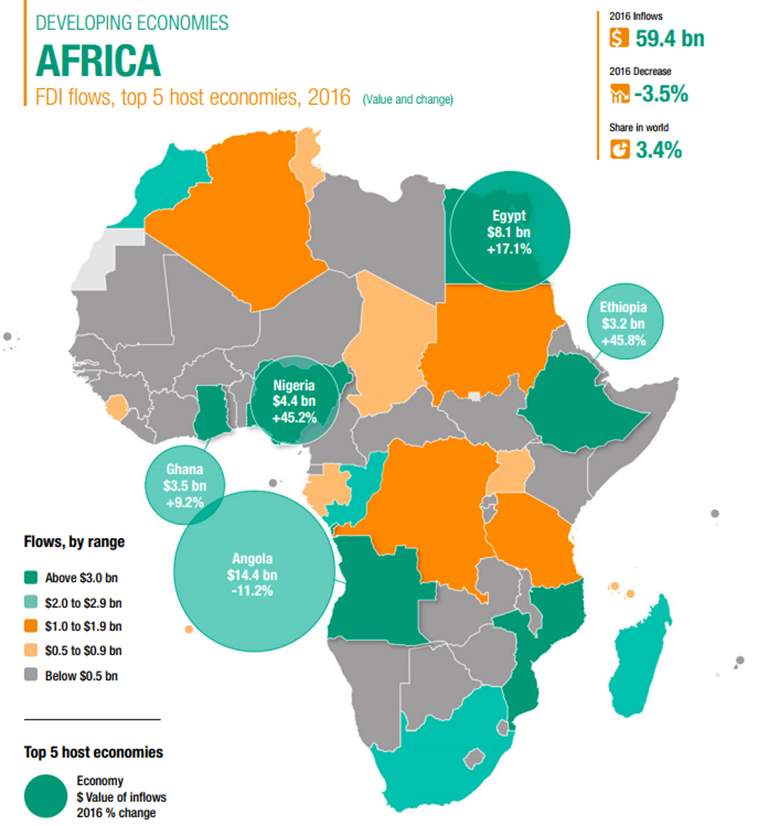

Ghana has been perceived as one of the destinations of choice in Africa for foreign companies wanting to invest in African resources. In fact, Ghana was the 4th largest recipient of foreign direct investment in Africa as highlighted in the figure below.

Figure 3: Top five FDI flows in africa

Source: (UN 2017)

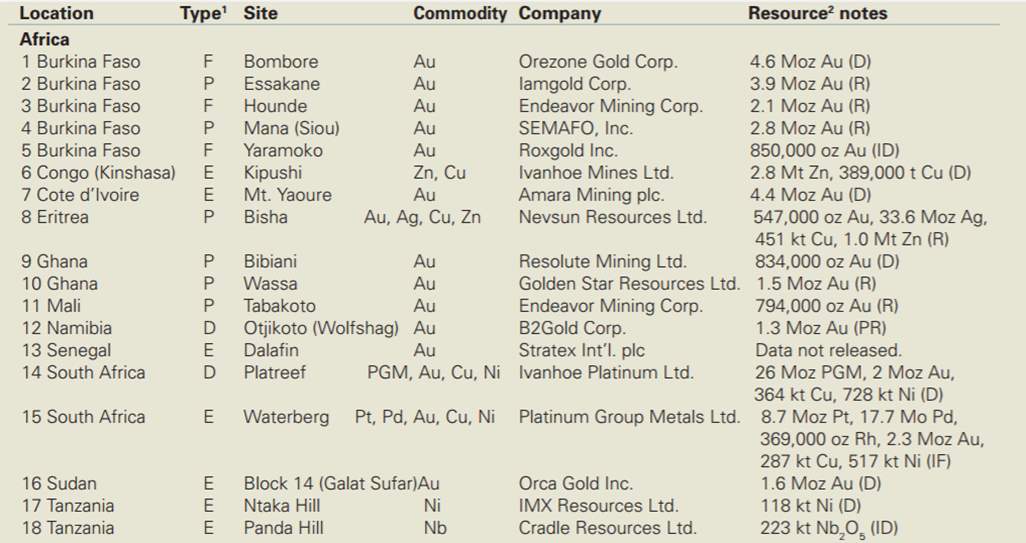

Currently, the Ghanaian mining sector is dominated by large scale foreign owned companies which account for 76% of large scale mining operations, approximately 67% of total Ghanaian gold exports and approximately 80% of total mineral exports (OBG 2017). Early in the twenty first century, West Africa and Ghana in particular, became an attractive place to enter the African mining sector for foreign mining companies but over the last 10 years the landscape within the country has changed dramatically. This is highlighted by the drying up of new greenfield exploration in Ghana as highlighted in the table below.

Table 1: Noteworthy exploration sites in africa

Source: (USGS 2014)

Note1: D – Approved for development; E – Active exploration; F – Feasibility work ongoing/completed; P – Exploration at producing site.

Note 2: Resource estimate as of end of 2103 derived from various 2013 sources: D=measured + indicated, ID=indicated, IF=inferred, R=proven + probable, P= proven, PR=probable.:

- What the above table illustrates is that only near mine exploration has been occurring in Ghana whilst other countries across Africa, including Cote d’Ivoire and the Democratic Republic of Congo, have had significant investment in green fields exploration. This can be considered as an indicator of mining company’s perceived outlook on the unattractiveness of investing in Ghana.

- The main issues contributing to this change in sentiment are to do with the constantly moving “goal posts” in terms of changes in laws as well as changes in the economic environment within the country, especially following the changes in government. These issues are not unique to Ghana, and there are numerous precedents across different countries in Africa where similar changes have occurred and anecdotal evidence of the effects of these changes has been observed. The impacts of various key policies on the mining industry that will be analysed include:

- Ownership (free carry interests, small scale mining and illegal mining);

- Royalties and taxes (attempt to introduce super profits tax and sliding scale royalties for example);

- Mining laws (including stability agreements); and

- General economic environment (includes fuel and power issues, currency and VAT refund issues).

3 key ISSUES

The following analysis and discussion looks at the key issues, highlighted above, in the Ghanaian mining industry along with providing anecdotal evidence of where the same issue has occurred in other parts of Africa and its impact in the respective country.

3.1 Ownership

3.1.1 Free-carry Interest

- In order to understand the ownership structure of the industry, consideration needs to be given to the history of mining in Ghana, which can be considered from two distinct periods. The first period, post-independence until 1983, there was almost 100% government ownership of mining entities, with the former Ashanti Goldfields Corporation being the only exception (ICMM&GCM 2015).

- The second period, post 1983, was when the state implemented the Economic Recovery Programme with the aim of attracting foreign investment, privatisation as well as the sale of state owned enterprises (ICMM&GCM 2015). Currently, the mining sector is predominately foreign owned with the Government of Ghana having a 10% minority free carried interest in the majority of the large scale mining operations (ICMM&GCM 2015). Today the Precious Minerals Marketing Company (“PMMC”), which is a marketing entity for small scale miners, and Sankofa Prestea, which is a gold mining company, are two wholly state-owned companies in Ghana (OBG 2017). Newmont and Anglo Gold Ashanti are also exceptions to this, as illustrated below:

Source: (ICMM&GCM 2015)

There is very minimal local equity participation in the industry with domestic entities only making up 24% of it (ICMM&GCM 2015). On the other hand the small scale mining industry is set aside for Ghanaians, and whist this sector now has a significant share of gold and other mineral exports, as well as obtaining support from the PMMC, artisanal and small scale mining remains predominately unstructured and informal (OBG 2017).

Across Africa there has been a growing trend towards resource nationalisation and whilst this hasn’t been a major risk in Ghana for the moment, there is fear amongst foreign investors into Ghana that this could change in line with this trend. Zimbabwe’s “indigenisation” policy where foreign entities were forced to cede 51% ownership to locals (Economist 2012) is an extreme case of such nationalisation but in recent times, Tanzania has also enacted government minimum non-dilutive free-carry interest of 16% with the entitlement to free-carry up to 50% (PWC 2017).

Whilst free-carry interest and resource nationalisation hasn’t been an issue in recent rimes in Ghana, the fact that it has become a “hot” topic across Africa in recent times contributes to some worry amongst foreign investors. Therefore, Ghana needs to continue to exhibit the stability and steer away from the resource nationalisation theme that is manifesting itself across parts of Africa.

The interesting aspect of the 10% free-carried interest is that there is no real direct financial benefit to the Government in holding this interest unless the company declares dividends and in most cases the majority, usually foreign, parent entity has large inter-company loans that earn interest that is payable before any dividends are even considered. Also, there are bureaucracy issues caused by this free-carried interest that can be quite costly to investor entities in Ghana. For instance, this 10% interest results in these entities being captured by the definition of a “state-owned enterprise” (GMOF 2016) in Ghana’s Public Financial Management Act 2016 which has a wide array of stringent reporting and governance requirements.

Furthermore, that free-carried interest usually results in the requirement of a Government representative on the company’s board and this can cause delays in implementing company strategy or decision making as Government approval is required. For instance, entities would need Government approval for entering into external financing arrangements. There is also the added question of whose best interest a Government representative would be acting in when sitting on a commercial entity’s board as board members are required to act in the shareholders best interest whilst a government representative is required to act in the best interest of the people of Ghana. Therefore, there is a potential conflict of interest in this board representation by a Government official.

3.1.2 Illegal Mining

Furthermore there has been anecdotal evidence of an influx of foreigners with heavy machinery illegally mining within the sector (ICMM&GCM 2015), and this is a key issue as it negatively affects large concessions and non-designated mining areas through invasive and illegal occupation of mining concessions, destruction of farm land, displacement of farmers, pollution of water, increase in crime as well as loss of lives and disruption of social life (OBG 2017). The Ghanaian Government’s response to combat illegal mining was to establish the National Security Committee on Lands and Natural Resources in 2009 as well as the 2016 amendments to the 2006 Minerals and Mining Act, both of which criminalised illegal mining and imposed severe punishments (OBG 2017).

However, these laws have done little to deter illegal mining as it continues to grow. This is evidenced by reported illegal mining invasions at a number of large scale mining operations, including incidents at Perseus Mining Limited’s Edikan mine site, the Owere mine sites in Konongo and Anglo Gold Ashanti’s Obuasi mine site (OBG 2017). Illegal mining in Ghana is deeply rooted as a result of the involvement of chiefs, significant local and foreign investment, an abundance of employment opportunities, and the ineffectiveness of alternative livelihood programmes (Banchirigah 2008), thus making a solution difficult to attain.

Anecdotal evidence across Africa has illustrated that illegal mining can cause significant damage to both the environment, the mining industry as well as the economy in any particular country. Illegal mining in South Africa is a multi-billion dollar transnational industry covering over 6,000 disused mines, employing up to 30,000 people and an estimated 10% of the South Africa’s gold production is stolen and smuggled out of the country accounting for a leakage of approximately R7 billion a year (GRAEME HOSKEN 2017). Thus, illustrating the effects of allowing the illegal mining industry to flourish in Ghana, as it has been over the last few years, will potentially have in that jurisdiction.

When considering the issue of illegal mining, one solution which has been considered is for large-scale miners to relinquish any unused portions of mining tenements (Banchirigah 2008). The argument for this is that this allows the small-scale miners the opportunity to mine on these concessions legally after they have applied for them, as well as being able to apply for support services, such as bank loans, due to having the legal concession as collateral. In addition, the illegal mining issue is largely poverty driven in that individuals are forced into it by not having any alternative choices for their livelihood. And so alleviation of illegal mining should consider creating job opportunities in areas with rampant illegal mining as well as the alleviation of poverty, with one key way of doing so being to ensure that the large scale mining entities’ contributions to Government revenue are appropriately shared with the communities where the mining activities are taking place (e.g. through investing in various job creating industries such as agriculture). Therefore, the Ghanaian Government should consider looking at these solutions in order to help prevent the leakages to the industry caused by illegal mining.

3.2 Royalties & Taxes

3.2.1 Royalties

- The mineral royalty regime in Ghana has evolved over the years and can be traced back to the original minerals act that was propagated prior to independence. After several changes to the royalty regime, the Minerals and Mining Act 2006 (Act 703) provided for a sliding scale royalty of not more than 6% and not less than 3% of the total revenue from minerals obtained by the holder of a mining license based upon the gold price (MMNR 2006). This type of sliding scale royalty regime, is generally superior to a fixed rate royalty regime in terms of allocative efficiency, equity and optimality but it does add some administrative burden (Otto. J et al. 2006). The key reason as to why the sliding scale royalty is far superior to a fixed rate royalty is because it allows for the mining company to be taxed based upon the price of gold and therefore doesn’t suffer from having to pay a fixed royalty regardless of where the price of gold sits. In addition, countries with fixed rate royalties have a history of constantly changing that fixed rate due to a mismatch between the rate and commodity prices, which is a concern for mining companies as there becomes a very high level of unpredictability of a major cost element in their operation. Therefore, the sliding scale royalty regime is a more equitable regime and allows for countries with sliding scale royalties to be more attractive to invest in.

- Due to difficulties in implementation and operation, as well as the public perception that mining companies were paying inadequate royalties, section 25 of the Minerals and Mining Act 2006 (Act 703) was repealed and replaced by the Minerals and Mining (Amendment) Act 2010 (Act 794) which fixed the rate at 5% (MMNR 2010). In 2015 a new Act was disseminated which included a provision that allows discretionary powers to the Minister of land and natural resources to prescribe the royalty rate as well as method of payment. This new Act was the Minerals and Mining (Amendment) Act 2015 (Act 900) (MMNR 2015). The royalty rate as well as method of payment has not yet been officially published or legislated by the Minister of land and natural resources, and since the Act was implemented mining companies continue to pay the royalty rate of 5% of mineral revenue, while a few entities pay a sliding scale royalty as set out in their individual investment agreements with the Government.

- The amendment of the royalty regime coincided with a period of increasing commodity prices and therefore, in the short term this change resulted in increased Government revenue from royalties. However, the medium to long term effects are distorted by the fact that this royalty regime does not discriminate between healthy and marginal mines and is inefficient in responding to changes in commodity prices as Government would have to change the fixed rate in such a situation.

- A fixed rate royalty means that the only additional revenue that could be realized during a commodity price boom will only emanate from an increase in mineral revenue as opposed to a sliding scale royalty where additional revenue will be a function of both the relevant royalty rate as well as mineral revenue. Furthermore, a fixed royalty rate is detrimental to mining companies during low commodity price periods and is detrimental to the Government during high commodity price periods and as a result, a number of mining jurisdictions in Africa are gradually shifting away from fixed rate royalty regimes to sliding scale royalty regimes.

- Whilst only for a select few mining companies with investment agreements, the adoption of the sliding scale royalty regime based on commodity prices for those entities is a step in the right direction as it takes into account the volatility in commodity prices and also stabilises the Government’s fiscal regime and revenue flows. However, the application of the sliding scale royalty regime to a select few mining entities distorts the revenue stream from the mining industry to the Government and results in a situation where mid-tier mines, who pay the fixed rate royalties and more often than not are higher cost producers, are more heavily taxed than their larger counterparts.

- As a result of this, marginal and mid-tier mining producers are not encouraged to partake in investment in exploration to extend mine life or spend on mine development by the current situation, which is to the detriment of the sustainability of the Ghanaian mining industry. This is because the mining industry in Ghana will become focused on high-grade mining which could lead to the sub-optimal development and utilization of the country’s rich mineral endowment. High grade mining is where mining concentrates on extraction of high grade ore only, leaving ore which in the right fiscal environment could be mined to the benefit of stakeholders. This situation violates the taxation principle of equity and is also a sub-optimal instrument for appropriating royalty revenue as the Government will not fully realize mineral revenue to its maximum potential.

- In addition, the state is penalizing the mid-tier and marginal producers during low commodity price periods. In the long run, there will be a reduction in much needed developmental projects to supplement or extend the life of existing mines as mining companies will choose to invest their capital in other mining jurisdictions that have lower and more equitable royalty rates.

- It has been highlighted above that a sliding scale royalty regime is superior to a fixed rate royalty regime in respect to economic allocative efficiency and responsiveness to volatile commodity prices. This position is not only proven by the Ghanaian Government’s four/five attempts to increase its mineral royalty in the last six years but is also supported by economic theory. It has been noted that the state has recently been implementing a sliding scale royalty regime for mining companies with develop investment agreements but the non-uniform application of this will have distortionary effects on government revenue, and hinder the investment of capital in the mining industry.

- Therefore, it is recommended that the Ghanaian Government even out the royalty regime for the mining industry by prescribing the same sliding scale rate for mineral producers. The rectification of this short-coming will strengthen and enhance the Ghanaian Government’s efforts to attract investment into the mining sector, as well as generate significant mining induced multipliers to boost both economic and social well-being.

3.2.2 Taxes

- It has been found that some of the provisions of the Income Tax Act 2015 (Act 896) are confusing, whilst other areas enforce requirements which will adversely affect the viability of mining companies in Ghana by attempting to tax non-existent profits. In order to maintain a viable mining industry it is recommended that the specific provisions relating to mining companies in Division II of Part VI of the new Tax Act (GRA 2015) be withdrawn or suspended to allow for adequate consultation with mining industry participants to remove inadvertent consequences. The failure to remedy these issues promptly is will lead to mine closures in Ghana and is a significant barrier to new mining investment. Some of the key areas of concern have been highlighted in the sections that follow.

-

3.2.2.1 Ring fencing

- Division II of Part VI of the Income Tax Act 2015 (Act 896), relating to minerals and mining operations, contains “ring fencing” provisions which mandate the artificial creation of separate “mineral operations” based upon individual areas of interests (individual mining concessions or tenements) (GRA 2015). These clauses are both inequitable and in some cases very difficult if not impossible for mining companies to comply with from an allocation of costs perspective. There are many issues identified which have been elaborated upon below. The notion of separately accounting for income and expenses of these artificially segregated components of a producing entity, as well as not being able to offset profits or losses between those artificial divisions is inequitable, non-commercial, unjustified and unsustainable.

Firstly, the historical costs have not been recorded utilising this methodology required by the legislation, and therefore accurate profit determination becomes very difficult if not impossible. Furthermore, the legislation does not provide any guidance or transitional provisions to allow mining entities to know how this legislation is to be applied to the historical data to get to a starting position. For example, consider a mining entity that from the time of its feasibility study had planned an operation consisting of multiple pits on three adjoining mining leases that provides ore to a central processing plant. The granting of the three mining leases were grounded upon the economics in that feasibility study. This highlights how inequitable and impractical to now require that the concessions and in fact the areas of interest that they hold be treated as separate “mineral operations” which are required to be taxed as separate entities, because such a change would significantly change the economics of the project and would require a completely different feasibility study to that which was originally completed.

- There is a fundamental flaw in the concept within this legislation that each “mining area” declared by the mining company with the approval of the Ghanaian Minerals Commission be treated as a separate entity. “Mining areas” within a mining lease are constantly changing and are usually declared progressively over time as the mining operations develop, the mine plan changes (for example due to changes in commodity prices or technological advancements) and new resources are identified from near mine exploration, even though it was planned from the beginning that all of the areas of interest would be mined. Furthermore, a mining area could be comparatively small and might only be subject to mining activities for a relatively short period of time making the requirement in section 78(3) of the Act that each mining area declared within a mining lease and any residual area in the mining lease be taxed as separate “mineral operations” (GRA 2015) is completely artificial, unworkable and inequitable.

- Also, in reality a processing facility would never be viable if it was to only process ore from the particular area of interest on which it is located and so it is inequitable that the Act tries to artificially segregate parts of an integrated operation with the aim of creating a taxable situation in one area while creating losses in others. The aim of introducing such legislation is also unclear.

- The Act results in the creation of multiple separate artificial “mineral operations”, and each of them would require a separate tax return. This creates an immense administrative burden of having to record information for each mining area of interest separately, and the resultant tax consequences will be devastating for the industry. For instance, section 81(1)(b) of the Act and section 6 of the Third Schedule requires the allocation of every expense of the mining entity across each of the separate “mineral operations” (GRA 2015), which is not only extremely expensive but also immensely onerous. There is also the issue of the incomprehensible result that this will create.

- On the topic of how costs incurred before the introduction of ring fencing are to be allocated to each artificial “mineral operation” when the existence of the artificial “mineral operation” was not known when the expense was incurred, there is the question of the treatment of historical exploration costs. Exploration is broadly carried out across an entire mineral concession or tenement. The location of each element of exploration on a particular mineral concession such as each drill hole, soil sample or geophysical survey is not necessarily tied in to an exact area of interest on a mineral concession, and recording such information on a location basis is extremely costly without the added benefit and impractical. Therefore, it will be difficult to accurately assign such costs to each artificial “mineral operation”, and there is no benefit of doing so to mining entities making such tax compliance an additional cost that Ghanaian mining operations will have to bear.

- In section 6(4) of the Third Schedule it is stated that where capitalized expenditure such as exploration which is partly used in more than one artificial separate “mineral operation” then “the Commissioner-General shall apportion the capital allowance of that asset in that year between the two separate mineral operations in proportion to the use of the asset in each separate mineral operation” (GRA 2015). In many cases, exploration costs will have to be allocated across multiple artificially created “mineral operations” and so it is of concern that the Commissioner-General’s allocation may result in the mismatch from some of the legislated five-year capital expenditure write-off and the shorter than five-year income from all such “mineral operations” as highlighted in the capital allowances section below.

- There is also the question on how are expenses such as stool fees or mining concession will be applied over the various “mineral operations” within the concession. If this is done on an area basis, then a deduction will only be available for the part of the fees or rent relating to active declared areas of interest. The fees or rent relating to the area outside the declared area of interest would not be an available offset, as there would be no income attributable to those areas. In summary, the “mineral operations” in an area of interest that are not profitable will lose their proportion of tax deductions. Thus, the effect of this legislation is that only a part of the expenses of the entire mining operation will be deductible and this is a major disincentive to investors into the Ghanaian mining industry.

- Furthermore, the requirement in section 77(5) that “arm’s length transaction” pricing rules be applied between individual artificial “mineral operation” (GRA 2015) will create tax anomalies and administrative issues. In most cases an “arm’s length” price for toll treating ore between separate artificial “mineral operations” would be higher than what could be sustained in an single combined mining operation comprising multiple pits. An “arm’s length” processing price would result in the individual artificial “mineral operations” recording losses whilst the mineral operation holding the processing plant recording a profit. That scenario is not sustainable especially because of the inability of applying deductions at the loss making artificial “mineral concessions”.

- The notion set out in Section 77(b) that transfers of assets between the artificially defined “mineral operations” on the same mineral concession but different areas of interest as asset disposals (GRA 2015) is inequitable and creates immense administrative burdens as well as costs.

- These provisions from the recently legislated Act suffer from a lack of clarity and the absence of guidance from regulators makes it extremely difficult for mining companies to know what records they must keep in order to comply with the legislation as well as how to apply this legislation. However, what is clear is that additional guidance on the application of these clauses will not be able to remedy what is essentially fundamentally flawed legislation, and so a review of the legislation after proper consultation with the mining industry is required

3.2.2.2 Deemed disposal of mineral rights

- Public listed entities on a stock exchange should be treated as a single shareholder and shouldn’t be subject to the look-through provisions that are contained in section 83(2), which deem a part disposal of a mineral right with tax consequences whenever 5% or more of the “underlying ownership” of shares in a mining company change (GRA 2015). It is inequitable for this provision to apply to changes in the shareholding of a publicly listed company which owns a Ghanaian mining entity, as the listed entity does not have control over movements within its share register. As a result of this provision a Ghanaian mining entity is subject to a tax liability and/or a loss of future tax benefits, even though there is no disposal of an asset by entity. There is ambiguity from the legislation whether the 5% threshold applies to a single disposal event or is to be considered cumulatively over time, but in either case the threshold is extremely low for mining entities, and shouldn’t apply to shareholder changes in publicly listed parent entity shareholders of mining entities.

- This provision alone is probably sufficient to deter foreign publicly listed entities from investing in the Ghanaian mining industry due to its flow on effects. Mining entities whose direct or indirect shareholders include publicly listed companies will not always know when there are changes in underlying ownership, and therefore will not be able comply with the reporting requirements contained in section 83(3), thus exposing them to the sanctions outlined in section 83(4) (GRA 2015).

- The following illustrates the possible effect of this deeming provision in section 83(2). Section 83(2) requires that a 10% change in the shareholding of its publicly listed 90% shareholder, results in a Ghanaian mining entity to be deemed to have disposed of 9% of its interest in each of its mineral rights, including mining concessions, exploration licences and reconnaissance licences, for the higher of the consideration which is equal to the amount received arising from the change of ownership; and the market value of the proportion of the right treated as disposed of (GRA 2015).

- Furthermore, due to the ring fencing provisions in the Act that were highlighted above, it is probably required that the market value to be divided between the relevant mining concessions, and possibly even further into each individual “mineral operation” that makes up the area of interest, as individual taxable entities.

- The publicly listed shareholder of the Ghanaian mining entity most likely has a number of assets and investments in companies that own many different mining permits, in a number of countries, and it will have both project and trading liabilities. An attempt in the allocation of the consideration received on the sale of the publicly listed shares between all of those assets including the mineral rights of the Ghanaian mining company would be immensely complicated as well as meaningless. As a result, by default the market value provisions of the Act will probably apply.

- In any case, section 83(2)(b)(i) seems to require that the entire consideration received from the sale of the shares by shareholders of the listed shareholder, without any adjustment for the other assets of the listed shareholder, would be taken to be the deemed consideration on the 9% deemed disposal of the mineral rights (GRA 2015). This ignores all of the other assets of the publicly listed shareholder and overstates the value of the consideration and will result in adverse, punitive tax consequences.

There is an implication in section 83(2)(b)ii) that there is a obligation for the mining entity to calculate the market value each of its mineral interests each time there is a 5% disposal of the shares in its publicly listed shareholder (GRA 2015). An independent, or even an internal, valuation of the mineral rights can be a very long and drawn out process as well as very costly and so this implied obligation is extremely onerous on Ghanaian mining entities. This is because of the underlying work that would be required in assessing resources, reserves, costs, the mine plan amongst other valuation considerations. This obligation is untenable where there is a public listed shareholder as regular changes of 5% or more can occur frequently in the shareholding of any publicly listed company.

- What is unclear from the legislation is if improvements, such as upgrades to the mine processing plant located on a mineral right, or other expenditure, such as exploration, can be included in the valuation or the cost base of the asset deemed to be partly disposed of. However, as it is the deemed disposal of a “mineral right” and not the deemed disposal of a “mineral operation”, it appears that these cannot be included in the valuation or the cost base of the asset deemed to be partly disposed of but guidance on this is something that the regulator should consider. In most cases the only direct cost of acquiring a mineral right would just be the application fees, and so there might be very little cost if any to offset against the deemed disposal value of the mineral right under this clause. And therefore, clarity is required on the cost base to be applied on the deemed disposal of the mineral right. Further to this, when different valuation methods are utilised there can be significantly different results and so clarity around the valuation method(s) allowed is recommended.

In conclusion, the allocation of the consideration across different “mineral operations” within a mining concession will be arbitrary and could further create artificial results to the detriment of entities in the Ghanaian mining industry. As a result, mining entities will either find themselves with tax liabilities for artificially deemed disposals of mineral rights due to shareholders in its ultimate holding company selling some shares on the stock exchange, or they will suffer a reduction in the tax carrying value on the mineral interests which it can carry forward to obtain a future tax benefit.

- In addition, the mining company may not be able to identify all share transactions by its shareholders, as shareholding is not always opaque such as in the instance of the use of nominee companies, making it difficult to comply with the disclosure provision of section 82(3), thus potentially exposing companies to penalties.

- Therefore it is recommended that a listed public company shareholder be treated as one shareholder in determining underlying ownership changes. Furthermore, if this deemed disposal provision is to remain, in any form the 5% threshold should be increased significantly so as not to make implementation so onerous and costly, and the various issues discussed above on valuation, cost base, to name a few, should be addressed.

3.2.2.3 Capital allowances

- Section 14 of the Act and the Third Schedule states that certain capital expenditure items are to be capitalised and written off over five years for tax purposes (GRA 2015). This five-year write-off was envisioned to be a concession to large taxpayers who purchase long life assets especially, but there are cases where the benefit from an asset is realised over a period that is shorter than five years. And so this requirement to write-off assets over five years will result in a mismatch between income and expenditure if the use of those assets is over a period of time that is less than the five years prescribed. Therefore, to allow proper matching of expenditure to income, capital allowances should be allowed to be written-off over the lesser of the prescribed five years or the period during which the benefit from the use of those assets is obtained.

- An example of where such a mismatch can occur which is the writing-off of capitalised stripping costs or exploration expenditure for a pit which will be mined over a period of less than five years. Income will only be generated from mining the pit for that less than five-year period, whilst the associated costs would be written off over the prescribed five years. This can cause significant discrepancies in net present value valuations as well as resulting in inequity in the payment of taxes by mining companies.

- The ring fencing provisions mentioned above compound this issue due to restricting the write-off to the specific mining area of interest, resulting in expenditure not being able to be claimed for tax purposes.

3.3 Mining Laws

3.3.1 Investment/Development Agreements

- Section 49 of the Minerals and Mining Act 2006 states that a development agreement may be entered into between the Government of Ghana and the mining entity providing benefits to the mining entity where the proposed investment by that mining entity will exceed US$500 million (MMNR 2006). The act does not clearly define what a “proposed investment” is and what expenditure it covers. In particular the legislation does not elaborate on whether a proposed investment includes the building of a processing plant for a particular project only, or if it includes the mining infrastructure and pre-stripping, or if it includes historical exploration expenditure related to that particular project in question. Therefore, should this minimum spend remain intact it is recommended that this ambiguity be clarified in order for foreign investors to be able to make appropriate decisions on investing into Ghana.

In addition, other African entities such as Côte d’Ivoire do not have any such minimum capital spending requirements before an entity can enter into an investment/development agreement with the Government of that country. This makes countries such as Côte d’Ivoire far more attractive for foreign mining investors as there isn’t the added burden of having to spend a minimum of US$500 million before entering into an investment/development agreement with the Government of the country they would like to invest into. Thus, due to this added fiscal security, protecting foreign mining companies from changing laws (which can change frequently as seen from the table below of changes in mining laws in Ghana), without having a significant minimum capital spend imposed on them makes these countries a far more attractive investment country than Ghana and it is recommended that this minimum spend be abolished entirely.

Source: (ICMM&GCM 2015)

3.3.2 Localisation Plans

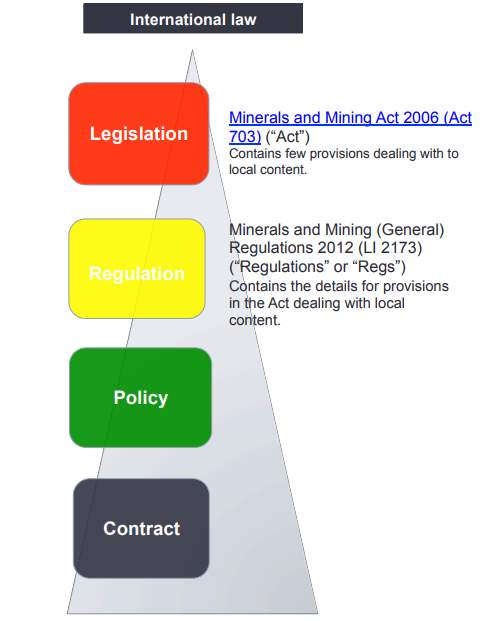

- The Ghanaian Minerals and Mining Act 2006 as well as the Minerals and Mining (General) Regulations 2012, illustrated in the figure below, both contain clauses related to localisation and local content requirements in Ghana. Section 1(1) of the Minerals and Mining (General) Regulations 2012 states that with “an application for a mineral right, a licence to export or deal in minerals or to provide mine support services under the Act or any Regulations made under the Act shall be accompanied by particulars of the applicant’s proposals with respect to the recruitment of expatriates and employment and training of Ghanaians” (MMNR 2012). Furthermore, section 1(12) states that “on commencement of the Regulations an entity registered to provide mine support services shall submit for approval a program for training and recruiting Ghanaians and maintain expatriate staff as specified in the Second Schedule” (MMNR 2012).

- Thus, as stated above, Government of Ghana imposes restrictions on expatriate work permits through limiting them to providing training opportunities for local employees. This limitation results in issues in attracting and retaining skilled employees in the country, as well as providing adequate training for local employees. Thus, posing risks to both operations as well as safety for foreign owned entities operating in Ghana. The significant penalties imposed by the Minerals and Mining (General) Regulations 2012 means that this this area remains a concern for foreign mining entities, and this should be considered as an area for review as there aren’t such stringent requirements amongst some of Ghana’s peers across Africa.

Figure 4: Employment law legislation

Source: (CSSD 2016)

3.4 General Economic Environment

3.4.1 Value Added Tax (“VAT”)

- There continues to be an issue of non-recovery of VAT paid by mining companies to the Ghana Revenue Authority and this has been an ongoing serious problem impacting on working capital, cash flows and thus the viability of entities operating in the Ghanaian mining industry. The VAT receivable is denominated in Ghanaian Cedis and therefore non-receipt of VAT credits going back over 18 months if not more for some entities heavily impacts cash flows and exposes mining companies to large foreign exchange losses associated with the rapidly devaluing Ghanaian Cedi.

- In addition, the Ghanaian Government has stopped issuing treasury credit notes which were allowed to be applied against other taxes, and this has intensified the problem. There has also been a historical practice of not allowing a VAT refund until an audit of that VAT receivable is completed, and then delaying VAT audits which causes significant cash flows issues for miners especially the marginal producers. There have been precedents of nine months before a VAT audit is conducted and accepted and then a further year before it is paid, which is a significant amount of time for any entity to have to wait for the recovery of a receivable. This uncollectible VAT as well as the devaluation that occurs whilst waiting for its recovery effectively becomes another major business expense, and is a significant investment deterrent for foreign entities wanting to invest into Ghana.

- Further to the VAT recoverability issues highlighted above, the VAT regime in Ghana is also a significant disincentive to exploration and development progression within the country. Legislation in Ghana requires the charging of 17.5% VAT on exploration, mine development and mine operating costs. This VAT charged on exploration and mine development is then only recoverable from the Ghana Revenue Authority four months before production starts following development. Thus, before the recovery of this VAT, it is in effect an extra 17.5% cost imposed upon exploration and developing entities, thereby making it very hard to finance new projects. This fact is therefore a significant disincentive to new investment in Ghana, for both the development of projects as well as exploration. In comparison, no VAT s charged on exploration, mine development or mining operating expenses in Côte d’Ivoire. Ghana’s VAT imposition on mining and mining related entities has also resulted in the reduction of for Ghanaian drilling, geological and mining consultancy entities.

- In recent times, the Government of Ghana has also begun a new initiative to enforce payment of VAT and customs duty on mining imports thus further exasperating the problem and adding to the disincentives for foreign entities to invest into Ghana. It is therefore recommended that the Government of Ghana reverse its policy of collecting customs duty and VAT on mining industry imports at the port, as well as provide exemptions for the payment of VAT by mining and mining related entites for all activities including exploration, mine development and mining operations. This will allow Ghana to be more competitive with its African peers and not be left behind in the race to attract foreign investment into mining in the country.

3.4.2 Fuel

- Power supply in Ghana is very erratic and many of the mining operations are heavily reliant on diesel powered generators as either the main source of power or as back up for when the main grid is down. Therefore, the price of fuel is an important and significant factor for mining operations. Therefore, the significant increases in the price of fuel in Ghana, such as the GH¢ 0.85 per litre (US$0.21 per litre) increase in the fuel tax that was effective from 1 January 2016 poses a significant increase in costs to entities in the Ghanaian mining industry. This significant increase in the price of fuel will also have a follow-on effect on costs such as power and transport which will also negatively impact Ghanaian mining entities.

- This fuel tax increase also included an increase in the Road Fund Levy from approximately 7 pesewas to 40 pesewas (approximately US$0.04 to US$0.10). However, it can be argued that this levy shouldn’t apply to mining entities whose operations are in remote sites and not on public roads. Other mining jurisdictions in Africa provide this exemption to mining entities. For example, Côte d’Ivoire has an exemption from duties on fuel used in mining operations and therefore such an exemption in Ghana would aide in making Ghana continue to be a favoured destination for mining investment

4 conclusion

- The above analysis has highlighted some of the key areas. That the Ghanaian mining industry is being left behind by some of the other jurisdictions across Africa. Recommendations have also been provided across the various areas in order to encourage foreign investment to continue to flow into Ghana’s mining industry so that it continues to be perceived as a mining destination of choice. The recommendations cover a range of issues, but all are grounded upon the Government of Ghana implementing laws and policies that encourage investment as opposed to deterring it. Furthermore, it is encouraged that the Government of Ghana consult with industry before implementing these policies in order to get insight from all stakeholders to assess the impact of these policies as well as ensuring that they result in the attaining of the Government’s objectives.

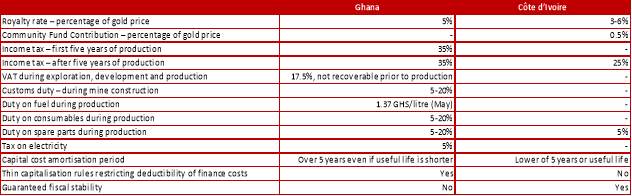

The table below illustrates the kind of policies that attract and promote foreign investment through a comparison between some key policies in the countries of Ghana and Côte d’Ivoire. This table illustrates how a few differences in key policies can result in major differences in a country being favoured as a destination in which to invest. The Ivorian Government offers fiscal stability for all mining entities and it has a fiscal regime that is designed to attract and promote foreign investment, in comparison to Ghana which seems to have been heading in the opposite direction in the last couple of years.

Source: (MMNR 2012, KPMG 2014, GRA 2015, MMNR 2015)

- As highlighted in the table above, in Côte d’Ivoire mining entities are provided with VAT and customs duty exemptions in all stages of the mining life cycle from exploration, construction and operations phases, in comparison to Ghana where that early stage VAT is a non-recoverable cost and the operations stage VAT suffers from major delays in recoverability.

- Furthermore, Côte d’Ivoire has a sliding scale royalty regime compared to Ghana’s fixed rate royalty regime, as well as a five-year tax holiday from first production, thus promoting investment as the sliding scale royalty regime is far superior as highlighted above and the tax holiday provides a significant incentive for investment. The Ivorian tax rate then reverts to 25%, which is also more favourable when compared to Ghana’s 35% tax rate.

Côte d’Ivoire also does not have the tax legislation issues such as the imposition of taxes non-existent profits in Ghana that has been highlighted above in the tax analysis.

Thus, to continue to be the mining investment destination of choice, Ghana needs to review and amend its fiscal framework, as highlighted above, to continue to be competitive with its West African peers.

5 REferences

Banchirigah, S. M. (2008). “Challenges with eradicating illegal mining in Ghana: A perspective from the grassroots.” Resources Policy 33(1): 29-38.

CSSD, C. C. o. S. D.-. (2016). “Local Content: Ghana Mining.” from http://www.eisourcebook.org/cms/February%202016/Ghana,%20CCSI%20Local%20Content%20Mining%20Analysis.pdf.

Economist, T. (2012). “African governments are seeking higher rents and bigger ownership stakes from foreign miners.” from http://www.economist.com/node/21547285.

GCM, G. C. o. M. (2016). “Factoid on the indusry’s performance.” Retrieved 15/10/17, from https://ghanachamberofmines.org/wp-content/uploads/2016/11/Factoid-2016.pdf.

GMOF, G. M. o. F.-. (2016). Public Financial Management Act 2016.

GRA, G. R. A.-. (2015). The Income Tax Act 2015 (Act 896)

GRAEME HOSKEN, S. J., JAN BORNMAN, and KYLE COWAN (2017). “The truth about South Africa’s illegal mining industry.” Retrieved 27/10/17, from https://www.businesslive.co.za/rdm/business/2017-03-27-the-truth-about-south-africas-illegal-mining-industry/.

ICMM&GCM, I. C. o. M. M. a. G. C. o. M. (2015, July 2017). “Mining in Ghana – What future can we expect?” Mining: Partnerships for Development July 2015. Retrieved 28/9/17, from https://www.icmm.com/website/publications/pdfs/9151.pdf.

KPMG (2014). “Ghana: Country Mining Guide.” from https://assets.kpmg.com/content/dam/kpmg/pdf/2014/04/ghana-mining-guide.pdf.

MMNR, M. o. M. a. N. R.-. (2006). The Minerals and Mining Act 2006.

MMNR, M. o. M. a. N. R.-. (2010). The Minerals and Mining (Ammendment) Act 2010.

MMNR, M. o. M. a. N. R.-. (2012). The Minerals and Mining (General) Regulations 2012.

MMNR, M. o. M. a. N. R.-. (2015). The Minerals and Mining (Ammendment) Act 2015.

OBG, O. B. G. (2017). “Ghana government takes steps to address a recent decline in mining.” Ghana 2017. Retrieved 28/9/17, from https://www.oxfordbusinessgroup.com/overview/digging-deep-government-taking-steps-address-recent-decline.

Otto. J et al. , A. C., Fred Cawood, Michael Doggett, Pietro Guj, Frank Stermole, John Stermole, and John Tilton (2006). Mining Royalties: A Global Study of Their Impact on Investors, Government, and Civil Society.

PWC (2017). “Two steps forward, one step back: The African tax landscape.”

UN (2017). “World Investment Report 2017.” from http://passthrough.fw-notify.net/download/119368/http://unctad.org/en/PublicationsLibrary/wir2017_en.pdf.

USGS (2014). “Exploration Annual Review 2014.” from https://minerals.usgs.gov/minerals/mflow/exploration-2014.pdf.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "International Studies"

International Studies relates to the studying of economics, politics, culture, and other aspects of life on an international scale. International Studies allows you to develop an understanding of international relations and gives you an insight into global issues.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: