Triple Bottom Line: Environmental Sustainability in Construction

Info: 8917 words (36 pages) Dissertation

Published: 6th Sep 2021

Abstract

The sustainability related ides of TBL (Triple Bottom Line) was coined by Elkington (1997), according to which true sustainability relies on economic prosperity, social uplift environmental sustainability as a whole. Big organizations are the drivers of development, hence it is their responsibility to look at all these three aspects and move towards sustainability. Since construction all over the world takes a major chunk of economy and resources and 90% of population comes in contact with the built environment, it is imperative that this sector is taken care of in terms of sustainability, and TBL seems to be the way forward. TBL reporting based on GRI gives a quantitative look to the sustainability goals which help the organization to set their target and more towards sustainability. However, there are still challenges faced by the organization when it comes to reporting social indicators as there are various intangible factors are involved which are hard to calculate. If there’s more focus give to the quality of data rather that how we calculate the data then TBL will help us ensure true sustainability.

Table of Contents

Relationship of TBL with Sustainable Development (SD)

Key Themes of Sustainable Development

Key Questions in Sustainable Development

Significance of TBL in Sustainable Development

Significance of TBL in Sustainable Construction

TBL Reporting Exercise based on Global Reporting Initiatives

Challenges and Issues in Reporting Sustainability

List of Tables and Figures

Table 1 The Seven Transitional areas (inspired by Elkington, 2004, 3)

Table 2 Summary of Key Areas, Goals, Risks

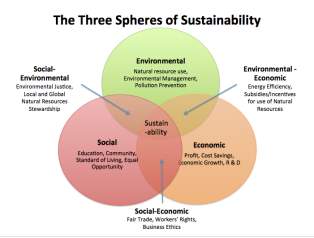

Figure 1 The Three Spheres of Sustainability

Figure 2 illustrations of TBL, Inspired by Elkington, 1994

Figure 3 Corporate Responsibility Landscape (McElhaney, 2008, 230)

Figure 4 Sustainable Development and TBL (Both Address the Same Aspect)

Introduction

Triple Bottom Line

Triple Bottom Line (TBL), is a sustainability related idea introduced by Elkington (1997). This concept come to the forefront when the term “sustainable development” was coined in the Brundtland Report (1987). The Brundtland Report stated sustainable development as “development that meets the needs of the present generations without compromising the ability of the future generations to meet their own needs”[1]. TBL focuses on the notion of environmental sustainability and integrates the social and environmental aspects.

Figure 1 The Three Spheres of Sustainability

The Concept of Triple Bottom Lines – Review

When the developed countries started focusing on the issue of sustainability, in 1997, Stuart Hart noted that ‘Beyond greening lies an enormous challenge – and an enormous opportunity. The challenge is to develop a sustainable global economy: an economy that the planet is capable of supporting indefinitely’ (Hart, 1997). It was then explained by Hart that getting rid of pollution isn’t just the solution to the problem of sustainability and the world would have to look at it from a larger context. Even if zero emission are achieved by 2000, the world would still be stressed in terms of generating resources and in coming times the ability to meet the needs future generations will be destroyed.

The issue at hand is not only bound to economic and environmental realms, it stretches out and connects with ethical, social and political aspects as well. All these aspects will have to be seen from the same prism in order to reach the goal of sustainability. Hence, economic and social bottom lines were added to economic bottom line to get a measure of sustainability.

The Bottom Lines

The economic bottom line: It is the measure of a company’s profits after all the deductions are done. Generally, an organization is said to be improving its economic bottom line when it is increasing its net earnings and reducing costs. Some of the examples include:

- Personal income

- Establishment churn

- Job growth

- Cost of underemployment

- Employment distribution

The environmental bottom line: It is the measure of natural resources and how would they be sustainably utilized. The concept of natural wealth, thus, becomes important to understand. E.g., one cannot simply make an account of trees cut in a forest and weigh it against a price, but various other functions of trees in a forest would have to be considered also as they contribute in the regulation of water, greenhouse gasses and they also play an important part in maintaining the flora and fauna of the forest. There are 2 forms of natural capital, the first one is called ‘critical natural capital’- which is necessary to sustenance of life and the other is called ‘renewable capital’- which can be replenished or repaired. A company is said to be improving its environmental bottom line when it is has a stable resource base, it is managing its resources and it is continually conserving and maintaining biodiversity and eco system.

The social bottom line: It is the measure of how much an organization is taking care of its employees. For many years, it was believed that sustainability had no link with social, ethical or cultural issues. But, recent studies have shown that, it is the most important factor behind sustainable development. E.g., if in organization the employees trust one another as they all work according to ethical norms, they will be able to work more efficiently as they will create a wide variety of social relationships. A company is said to be improving in its social bottom line when it is treating its employees with equity in terms of health and education, it is promoting gender equality, there’s political accountability and participation of the workers.[2]

There is no unified definition of Triple Bottom Line (TBL) but, generally it can be described as the communication between the corporate entity with its stakeholders that defines the company’s method to manage its environmental, social and economic aspects of its workings. [3]

TBL is a reporting framework which incorporates environmental, social and economic aspects while accounting an organizations performance. These three aspects are also referred to as people, planet and profits where the “people” bottom line is referred to as the measure of how an organization has treated its employees with due care, the “planet” bottom line is referred to as how environmentally responsible the firm has been in its operations and the “profit” bottom line is referred to as how much a the profit and loss accountability. [4]

According to Andrew Savitz TBL “Captures the essence of sustainability by measuring the impact of an organization’s activities on the world … including both its profitability and shareholder values and its social, human and environmental capital”. In short, all these aspects should be viewed in totality in order to ascertain their impacts in a larger context.

There’s no concrete agreement as to how many aspect should be looked into in terms of defining sustainability, some other aspects include community improvement, environment, entrepreneurship and education (Sher & Sher, 1994). But, there’s a consensus that all these aspects are measured in terms of their influences on the society currently and in the days to come.

TBL has made organizational reporting more transparent as the companies have to report on both positive and negative aspects simultaneously in terms of how the company is effecting sustainability. This type of thorough reporting creates better communication with all the stakeholders. There are frequent re-evaluation so that the targets set are met. Moreover, showing TBL reports creates trust between the company and the stakeholders and improves global influence (Ho & Taylor, 2007). [5]

Figure 2 illustrations of TBL, Inspired by Elkington, 1994

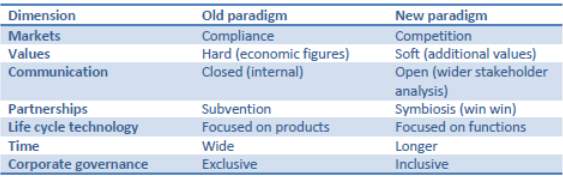

The above illustrations show different meanings of triple bottom line but there is a commonality in all these images as all of these illustrations focus on the ‘shared part’. The hard lines between these aspects become blurred and greater emphasis is given to how these aspects interact with each other. TBL can also be referred as a transitional practice where organizations are moving forward from their old methods to new methods and different aspects represent different corporate ambitions. The table below shows the paradigm shifts.

Table 1 The Seven Transitional areas (inspired by Elkington, 2004, 3)

The Seven Drivers of Elkington

According to Elkington (2004), TBL would start a ‘cultural revolution’ and this revolution will be led by different businesses. Also, external factors such as rapid globalization, deregulation and societal pressures would force these businesses to be open and flexible. These changing aspects are defined below.

Markets: As the competition increases, there is always a growing need to introduce something new which stands out in the market. This creates opportunities to experiment and create newer and better product.

Values: As TBL reporting has created more awareness of the problems regarding market conditions hence, values have changed. E.g., consumers tend to trust organizations which are involved with the community.

Communication: Increased transparency and rapid advancements have led to the need for the corporations to communicate more. E.g., the oil leak by BP was heavily criticized over their corporate misconduct.

Partnership: There is a focus on increased cooperation amongst all the stakeholders. Corporations have identified the fact that increased cooperation and access to external resources would lead to win-win situations more often than not.

Life Cycle Technology: Reconsidering products in terms of their value to the consumers has led to the thought of life cycle assessment which, in return, provides viable eco-friendly results. E.g., Xerox (An American Company) has start aiming at producing waste-free products with better life cycles.

Time: The notion of ‘Time is money’ is very well realized by the organizations and they are quick in reacting to changes. There are systems put in place for reporting at different intervals e.g. “just in time” and “LEAN” production systems.

Corporate Governance: The CEO’s and board members have a shared responsibility to tackle strategic issues; they have to act within the boundaries of Triple Bottom Line. [6]

Corporate Responsibility

Modern day business have to take into account a broad spectrum of objectives which are beyond the scope of just making profits. [7] These objectives include:

- Consumer oriented goods and services

- Job creation for stakeholders

- Continuous product innovation

- Investment in upgrading technologies and employee skills

- Continually working on international standards for environmental practices

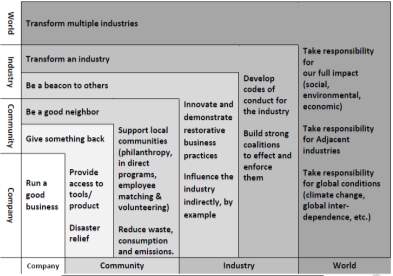

These objectives create a boundary of accountability for which these businesses will be held accountable. Thus, organizations will have to act reasonably and with due diligence. Corporate responsibility (CR) means that these organizations will have to involve all the stakeholders and create parity in the interest of the stake holders. These interests may sometimes overlap, hence it becomes a very delicate management job. Some of these interests are given in the figure 3.

Figure 3 Corporate Responsibility Landscape (McElhaney, 2008, 230)

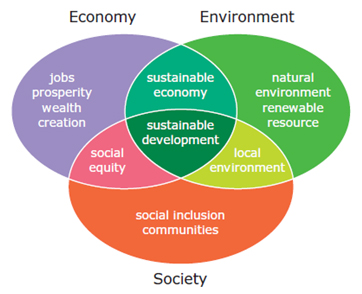

Relationship of TBL with Sustainable Development (SD)

When describing the relationship between Triple Bottom Line (TBL) and Sustainable Development, it is imperative to understand the meaning of sustainable development first. According to Brundtland Report (WCED, 1987), it is defined as “Development that meets the needs of the present without compromising the ability of future generations to meet their own needs”. Sustainable development connects the carrying capacity of the world with economic, social and environmental realities. “Thus the goals of economic and social development must be defined in terms of sustainability in all countries developed or developing, market-oriented or centrally planned” (World Commission on Environment and Development, 1987). It was further elaborated by Elkington that businesses should not only focus the bottom line of profit, but they will have to include two more bottom lines of environmental stewardship and social progress to achieve true sustainability.

According to Australian Commonwealth, State and Territory Governments Sustainable Development is defined as ‘Development that improves the total quality of life, both now and in the future, in a way that maintains the ecological processes on which life depends.‘

Australian Building Codes Board define it as ‘Development that effectively balances long and short term economic, environmental and social considerations to meet the needs of the present without compromising the ability of future generations to meet their own needs.’

Figure 4 Sustainable Development and TBL (Both Address the Same Aspect)

Triple Bottom Line recognizes the three aspects will have equal impacts in terms of allowing the generations to meet there need and protecting the needs of future generations. Hence, a conspicuous relationship between the two can be identified. According to Payne and Raiborn, 2001 without SD “neither business nor the societies in which they exist will have a long term future”. There have been various definitions of sustainable development proposed like those by Fergus and Rowney, 2005, MacDonald, 2005 and Baumgartner, 2004 etc., but none has gone outside the scope of Triple Bottom Line. Hence, it can be clearly said that there is a strong relationship between the two as sustainable development is a model of triple bottom line.

Key Themes of Sustainable Development

According to Wang (2015), there are various key themes that sustainable development addresses, these key themes are discussed below as sustainable development:

- Concerns that the earth resources are limited and that there is a need for better resource efficiency. Rapid growth in population has put a great amount of stress on earth’s resources. These resources are limited in number so these resources will have to be utilized in an efficient manner so that we don’t harm the capacity of future generation to meet their need.

- Concerns that developments may reduce the biodiversity and upset the ecology on which all life depends. Development at any scale should take into consideration the ecological factors and shouldn’t disturb the earth’s natural cycles, otherwise lives of all the species will be at a great risk.

- Concerns for future generation. As discussed before, sustainable development is primarily focused on safeguarding the needs of generations to come.

- The need to improve quality of life for all. Sustainable development also emphasizes on better living conditions for all the people living on earth.

- The need for equity between different groups of people on earth. With the development of the world, various groups in society should have equal rights, justice and there’s no partiality amongst different groups.

- The need to balance between competing goals (economic, environmental, social). Sustainable development shouldn’t be only looking at environmental sustainability, that only a part of SD; for long lasting sustainability, economic and social factors should also be taken in account. There should be parity amongst the three factors while moving forward.

- The realization of the interdependency within and between all communities on earth. No community or group can thrive in isolation, especially in the era of globalization. Everybody will have to realize that interdependencies will have to be created and respect in order to attain efficient and sustainable development.

- Intergenerational equity on the aspect of natural capital that has to be shared equally between now and future. It means that the future generation would have the same amount of natural resources available to them as the current generations have.

- The humility principle: it recognizes the limitation of human knowledge and puts burden of proof on those taking the action.

- The precautionary principle: it advocates caution when in doubt.

- The reversibility principle: it requires not to make any irreversible change.

Key Questions in Sustainable Development

According to Wang (2015), there are a few key questions which sustainable development will need to answer. These questions are discussed below:

- Can the current world development continue? (Do we have enough resources, food, energy, forests, water etc. to go on for the foreseeable future? What are the effects of the reduction in forest areas?

Sustainable development, at its core, derives its concept from balancing the use of resources and managing them well. Growing population and resource mismanagement are hindrances to global development but sustainable development answers these issues by balancing resource usage so that development continues.

Proper management of resources by using principles of sustainability would mean that we will have enough resources to go on in the foreseeable future.

Reduction in forest areas has contributed a lot in global warming and climate change, but reducing deforestation and relying on reusable materials more will lessen the impacts and move us towards sustainable development.

- What will the pollution do to us? (Air pollution, Acid rain, indoor air pollution, water pollution, waste etc.?

Air pollution, Acid rain, indoor air pollution, water pollution, waste etc., are going to have severe impacts on all the species in the world. We have been witnessing extinction of many species and this trend could reach out to human beings as well. Sustainable development offers a way out by minimizing the pollutants and keeping the environment clean.

- What problems are we creating for future generations? (Chemical problems, biodiversity, global warming)

We have spread very harmful greenhouse gasses into the atmosphere, polluted our environment and adversely impacted the natural cycles. Global warming and climate change are amongst the various issues that we have created for the future generations. Looking forward, we will have to focus on sustainable development so that our future generations don’t get burdened to meet their needs.

Significance of TBL in Sustainable Development

Industries and businesses are the main drivers of sustainable development, hence it is important that the principles of TBL are incorporated in the working procedures of these businesses.

According to Doyle, (1991, p4) ‘I think each of us here can see that however sustainable development is ultimately defined, industry will have the primary role in making it work. We are the experts at development. We do the production for society. It is critical that we assume leadership in this area.’ The importance of industries in sustainable development is emphasized here and it is also believed that that industries will take the leadership role in development. Looking at this scenario the significance of TBL is further strengthened because TBL will define the workings of the businesses and these businesses will further define sustainable development in the world.

Some of the generic characteristics of TBL as defined by Adams (et al., 2004) are defined below.

Accountability – It means that organizations and business will have to be accountable to all the stakeholder in terms of the targets set for economic, social and environmental sustainability. There has been a growing significance of stakeholders and focus on accountability.

Transparency – It means that every organization need to be transparent in the way they conduct their businesses. All the data regarding the three aspects of TBL should be made available to all the stakeholders. This not only solidifies accountability, but also it creates a sense of trust between the organization and the stakeholders. If there are any uncertainties or assumptions in the data, these should also be conveyed to the concerned people.

Measurability – Elkington (1998, p.72) says that the key to managing organization progress towards sustainability is measurement. “What you can’t measure, you are likely to find hard to manage”.[8] Hence, TBL emphasizes on the concept of measurability where social, environmental and economic sustainability factors are measured.

Benchmarking – There are certain standards set by the organizations, these standards are then considered to be the benchmarks which have to be achieved and the performance of the three aspects is weighed against these benchmarks.

Integrated Planning and Management – TBL goals have to be echoed in the planning and management tiers as well. Hence, these goals are defined at the policy level and people are educated to achieve those goals. There’s a strong commitment in understanding stakeholder views and various strategies are formulated to keep everyone a part of the TBL process.

Clarity – Organizations emphasize on the clarity of communication and information availability in order to achieve efficient results.

Significance of TBL in Sustainable Construction

Sustainable Construction Definitions

“The creation and responsible management of a healthy built environment based on resource efficient and ecological principles” (Kibert, 1994, cited in Wang 2015).

“A way of building which aims at reducing negative health and environmental impacts caused by the HES6176 – Environmental Sustainability in Construction © 2011 health and environmental impacts caused by the construction process or by buildings or by the built-up environment” (The Netherlands: CIB, 1999, cited in Wang 2015).

“In its own processes and products during their service life, aims at minimizing the use of energy and emissions that are harmful for environment and health, and produces relevant information to customers for their decision making” (Finland: CIB, 1999, cited in Wang 2015)

“Sustainable construction means that the principles of s stainable development are applied to the of sustainable development are applied to the comprehensive construction cycle from the extraction and beneficiation of raw materials, through the planning, design and construction of buildings and infrastructure, until their final deconstruction and management of the resultant waste. It is a holistic process aiming to restore and maintain harmony between the natural and built environments, while creating settlements that affirm human dignity and encourage economic equity’ (du Plessis, 2002, cited in Wang 2015).

Objectives of Sustainable Construction

Economic sustainability – efficient use and management of resources which include labor, energy, material and water, hence increasing profits.

Environmental sustainability – reducing emissions and waste wherever possible to protect the environment and efficient use of natural resources.

Social sustainability – taking care of the need of all the stakeholders from start to finish of a project. These people include workers, communities and the supply chain people.

Significance of TBL

In terms of environment, 40% of all materials and energy are used in construction, 40% of all greenhouse gasses are emitted due to construction and 40% of all the global waste is generated due to construction. In terms of society, 90% of all people’s lives are spent around buildings, quality of life and working conditions of people directly depends on the built environment. In terms of economy, construction takes a huge chunk of global economy and it’s a developing business worldwide.[9] (Source UNEP, 2007) Looking at these figures, it is important that all these aspects are handled in a sustainable manner, so the significance of TBL is realized.

As the global construction industry is growing, the demand for sustainable methods in construction is also growing and the designers and contractors are responding to this fact by incorporating sustainable methods in construction in order to compete in the market. TBL is being practiced by almost all the big construction companies in order to measure the environmental impacts that construction activities have.

TBL has expanded the practices of construction sector by employing social and economic indicators. Organizations have been able to make quantitative and qualitative assessment of their performances and it has yielded very good results in terms of sustainability as well. As there is a big chunk of natural resources spent on construction industry, there has been more focus on managing this sector according to the principles of TBL. Organizations have started to emphasize more on the environmental and social indicators and there has been stress on serving the customer and the stake holders.

As we have taken a lot from the natural resources of the world, it is imperative that we give something back to it as well, this is the sort of awareness that TBL has created in the organizations. In terms of financial results, the profits may be lesser when seen in isolation, but when we include the social and environmental aspects and gauge the sustainability results, they are very optimistic. So, it can be easily said that TBL has changed the landscape of construction industry in terms of its practice and the application of TBL in a sector which consumes a great proportion of natural resources will allow us to develop in a more sustainable manner.

Let us have a look at TBL approach to sustainable construction.

Environmental Aspect – TBL approach to construction is based on resource-efficiency and it includes better management of materials, energy, water and waste. Passive design methods are used so that building consume less energy, it is emphasized that reused materials are used, during construction period it is taken care that lesser water is consumed and wastage is minimized. There are various green rating methods used to see how environmental friendly a building is e.g., in Australia, a Green Star rating system is used and in the US, LEED rating system is used.

Social Aspect – Emphasis is given to the users of the buildings and factors like safety, access and security are considered. Sustainable building design also incorporates the needs of community and makes sure that the building interacts and contributes at a community level instead of working just in an isolated manner.

Economic Aspect – It is made sure that cost efficient construction methods are applied. There are strategies devised to make sure that construction time is minimized. Also, it is made sure that the materials used are cost efficient and durable. Local materials, workforce and suppliers are considered first in order to cut costs, this also helps in reducing time and logistic costs. Cost cutting is also considered at the design level, designers are urged to use cost efficient materials.

All in all, TBL provides a way forward in term of sustainable construction by considering not only the environmental dimension but also the economic and social dimensions.

TBL Reporting Exercise based on Global Reporting Initiatives

Introduction of the Organization

Company Name: ABC Construction

Establishment Date: 22-12-2007

Area of Expertise: Building Design, Construction, Project Management.

Main Location: Australia

Sub-locations: Pakistan, China, India.

My Role in the Company

I am Nayab Ahmed, I am the head of Sustainability in this company. We are an international company with head office in Australia and sublets in Pakistan, India and China. The most important goal of our company is to satisfy the clients while keeping sustainability in mind. In order to achieve this goal we are committed to use TBL reporting based on Global Reporting Initiative (GRI).

Strategies and Analysis

Section 1

Statement from the CEO of ABC Construction:

We at ABC construction believe that true development is the one which incorporates environmental protection, social development and economic growth. So, we have combined sustainability in our culture and our skills and we seek to achieve these targets by:

- Meeting the sustainability commitments of our clients and all the stakeholders.

- Our services will be based on the considerations of sustainability.

- Building on our knowledge and skill related to sustainability.

- Incorporating sustainability into our corporate values.

- Reducing carbon footprint.

We will take into account the interests of our stakeholder and try to achieve our goals according to the GRI G4 standards.

Our main goal is to tackle the challenge of sustainability across social, environmental and economic aspect.

Section 2

The most important opportunities that have risen from sustainability trends are that stakeholders have now realized that sustainability is the way to go in the future. Hence, our Company will try to meet those demands of our clients.

We have identified the key areas that we need to work on and they are reviewed on an annual basis by the Sustainability committee. We will continue to develop on our key area and tackle the risks accordingly.

Table 2 Summary of Key Areas, Goals, Risks

| Key Areas | Long-term Objective | Risks |

| Environmental Impact | Minimize the impact on climate. | Major environmental incident. |

| Quality Assurance | Aspire to provide better services in the times to come.

Ensure clients are satisfied. |

|

| Site Safety | Keeping our sites safe and legally compliant. | Major safety incident. |

| Occupational Health & Safety | Empower employees to have health and safety at the forefront of their thinking. | Major safety incident. |

| Our employees | Create an environment where employees can thrive | Employee recruitment, retention and motivation

Succession planning for senior positions |

| Corporate Knowledge | Safeguard our knowledge and expertise | Security of business information and assets |

| Community

Education & Involvement |

Support the communities in which we operate. |

Organizational Profile

Name of the organization: ABC Construction.

Primary services: Building Design, Construction, Project Management.

Countries in which the organization operates: Australia, Pakistan, China, India.

Nature of ownership: Private, owned in trust.

Markets served: Construction Markets in Australia, Pakistan, China, and India.

Scale of the organization:

- Total number of employees: 5,000.

- Total number of operations: 20.

- Net sales: 2 billion.

- Quantity of products or services provided: 3.

Total number of employees by employment contract and gender: 3000 males 2000 females.

Total number of permanent employees by employment type and gender:

- 1500 male fulltime permanent.

- 1500 female full time permanent.

- 2000 non- permanent.

Total workforce by employees and supervised workers:

Workforce: 10,000. 80,000 supervised.

Total workforce by region and gender: 10,000. Asian 8,000. Australian 2,000.

The percentage of total employees covered by collective bargaining agreements: 5%.

Externally developed economic, environmental and social charters: GRI G4.

ABC construction is a private company with over 5,000 employees. It is based in Australia but has branches in India, China and Pakistan.

Services provided by this company include building design, construction and project management with the key emphasis on sustainability across all the sectors.

Reporting Parameters

Profile

Reporting period: 12 months.

Date of previous report: 30/06/2015.

Reporting frequency: annual.

Scope and Boundary

This report contains the sustainability measures taken according to the environmental and social indicators. As the company focuses primarily on the stakeholder involvement, there would be priority set on how the company handles the stakeholders. Along with the stakeholder, the report will also focus on the financial sustainability along with community involvement as well.

This sustainability report shows the performance of fiscal year ending in 30th Jun 2015, and compares the baseline of the year 2014. Our baseline is recalculated this year as well and we will try to adhere to our baseline.

Governance Structure

Global Head of Sustainability

Chief Executive officer

Head of Sustainability

Head of Community Development

Major projects

ABC Construction

The Designers

Sapphire CR

Harrison Villa

Park House

Sites

Design

Material Sourcing

Occupational Health and Safety Manager

Sustainability Officer

Sustainability and CSR Manager

Sustainability and CSR Manager

Sustainability Officer

The governance structure will include local committees, the board of the company and stakeholder involvement. The board will take the decisions with the consultation from local committees and it will be ensured that all the stakeholders are involved in the process.

Commitments – ABC construction is committed to provide governance and responsible investment, it will also try to address the issue regarding climate change, bring new ideas and create value in their service. It will also create community integration, promote cultural diversity, take care of its employees and work on employment and training. Moreover it will reduce the carbon emission and try to manage the natural resources.

Stakeholder Engagement – ABC Construction will ensure that communities, civil society, customers, shareholders, suppliers and employees are engaged in all the projects.

Local Government

ABC CO

Stakeholder Engagement

Customers

Residents

Employee Groups

Employees and Contractors

Suppliers and Vendors

Investors and Financers

Multi Lateral Organizations (e.Unesco

Local Community

Federal Government

Management Response

ABC construction is committed to give management response to specific problems. These responses are discussed below.

Sustainable Design and Operation – Integrate sustainability in all the design and achieve green star rating.

Incident & Injury Free – Ensure an injury free environment through management.

Valuing Our Employees – Ensure personal and professional development of all the employees.

Climate Change and Energy Management – Achieve net zero carbon emissions.

Water Management – Achieve net zero water usage.

Waste Minimization: Achieve net zero wastage.

Enhancing Biodiversity and Land Use – Achieve a net increase in the ecological value.

Responsible Sourcing – Ensure that the supplies and contractors follow the same sustainable principles of the company.

Community Development – Ensure that all the projects help in the community development as well.

Challenges and Issues in Reporting Sustainability

There is a lot of complexity involved in measuring sustainability. Measurement of intangible assets such as loyalty are very difficult. In order to expand the reporting system, companies continuously develop and state their methods. But, the objectivity still remains unclear. There is more emphasis on obtaining measurement rather than how much the measurement are reliable.

Social measurement – The G3 guidelines for GRI (Global Reporting Initiative) provides insufficient guidance as to why indicators were considered core or not. A ‘relevance’ or ‘materiality’ section could be added to indicate an indicator to be more important than others. There are a lot of indicators which make it hard for the organizations to give priority to indicators. With so many indicators to choose from, corporations tend to pick only those indicators which are important to them. (Moneva et al. 2006)

Social performance – Social and environmental performance is unique to each corporation, or at least industry, and is difficult to quantify (Hubbard 2009). There is a huge criticism on Elkington’s measurement claim and aggregation claim. According to the measurement claim, social performance can be quantified with objective methods. It is very difficult to measure the level of goodness or bad in a problem also, it is important to assess social impacts in both quantitative and qualitative ways. Especially, the social impacts need to be assessed in qualitative way.

Based on past research, the amount of reporting done on social aspects of corporate responsibility is significantly lower than reporting done on environmental issues (Adams 2002; Kolk 2003). That is because social impacts are hard to measure.

Problem in Aggregation – Sustainability reporting is very had to aggregate across the social, environmental and economic impacts. The basic problem with that is the quantification of a social number; different firms can calculate a different number using different formulae which suits them. There is no prioritization formula for different stakeholder groups. Also, there is no formula which can aggregate the three principles.

Reductionism – This is an approach to measurement where scientist break down the complex systems and study it in isolation and then their interconnections. This approach has received much criticism as said by Slobodkin, 1994.

There are many complex factors behind every measurement, by simplifying them, we are putting ourselves at risk.

Moreover, there has been various critical voices regarding the measurement of very sensitive factors. Some say that ‘the GDP does not capture the depletion of natural resources or that evidently harmful activities or events are counted as assets (Hamilton, 1994; Cobb, Halstead and Rowe, 1995; Meadows, 1998)’.

Hence, it can be said that although measuring sustainability is a good thing as gives quantitative landscape of the problem at hand but, the qualitative side of measuring sustainability still remains a problem as there are a lot of sensitive interconnected factors which are not taken into account.

Conclusion and Discussion

All in all, the use of TBL in the working of the companies provides the way forward in achieving economic, ecological and social sustainability. Since construction all over the world takes a major chunk of economy and resources and 90% of population comes in contact with the built environment, it is imperative that this sector is taken care of in terms of sustainability, and TBL seems to be the way forward. Also, TBL has great linkages with sustainable development. TBL reporting based on GRI gives a quantitative look to the sustainability goals which help the organization to set their target and more towards sustainability. However, there are still challenges faced by the organization when it comes to reporting social indicators as there are various intangible factors are involved which are hard to calculate. If there’s more focus give to the quality of data rather that how we calculate the data then TBL will help us ensure true sustainability.

Bibliography

Mowat, D. (2002). The VanCity Difference — A Case for the Triple Bottom Line Approach to Business. Corporate Environmental Strategy.

Hayward, SF 2003, ‘The Triple Bottom Line’, Forbes, 171, 6, p. 42, Health Business Elite, EBSCOhost, viewed 6 September 2015.

Fauzi, H., Svensson, G. and Rahman, A. (2010). “Triple Bottom Line” as “Sustainable Corporate Performance”: A Proposition for the Future. Sustainability.

Thai, J. (2015). Triple Bottom Lines and Sustainable Development Overview Construction Essay. [online] UKEssays. Available at: http://www.ukessays.com/essays/construction/triple-bottom-lines-and-sustainable-development-overview-construction-essay.php [Accessed 8 Sep. 2015].

Ebner, Daniela, and Rupert J. Baumgartner. “The relationship between sustainable development and corporate social responsibility.” Corporate responsibility research conference. Vol. 4. No. 5.9. 2006.

Tripathi, Deepak Kumar, Arun Kaushal, and Vikash Sharma. “Reality of Triple Bottom Line.” Global Journal of Management and Business Studies 3.2 (2013).

Suggett, Dahle, and Ben Goodsir. Triple bottom line measurement and reporting in Australia: Making it tangible. Allen Consulting Group, 2002.

Thai, J. (2015). Triple Bottom Lines And Sustainable Development Overview Construction Essay. [online] UKEssays. Available at: http://www.ukessays.com/essays/construction/triple-bottom-lines-and-sustainable-development-overview-construction-essay.php [Accessed 9 Sep. 2015].

Sridhar, Kaushik, and Grant Jones. “The three fundamental criticisms of the Triple Bottom Line approach: An empirical study to link sustainability reports in companies based in the Asia-Pacific region and TBL shortcomings.” Asian Journal of Business Ethics 2.1 (2013).

Moldan, Bedřich, et al. “Composite indicators of environmental sustainability.” Statistics, Knowledge and Policy Key Indicators to Inform Decision Making: Key Indicators to Inform Decision Making (2005).

Jackson, Aimee, Katherine Boswell, and Dorothy Davis. “Sustainability and triple bottom line reporting–What is it all about.” International Journal of Business, Humanities and Technology 1.3 (2011).

Wang, R 2015, ‘Lecture3’, Environmental Sustainability in Construction, Learning Material on Blackboard, Swinburne University of Technology, 10 August, viewed 16 August 2010.

[1] Brundtland,1987,p 43.

[2] Elkington, J. (1998). Partnerships from cannibals with forks: The triple bottom line of 21st-century business. Environmental Quality Management, 8(1), pp.37-51.

[3] The Triple Bottom Line Explained. (2015). [pdf] Angela Lewis Consulting. Available at: http://www.angelalewis.com.au/publ/The%20Triple%20Bottom%20Line%20Explained.pdf [Accessed 5 Sep. 2015].

[4] Slaper, Timothy F., and Tanya J. Hall. “The triple bottom line: what is it and how does it work.” Indiana Business Review 86.1 (2011): 4-8.

[5] Jackson, Aimee, Katherine Boswell, and Dorothy Davis. “Sustainability and triple bottom line reporting–What is it all about.” International Journal of Business, Humanities and Technology 1.3 (2011): 55-59.

[6] Mark-Herbert, Cecilia, Julia Rotter, and Ashkan Pakseresht. “A triple bottom line to ensure Corporate Responsibility.” Timeless City land: An Interdisciplinary Approach to Building the Sustainable Human Habitat (1-7). Uppsala: Sveriges Lantbruks Universitet (2010).

[7] Svenskt Naringsliv,2004,6

[8] Tripathi, Deepak Kumar, Arun Kaushal, and Vikash Sharma. “Reality of Triple Bottom Line.” Global Journal of Management and Business Studies 3.2 (2013).

[9] Council, S. (2015). Construction | Sustainable Steel Council, Auckland. [online] Sustainablesteel.org.nz. Available at: http://www.sustainablesteel.org.nz/construction-and-the-triple-bottom-line/ [Accessed 9 Sep. 2015].

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "Sustainability"

Sustainability generally relates to humanity living in a way that is not damaging to the environment, ensuring harmony between civilisation and the Earth's biosphere.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: