Competition Environment of the UK Banking Industry

Info: 15957 words (64 pages) Dissertation

Published: 19th Jan 2022

Abstract

Competition of the bank industry can affect the efficiency as well as the financial stability. In order to investigate the competition environment of UK banking industry, two competition measures in non-structural approach, Panzar-Roose H-statistic and Boone indicator, have been used in this study. Using panel data captured from the banks’ balance sheets with the bank-specific variables, this paper will inspect the trend in competition environment of UK banking market during the period of 2007-2015. The results are quite fluctuated from two competition measures do not seem quite consistent in 2007-2009 but the pattern of change of competition is still quite similar to some recent studies after 2009.

JEL classification: D4, G21, L1.

Keywords: Banking industry; competition; Panzar-Roose Model; Boone indicator

Table of Contents

Click to expand Table of Contents

Abstract………………………………………………………ii

TABLE OF CONTENT…………………………………………….iii

List of Tables………………………………………………….vi

List of figures…………………………………………………..v

Chapter

- Introduction……………………………………….1

- LiteRature Review……………………………………2

- METHODOLOGY

3.1 Input and Output of a Bank…………………………………9

3.2 The Panzar-Rosse Model (PR Model)…………………………10

3.2.1 General Theory……………………………………10

3.2.2 Competition Environment Testing ………………………12

3.2.3 Equilibrium Testing ………………………………..14

3.3 The Bonne Indicator…………………………………….14

3.3.1 Intuition and Theory behind the Boone Indicator……………..14

3.3.2 Estimating Boone Indicator………………………….16

4. DATA………………………………………………….18

5.1 The Panzar-Rosse H-statistics ………………………20

5.2 The Boone Indicator…………………………………….23

5.3 Comparison between two Competition Measures…………………26

6. CONCLUSION………………………………………….28

REFERENCES …………………………………………30

Appendix

A. Equilibrium test for Panzar-Roose model………………………….35

B. Model used in the study and their assumptions ……………………..36

C. H-statistic and Bonne indicator across years and associated significance test……37

List of Tables

Table 2.1: Recent studies on measuring competition in banking industry

Table 3.1.1: Interpretation of

Table 4.1 Number of banks and observations by consolidation type and year

Table 4.2 Summary Statistics of variables

Table 5.1.1: H-statistic of whole period: fixed effects

Table 5.2.1: Boone indicator for whole period: fixed effects

Appendix A: Models used in the study and their assumptions

Appendix B: Equilibrium test for Panzar-Roose model

Appendix C: H-statistic and Bonne indicator across years and associated significance test

List of Figures

Figure 2.1: The Structure-conduct-performance paradigm

Figure 5.1.1: H-statistic over 2007-2005

1. Introduction

Before the 1990s, the UK banking industry was low in competition due to the tight banking regulations to restrict the lending activities in the domestic market (de-Ramon and Straughan, 2016).[3] The reformation of stock market from Banking Act in 1979 and Building Society Act in 1986 have increased the banking competition by encouraging the new entry of banks and changes the traditional role of banks and building society (Callen and Lomax, 1990). It also encourages the building societies to convert to banks by demutualisation in the 1990s. At the same time, mergers and acquisition were popular among banks but it did not alter the competition intensity significantly until 1999-2000. However, the competition started decreasing in the pre-financial crisis period in 2004 and onwards. Some banks and building societies were forced to be consolidated, nationalised and dissolved in the crisis which causing a continuous decline in competition of the UK banking industry. This has been supported by the previous empirical studies such as Weill (2013) and de-Ramon and Straughan (2016).

Along with the evidence and previous empirical studies, this study is aiming at investigating the competition environment in UK banking industry from the crisis period and the most recent available data in 2007-2015. Structural approaches such as concentration ratio (CR-ratio) or Herfindahl-Hirschman index (HHI) were the traditional models for competition measurements. However, these measures have been proved as the bad measure of competition which then new approaches have developed. In this paper, Panzar-Roose H-statistic and Boone indicators will be used to investigate the evolution of competition in recent years after the crisis with the panel data of 123 UK banks so that the results can be compared yearly and with some recent studies.

In the following paper, it consists of 6 sections. Section 2 reviews a broad range of literature of relevant empirical studies among the world and the development of competition measures. In Section 3, it includes the details of the theory and intuition of the competition measures used in this study. Section 3 shows an overview of the way to get the data and some basic findings from the summary statistics of the variables. The data will be used to for regression and the empirical results will be represented in Section 5. Eventually, Section 6 concludes the main findings from the study.

2. Literature Review

Previous studies on measuring competition are mainly from using two approaches: the structural approach and non-structural approach. In structural approach, it is common to measure the competition with the aim of market concentration by concentration ratio (CR-ratio) or Herfindahl-Hirschman index (HHI).[4] It states that the higher CR-ratio and HHI, the lower the competition in a particular market. This approach is based on the paradigm called “structure-conduct-performance” (SCP). In the other hand, non-structural approach uses the aim of econometrics methods such as Panzar-Roose (1982, 1987), Bresnahan (1982) and Lau (1982) models and the most recent model by Boone (2000, 2001, 2004. 20008) or Lerner (1934) index to develop competition measures which can be explained by the factors other than market concentration and market structure. These models have been classified as the New Empirical Industrial Organisation (NEIO) approach.

SCP paradigm, the structural approach, was the first model of competition measure as the major approach for early studies for competition. It was developed by Mason (1939, 1949) and Bain (1951, 1956, 1959). SCP tries to explain the firms’ conduct and performance with the structural features of the industries or markets. To begin with, the characteristics of a specific market or industry needed to be clarified include the numbers of firms and their size in terms of absolute and relative values, entry barriers and degree of product differentiations. With the above characteristics, SCP states that it is expected market structure will affect firms’ conduct such as prices, collusion, research and development, and advertisement costs. Conduct will, therefore determine the performances which can include profits, market shares, technology and efficiency. The solid arrows in Figure 2.1 indicate the relationship and linkage between structure, conduct and performance as the overview of SCP.

The traditional empirical studies suggest that increasing concentration ratio can reduce the cost of the collision which leads to anticompetitive behaviour and supernormal profits as the result of an increase in prices (e.g Bain (1951) and Weiss (1974)). They suggested that concentration and profit are positively correlated. Therefore, firms will act collusively to increase the profits.

Figure 2.1: The Structure-conduct-performance paradigm

Source: Goddard et al. (2001, pp.35)

Furthermore, it is also expected increase in competition will enhance the efficiency of a firm as the production cost will be reduced. This view was first raised by Hicks (1935) with “quiet life hypothesis”.[5] This view has been being supported with some evidence by some of the previous literature such as Barth et al. (2001), and Andrieşa and Căprarua (2014). However, the “efficient structure hypothesis” (ESH) by Demsetz (1974) proposed the opposite view which competition and efficiency are negatively correlated which is the assumption of SCP.[6] It has been being supported by some studies like Berger (1995), Goddard et al. (2001), Weill (2004), and Casu and Girardone (2006).[7] Therefore, the relationship between competition and banking system performance is more complex than expectations (Vives, 2001).

Berger (1995) found that ESH holds in U.S. banking which can explain more of the variation in bank profitability than SCP does. Both approaches together explain less than 20% variation in the bank profitability (Carbó et al., 2009). In, Stigler addition, studies on strategic actions of oligopolies and the role of the market of contestability raised the questions on the accuracy of SCP approach. From the early studies from Cournot and Betrand (1964) extended the theories on oligopoly that markets with high concentration can have aggressive competition which the firms may need to guess the prices and quantity of other competitors to react. This suggests that competition environment is necessarily determined by the market structure. On the other hand, Baumol et al. (1982) suggested that market contestability is significant to check the accuracy of SCP. Under a contestable market, firms’ behaviour is determined by the conditions of entry and exit.[8] The view is also in line with recent studies on banking industry such as Bikker et al. (2009).[9] Thus, the structure of the market is not related to competition which is also consistent with the view of the oligopolies’ behaviour. With the above limitations of SCP approach, alternative indicators for measuring competition need to be used.

NEIO, non-structural approach, was proposed to overcome the limitations of SCP approach. Non-structural approach attempt to measure rather than observe the competitive environment and it is not assumed that concentrated markets are not competitive at all (Gooddard et al., 2001, pp.81; Caus and Girardone, 2006). This approach also does not require clarifying a geographic market as the market power is given by the banks’ behaviour. In competition studies of banking industry, some literature uses Lerner index to analysis the competition with the degree of market power which is required to estimate a cost function of the firm. Alternatively, Iwata (1974) model uses the aim for conjectural variations within oligopolies and another model such as Bresnahan-Lau, PR and Boone models which use the concept of the contestable market.

The approaches of Bresnahan-Lau and PR are the most popular approaches among other empirical methods. Both of them based on the assumption that the market is in equilibrium which the firms will maximise their profits. PR model can work well even there are no information on equilibrium prices and quantities of a firm or industry, given the firms-specific data on revenue and factor prices (Matthews et al., 2007). Shaffer (2004) suggests that PR model works better in small samples while the Brensnhan-Lau model may cause an “anti-competition bias” with small samples. However, PR model needs to be handled carefully with the strong assumption. The long-run equilibrium test is required in order to make the H-statistic be a valid competition measures.[10] The H-statistic will only be valid if the market is in under a long-run equilibrium. This can address some of the problems from not having full information about cost market equilibrium (Bikker et al., 2012). As the H-statistics can be very sensitive to the way to scale the variables, Bikker et al. (2012) did an empirical study by using different scaling methods with data from 63 countries around the world from 2004-2010. In the case which H-statistics is not valid (no long-run equilibrium), Spierdijk and Shaffer (2015) suggests that Lerner index seems to be a good alternative approach to measure the market power.

In contrast to Boone indicator, it is still a very recent developed alternative approach. It has an advantage of small observations are enough for the analysis which is better than Bresnahan–Lau model as it requires more data (van Leuvensteijn et al., 2011). Boone indicator is not also just limited to investigate all types of banks likes what the Panzar-Roosse model typically applies with. Van Leuvensteijn et al. (2011) has developed an approach to analysis only the loan markets in 6 Europe countries, the US and Japan in 1994-2004. Schiersch and Schmidt-Ehmcke (2010) investigate the applicability of Lerner index and Boone indicator with the data from firms from every industry in Germany in the period of 1995-2996. They found out that the data does apply to Lerner index but seem not apply to the theory of Boone model. Van Leuvensteijn et al. (2011) also mention another limitation of Boone indicator that the indicator will misinterpret when there is an increase in heterogeneous products or firms seek to increase the market share rather than maximising their profits. Therefore, more empirical studies need to be done to check the applicability of Boone indicator.

Table 2.1 shows the summary of some recent studies on estimating competition environment in banking. These studies make use of various competition measures industry including both structural and non-structural approaches that discussed above. They cover the data over the UK, other EU countries and rest of the world across year from 1989-2013 and report the findings by years, sub-period or average of the whole period. All of the studies find that UK banking market is indeed under a monopolistic competition.

The most recent study from de-Ramon and Straughan (2016) covers four competition measures on analysing the depositing-taking institutions in the UK from 1989-2013. They find that the competition is less intense across the period which the difference is quite large by comparing the year of 1989 and 2013. The competition decreases sharply around the financial crisis in 2007-2008. They also find that measure of Boone indicator is more volatile than the other measures that they use. This is also consistent with the finding in other studies (van Leuvensteijn et al., 2007; Schaeck & Cihák, 2010; Schaeck & Cihák, 2014).

In contrast, Matthew et al. (2007) conduct the study on UK banking industry for the year of 1980-2004 which part of the years is covered in studies de-Ramon and Straughan (2016). Even they use different sub-periods as de-Ramon and Straughan (2014), they also find the same results that the UK banking competition has dropped when compare the 90s to early-2000s than 80s and the first sub-periods and last sub-periods.[11] Matthew et al. (2007) suggest the decline in competition can be explained by the merger and acquisitions of banks, the conversion of a series of building society and changes in banking regulations. Matthew et al. (2007) also conducted the equilibrium test and found out sub-periods in 1983-1992, 1986-1995 and 1995-2005 were not in equilibrium. This is inconsistent the results from de-Ramon and Straughan (2016) as he found out there was market equilibrium in almost all year (except 1997-1999 and 2009-2011).

Most of the studies using PR model found a close range of H-statistics 0.5-0.8 (Goddard & Wilso, 2008; Carbó et al., 2009; Claessens and Laeven, 2004; Bikker et al., 2012, Schaeck and Cihák, 2012, Andrieşa & Căprarua, 2014). [12] This means the competition of UK banking industry is quite high. Casu and Girardone (2006) study the banking industry across EU-15 countries in 1997-2003 including the UK which found out those banking markets in EU-15 and UK were in monopolistic competition. However, they found out a low value of H-statistics around 0.3 for UK banking industry for the period even having a large number of banks than other EU countries which indicates a low competition. They also construct DEA efficiency score and integrate into the Panzar-Roose model and found out that H-statistics fell for all countries whether the efficiency score is included.[13] The small value of H-statistics was also supported by the Schaeck and Cihák (2012) and Weill (2013). For instance, Schaeck and Cihák (2012) found out a small H-statistics among the commercial banks and small-sized banks. They also argue that large banks mainly engage in “arm’s length lending” with a lower level of capital than small banks while small banks primarily focus on lending services to the banks need high monitoring due to the asymmetric information. Despite the difference the values of H-statistics, all studies which analysis yearly and in sub-periods found out a decrease in competition across the year from the 1980s to 2010s.

Table 2.1: Recent studies on measuring competition in banking industry

| Authors | Region | Period | Measures1 | Series2 | Findings3 |

| Andrieşa & Căprarua (2014) | EU-27 | 2004-2010 | PR | X | Monopolistic Competition; high H-statistics (0.7) |

| Bikker et al. (2012) | 63 countries | 1994-2004 | PR | X | Monopolistic Competition; high H-statistics (0.5-0.7) |

| Carbó et al. (2009) | 14 EU countries | 1995-2001 | PR | X | Monopolistic Competition; high H-statistics (0.7) |

| Casu & Girardone (2006) | EU-15 | 1997-2003 | CR, PR | X | Monopolistic Competition; low H-statistics (0.3) |

| Claessens & Laeven (2004) | World | 1994-2001 | PR | X | Monopolistic Competition; high H-statistics (0.7) |

| de-Ramon & Straughan (2016)4 | UK | 1989-2013 | HHI, L, PR, B | A, C | PR: Monopolistic Competition; decreased over the period; big range of H-statistic (0.07-0.8)

B: Decreased over the period; most volatile measures |

| Goddard & Wilson (2008) | G7 | 2001-2007 | PR | X | Monopolistic Competition; Broad range of H-statistics (0.3-0.8) |

| Matthews et al. (2007) | UK | 1980-2004 | PR | C, X | Monopolistic Competition; high H-statistic (0.4-0.6) |

| Schaeck & Cihák (2010) | 10 EU countries & US | 1995-2005 | B | A | A range of 0.05-0.1 (absolute term); Competition decreased over the period |

| Schaeck & Cihák (2012) | 10 EU countries | 1999-2005 | PR | X | Monopolistic Competition; low H-statistics in commercial banks (Large: 0.1, Small:0.3); high H-statistics full sample (Small:0.5, Large: 0.7) |

| Schaeck & Cihák (2014) | 10 EU countries | 1995-2005 | B | A, X | A range of 0.05-0.1 (absolute term);Competition decreased over the period |

| van Leuvensteijn et al. (2007) | 6 EU countries, US & Japan | 1994-2004 | B | A | A range of -1.9-0.4; Competition increased over the period with a decrease in competition from 1999 |

| Weill (2004) | 12 EU countries | 1994-1999 | PR | A,X | Monopolistic Competition; Competition decreased over the period; high H-statistics (0.4-0.7) |

| Weill (2013) | EU-27 | 2002-2010 | L, PR | A, X | Monopolistic Competition; Competition decreased over the period; low H-statistics (0.1-0.2) |

Notes:

1 HHI: Herfindahl-Hirschman Index; L: Lerner Index; PR: Panzar-Roose H-Statistic; B: Boone Indicator

2 A: Annual; C: Average for sub-periods; X: Average for period

3 Shows findings for UK banks only which use PR and B as the competition measures

4 This table is the extension version of the table in de-Ramon & Straughan (2016, Table 2.1)

That are not many empirical studies in the banking industry by using Boone indicator. The most recent study is from de-Ramon & Straughan (2016) found out a less negative in Boone indicator across the year which means a decrease in competition across the period and consistent with the result to the findings in H-statistics with a decrease in competition throughout the study period by suing sub-periods.[14] They also include a robust check with using a sub-sample the banks lend more than 50% of the balance sheet and found out the same result as van van Leuvensteijn et al. (2011) and without robust checking. The finding from Boone indicator from them is supported by others (Schaeck and Cihák, 2010, 2014; van Leuvensteijn et al., 2011). Schaeck and Cihák found that the UK banking competition decreased over 1995-2005 while van Leuvensteijn et al. found the same result in 1998-2004. They also concluded that UK banking industry has one the lowest competition inensity among the developed countries.

3. Methodology

3.1 Input and Output of a Bank

As banks provide wide ranges of products and services which mean there are no general definitions on the measuring the inputs and outputs, it is not applicable to measure the outputs as physical quantities like the case under manufacturing firms (Goddard et al., 2001, pp.102). This is the major problem when analysing a performance of a specific bank. However, the persistence development creates to main approaches to measuring the determinants of bank’s output and the production function: the production approach and the intermediation approach.

For instance, intermediation approach developed by Sealey and Lindley (1977) will be used in the following analysis. Under the intermediation approach, it considers the banks as intermediaries between investors and savers (Colwell and Davis, 1992; Goddard et al., 2001, pp.103). Banks take deposits and make loans with the assistance of the capital and labour. The banks use deposits along with other types of inputs like buildings, equipment or technology to transform the funds into loans and other securities (outputs) (Ferreira, 2011). Therefore, operating costs and interest costs will also be included in the total revenue function.

3.2 The Panzar-Rosse Model (PR Model)

3.1.1 General Theory

Roose and Panzar (1977) and, Panzar and Rosse (1982, 1987) developed a model based on the data of the impact on firm-level equilibrium revenues from the change on factor (input) prices. It can be used to analyse the differences in the types of banks (firms) such as the sizes and regions. PR model uses H-statistics to estimate the market structure of a specific market from a reduced-form revenue function. It measures the

H-statistic as the sum of the elasticities of the total revenue with respect to each factor price which can be shown as:

H=∑k=1m∂Ri*∂wkiwkiRi* (1)

where

Ri*is the equilibrium revenues of the banks and

wki is a vector with factor

mand factor prices of bank

i.

It is based on a strong assumption that the banks are all in the long-run equilibrium[15] [16]which all the banks are maximising their own profits given by the available resources such that bank

iwill maximise profits when marginal costs equal to marginal revenues which the bank is making a normal (zero) profit:

Ri’xi, n, zi-Ci’xi , wi, ti=0 (2)

where

Riand

Cirefers to the revenues and costs respectively for bank

i;

xi,is the bank

i’s output;

nis the numbers of the banks; and

ziand

tiindicate the vector of exogenous variables which shifts the bank’s revenue function and cost function correspondingly.

Therefore, in general, H-statistic is derived from a reduced-form total revenue function:[17]

lnTRit=α+∑k=1kβk lnwkit+∑j=1jγjlnXjit+εit (3)

where

TRitis the total revenue of bank i at the time t; X is the exogenous variables that affect the bank’s revenue function and cost function; and

εis the disturbance term. While the choices of w and X can be different, TR can be represents in different forms which were use in previous studies. For examples, TR can be just equal total income (Shaffer, 1982; Claessens and Laeven, 2004).[18] It can also represent as the ratio of interest revenue to total assets (Molyneux et al., 1994). Some studies divided total income by total assets (Casu and Girardone, 2006). The coefficient

βkis the estiamted H-statistic which can be shown as:

H=∑k=1kβk (4)

H=1

represents a perfectly competitive market. As the increase in total revenue is proportionated to the increase in total cost and increase in price, factor costs will change by the same as total revenue.

H≤0indicates a market in monopoly competition. In order to maximise the profits, the monopolist will adjust the price and output. However, increase in factor costs will decrease the total revenue. Thus, H-statistics is in negative competition which the elasticities of the total revenue with respect to factor prices is inelastics.

0

H-Statistic under different condition. Moreover, the PR model also assume a monopoly firm faces a Cobb-Douglas demand function[19] with a constant elasticity

e>1,

H-statistics can be interpreted as the inverse measure of the degree of monopoly power, the Lerner index (

L)[20] (Bikker and Haff, 2002; Claessens and Laeven, 2004).

Table 3.1.1: Interpretation of

H-statistics

H ≤ 0 Indicates a collusive oligopoly or a monopoly, in which an increase in costs causes the output to fall and price to increase. Because the profit-maximizing firm must be operating on the price elastic portion of its demand function, total revenue will fall.

H = 1 Indicates a perfectly competitive industry, in which an increase in costs causes some firms to exit, price to increase and the revenue of the survivors to increase at the same rate as the increase in costs.

0

Sources: Goddard et al. (2001, p. 82); Casu and Girardone (2006, Table 2).

3.1.2 Competition Environment Testing

The reduced-form total revenue function is estimated to derive the H-statistics with different bank input and output. The following estimated function derived by Casu and Girardone (2006):

ln(TRit)=α+β1ln(P1,it)+β2ln(P2,it )+β3ln(P3,it)+γ1ln(EQASTit)+γ2ln(ASTit)+γ3ln(LOANASTit)+γ4ln(DEPit)+γ5ln(CASHDEPit)+γ6ln(OBSASTit)+uit (5)

for

i=1, 2, …, I, where I is the total number of the banks, and

t=1, 2, …, T, where T is the number of the periods which is the years in the following analysis. TR is the dependent variable that indicated the ratio of total revenue (income) over total assets and proxy of output prices. As non-interest incomes from fee-based products and off-balance sheet (OBS) activities have been increased greatly in past years, banks’ revenues are not only driven by interest income from tradition bank activities such as loan interest (Casu and Giardone, 2006). This view has been supported with different studies by Shaffer (1982), Nathan and Neave (1989), De Bandt and Davis (2000) and Lepetit et al. (2008). They stated that the divergence between interest and non-interest income becomes less important in an increasing competitive market. Moreover, as the sizes of the banks and accounting standard can be different across the countries, including the total assets in part of ratio of TR here can be avoid the standard of measures being poor by controlling for scale of the banks (Casu and Giardone, 2006; Biikker et al., 2012).

With the intermediation approach that addressed in Sealey and Lindley (1977), it is assumed that banks include labour, capital and deposits as the inputs.

P1is the ratio of personnel expense to total assets as the proxy of the average cost of labour.[21]

P2is the ratio of interest expense to total deposits, money market funding and short-term funding as the proxy of the average cost of deposits.[22]

P3is the ratio of other operating costs to fixed assets as the proxy of the average cost of physical capital.

A set of bank-specific exogenous control variables is there to reflect relevant activities of a bank[23]. It reflects the differences in structures, risk, costs, size and products across various banks. EQAST is the ratio of total equity to total assets. AST is the total asset. DEP is the ratio of total deposits to the total deposits, money market funding and short-term funding[24]. CASHDEP is the ratio of cash and due from banks to the total deposits. OBSAST is the ratio of OBS activities to total assets. Therefore, H-statistic can be measured as the sum of the input prices coefficients β1 to β3:

H=β1+β2+β3 (6)

Moreover, following the approach from Claessens and Laeven (2004) and Schaeck et al. (2009), time dummies are added to compare the H-statistic and competition trend, the regression can be shown as:

ln(TRit)=α+β1ln(P1,it)+β2ln(P2,it )+β3ln(P3,it)+γ1ln(EQASTit)+γ2ln(ASTit)+γ3ln(LOANASTit)+γ4ln(DEPit)+γ5ln(CASHDEPit)+γ6ln(OBSASTit)+δdit+uit (7)

where

dkt is the time dummies which takes a value 1 if

k=t when t is the year and 0 otherwise.

β in the interaction term will be the estimated H-statistic.

3.1.3 Equilibrium Testing

However, PR model assumes the market is in long-run equilibrium which may need a separate test to determine whether the assumption is satisfied. Therefore, a test is needed for testing whether the market is in long-run equilibrium. The test can be done by replacing the dependent variable in equation (6) with the natural logarithm of return of assets (ROA):

ln(ROAit)=α+β1ln(P1,it)+β2ln(P2,it )+β3ln(P3,it)+γ1ln(EQASTit)+γ2ln(ASTit)+γ3ln(LOANASTit)+γ4ln(DEPit)+γ5ln(CASHDEPit)+γ6ln(OBSASTit)+uit (8)

where ROA is the ratio of profits to total assets. By using the F-test, we can test if the F-statistic on

F =β1+β2+β3 in which

F=0 if the market is in equilibrium or

Fet al. (1994), Clasessens and Laeven (2004), Casu and Girardone (2006), Matousek et al. (2015) and de-Ramon and Straughan (2016).

3.2 Boone Indicator

3.2.1 Intuitions and Theory behind Boone Indicator

Bonne indicator is a recent developed and alternative measure of competition based on the idea of efficient structure hypothesis which was introduced and developed by Boone (2000, 2001, 2004), Boone et al. (2004), CPB (2000). The method was first applied to studying banking industry in van Leuvensteijn et al. (2007) to analysis the competition within the loan markets of the euro area. Boone indicator assumes that firms with greater efficiency (firms with lower marginal costs) can expand the output with smaller costs compare to less efficient firms. Hence, they can enjoy greater profits and market shares. The stronger the effect is, the higher the competition intensity is in a specific market. An “output-reallocation effect” will then exist which the output is reallocated to firms with more efficiency due to the decrease in profits in lower efficient firms causing them leave the market.

With the interpretation, Boone et al. (2004) and van Leuvensteijn et al. (2007), a firm (bank) ishould face the following demand curve with a product (or a portfolio of products)

qi:

pqi, qj≠i=a-bqi-d∑j≠1qj (9)

where each bank will face constant marginal costs,

mci. The parameter p represents the price, a is the market size, b indicates the elasticity of demand, and d capture how close the consumers think the various products in a market as the substitutes within each product. Assume that

a>mci and o

πi=(pi-mci)qi. So that the first-order condition for Cournot Nash equilibrium can be shown as:

a-2bqi-d∑j≠1qj-mci=0 (10)

In a market with Nbanks which produce positive levels of output (qi>0), the optimal output level as a function of mci can be obtained by solving Equation (9) to obtain:

qimci=2b/d-1-2b/d+N-1mci+∑jmci/2b+dN-12b/d-1 (11)

From

πi=(pi-mci)qi, it can be seen that there is a quadratic relationship between variables profits and marginal costs with negative a slope. With the variables profits

(πi) excluding costs of entry (ϵ), equation (10) indicates the relationship between output and marginal costs which a bank will enter the market if, and only if,

πi≥ϵ in equilibrium.

According to the above features, it can be concluded two reasons for increasing competition: (i) close substitutes exist for banks products and services, i.e. d increases when d

ϵ reduce. Boone (2004) and Boone et al. (2004) has proved the performance and market shares of higher efficient firms improve and increase under above two regimes.

3.2.2 Estimating the Boone Indicator

From the theoretical model from Boone (2004,2008), Boone et al. (2004, 2005) characterise the relationship between profits and marginal costs for bank i:

πit=α+βlnmcit+εit (12)

where

πit is the variables profits,

α is the intercept,

mcit is the marginal costs, and

ε it is the random error for each firm i at period t. CPB(2000), Boone et al. (2004) and Boone et al. (2005) suggested that average cost cit should be the proxy for mcit because marginal costs cannot be observed directly[25]. The parameter β is the estimated Boone indicator.

It is also necessary to include bank-specific control variables and to the above model for a complete analysis. By using the intermediation approach mention in section 3.1, it is assumed to use the same inputs and bank control variables in the Section 3.1.2.[26] Following the model from Boone et al. (2007), it is suggested that the Boone indicator can be estimated with the following model:

πit=α+βlncit+δXit+εit (13)

where

πit is defined as the ratio of profits to total assets[27].

cit is the average costs consist of the average cost of three inputs has been specified[28] which equal to the ratio of inputs costs to the total revenue.

Xit is the bank control variables which has been stated previously and

εit is the error term for bank i at period t. The determination of all the variables has been specified in the Section 3.2 which the above model will share the same bank-control variables as in PR model. Therefore, β is the estimated Boone indicator.

In order to see the trend and revolution of competition environment, time dummies are added to the regression to get the Boone indicator for each year (Scheack and Cihák , 2014; de-Ramon and Straughan, 2016) so that the regression can be expressed as:

πit=α+βdktlncit+δXit+γdkt+εit (14)

where

dkt is the time dummies which takes a value 1 if

k=t when t is the year and 0 otherwise.

β in the interaction term will be the estimated Boone indicator.

β will take the value between -∞to 0 as profit are higher for banks with lower marginal costs (Scheack and Cihák, 2014). In practice, the Boone indicator is in negative which also indicated that higher the absolute value of β is, the greater the competition is.

-∞ is the case when the market in perfect competition as an increase in costs forces firms with lower efficiency exit the market and the output will be reallocated to more efficient firms.

4. Data

The dataset is collected from Fitch Connect of an UK credit rating agency, Fitch Ratings. It contains an unbalanced panel data set of bank-specific variables from UK banks’ balance sheets between 2007 and 2015.[29] The data are drawn from the consolidated account whenever is available to avoid double-counting with using the same accounting standard, International Financial Reporting Standard (IFRS).[30] The observation sample consists different deposit-taking institutions which are the retail and consumer banks, private banks and commercial banks.

Using the intermediation approach as discussed in Section 3.1, banks are supposed to accept deposits and transform them into loans. Banks can also conduct other non-traditional activities apart from providing loans such as OBS. Some observations have been removed due to the missing data especially in total deposit and gross loans. Additionally, following the way from de-Ramon and Straughan (2016), banks with either less than 10% in loans-to-assets ratio or less than 20% in deposits-to-total assets are removed from the analysis.

Table 4.1 shows the summary the number of banks and observations by consolidation type and total using for the analysis after excluding some banks with the rule stated above. In the dataset, there are in total of 123 banks with 686 observations all over the year of 2007 to 2015. 49 of the banks are in non-consolidated data while 74 banks are consolidated.

Table 4.1 Number of banks and observations by consolidation type and year

| Consolidation type | # bank | # observations |

| Non-consolidated | 49 | 439 |

| Consolidated | 74 | 246 |

| Total | 123 | 685 |

Table 4.2 is the summary statistics of various variables and ratio calculated from the dataset which is used for the study. Apart from return on assets, cash and due from banks, and off-balance sheet, other variables have data throughout the whole dataset The total assets of banks in the dataset have a big range from the value of £31.7 million to about £2.4 trillion with a mean of £1.68 trillion. Input costs consist of from personnel expense, interest expense and other operating expense and the average costs of each input are measured with the ratio of each inputs cost to (i) total assets, (ii) total deposits, money market and short-term funding and (iii) fixed assets. Interest expense is the highest among these three inputs which is because banks are traditionally paid interests to the depositors and investors. The standard deviation of total assets, gross loans and total deposits are the highest with a big value from about 157461 to 391692 which can show the dataset contains banks with different size so that it will be favourable for the competition analysis in this study.

Table 4.2 Summary Statistics of variables

|

Variable |

Obs | Mean | Standard

Deviation |

Minimum | Maximum |

| Key Variables | |||||

| Input costs | |||||

| (i) Personnel Expense (£m) | 685 | 1047.0 | 2584.8 | 0.4 | 14262.7 |

| – ratio to total assets | 685 | 0.01090 | 0.01192 | 0.0001967 | 0.1449 |

| (ii) Interest expense (£m) | 685 | 1857.4 | 4436.2 | 0 | 33432.8 |

| – ratio to total deposits, money market and short-term funding | 685 | 0.02493 | 0.02330 | 0 | 0.2350 |

| (iii) Other operating expense (£m) | 685 | 1098.8 | 2561.7 | 0.1 | 14225 |

| – ratio to fixed assets | 685 | 17.99 | 81.56 | 0.08317 | 1074 |

| (i)+(ii)+(iii) | 685 | 4003.2 | 8824.9 | 1.9 | 59866.7 |

| – average cost (£m) | 685 | 0.9388 | 1.724 | 0.3442 | 43.63 |

| Total Revenue (£m) | 685 | 5133.1 | 11502.1 | 0.19 | 83601.2 |

| -ratio to total asset | 685 | 0.04840 | 0.02980 | 0.0008628 | 0.1956 |

| Profits | 685 | 276.3 | 2417.2 | -25691 | 14146.8 |

| – ratio to assets | 685 | 0.003049 | 0.02076 | -0.2874 | 0.05475 |

| Return on Assets | 351 | 268.9 | 911.8 | 0 | 7967.7 |

| Control variables | |||||

| Total equity (£m) | 685 | 7783.7 | 19089.9 | 7 | 133285.2 |

| – ratio to total asset | 685 | 0.08627 | 0.07343 | 0.0005223 | 0.5641 |

| Total assets (£m) | 685 | 167919.2 | 391692.1 | 31.64 | 2401652 |

| Gross loans (£m) | 685 | 75734.0 | 157460.5 | 4.9 | 885611 |

| – ratio to total asset | 685 | 0.5606 | 0.2335 | 0.1003 | 1.07 |

| Total deposits (£m) | 685 | 83642.0 | 175241.6 | 19.5 | 994998 |

| – ratio to total deposits, money market and short-term funding | 685 | 0.9626 | 0.07926 | 0.4210 | 1 |

| Total deposits, money market and short-term funding (£m) | 685 | 95442.4 | 205157 | 19.5 | 1150740 |

| Cash and due from banks (£m) | 669 | 7321.2 | 18996.0 | -0.9 | 108706 |

| – ratio to total deposits | 669 | 0.1019 | 0.1893 | -0.0003263 | 2.127 |

| Off-balance sheet activities (£m) | 583 | 37149.9 | 90925.6 | 0 | 538354.1 |

| – ratio to total assets | 583 | 0.1914 | 0.6104 | 0 | 12.60 |

5. Empirical Results

5.1 Panzar-Roose H-statistic

Following the reduced-form revenue equation in Equation (5), the regression models are estimated with fixed effects in order to account for heterogeneity.[31] In order to control for the heteroscedasticity and intragroup effects, the regressions are run with robustness and clustering. The result is shown in yearly by introducing time dummies into the regression and whole period. Due to some missing data of off-balance sheet activities (OBS) and cash & due from the banks (CASH), two regressions have been run to inspect whether the ratio of off-balance sheets to total assets (OBSAST) and the ratio cash & due from the bank to total deposits, short-term and money market funding (CASHDEP) have a strong effect to the model.

Table 5.1.1: H-statistic of whole period: fixed effects[32]

| Variables | H1 | H2 |

| ln(P1) | 0.272**

(0.007) |

0.346***

(0.000) |

| ln(P2) | 0.377***

(0.000) |

0.362***

(0.000) |

| ln(P3) | -0.0052

(0.800) |

0.0072

(0.738) |

| ln(EQAST) | 0.0555

(0.349) |

0.0533

(0.492) |

| ln(AST) | 0.0569

(0.350) |

0.00799

(0.852) |

| ln(LOANAST) | 0.184*

(0.05) |

0.0632

(0.407) |

| ln(DEP ) | -0.147

(0.331) |

-0.196

(0.155) |

| ln(CASHDEP) | -0.0259*

(0.045) |

|

| ln(OBSAST) | 0.0248

(0.281) |

|

| Constant | -0.57

(0.334) |

0.195

(0.641) |

| Observations | 683 | 559 |

| Adjusted R-squared | 0.604 | 0.671 |

| H statistic | 0.6438 | 0.7152 |

| F-test (

H statistic=0) |

53.2 | 111.26 |

| Prob>F | 0.000 | 0.000 |

| F-test (

H statistic=1) |

26.32 | 17.57 |

| Prob>F | 0.0001 | 0.0001 |

Notes: p-value in parentheses: * p

Table 5.1.1 shows the two regression results with the value of coefficient of each bank-control variable, H-statistic (sum of the coefficients of P1, P2 and P3), F-test for jointly significant test and some other associated statistic for whole period. For simplicity, H1 will be indicated as the regression result that excluding OBSAST and CASHDEP while H2 is the result that including OBSAST and CASHDEP. The estimated H-statistic for whole period in both regressions have shown the same result that the UK banking industry is in monopolistic competition with the similar value of 0.6 in H1 and 0.7 in H2.[33] The results are consistent with the previous studies which also find that UK banking industry is under the monopolistic competition (see among other which are stated in Table 2.1). However, the value of H-statistic is more double than some other recent studies which are normally around 0.2-0.5 on average in UK banking market (Casu and Giardone, 2006; Scheack et al., 2009; Scheack and Cihák, 2012). Some literature finds a similar H-statistic with this study but in early 2000s (Claessens and Laven, 2004; Carbó et al., 2009).

The table also reflects the p-value and coefficient and each variable which can show the significance level. In terms of the H-statistics, the coefficient from the three inputs indicates the elasticities of the total revenue with respect to each factor price. Individually, the p-value of average cost of labour (P1) and average cost of deposits (P2) in both H1 and H2 are equal to 0 which mean that they are statistically significant in 5% significant level which they are different from to 0. However, average cost of labour (P3) has a relatively high p-value which can indicate that it may not be statistically significant. Moreover, the sign of the coefficient of P3 is different whichthe one in H1 has a negative sign so it suggests a negative correlation with the total revenue.

In addition, the F-test of the H-statistic also shows that it is jointly significant which the null hypothesis (H-statistic

=0) is rejected in any significance level. The null hypothesis (H-statistic

=1) is also rejected with a low p-value nearly equal to 0. It can mean that H-statistics here will only take the range between 0 and 1 in UK so that the banking market is indeed in the monopolistic competition which is match to the finding Casu and Giardone (2006).

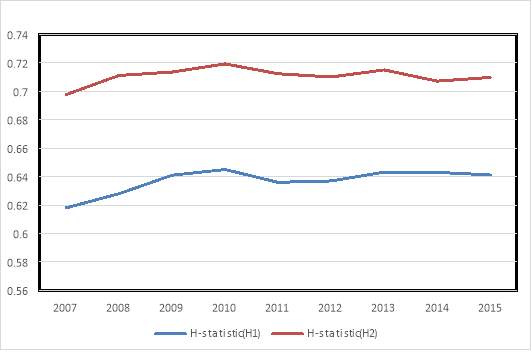

In order to investigate the H-statistic by year, it can be done by including time dummies into the regressions (Equation 7). Figure 5.1.1 shows the change in H-statistic over the 2007 to 2015.

Over the period, the competition does not fluctuate a lot in terms of the value of the H-statistics. Both H1 and H2 have a very similar pattern of change in the competition measures which the H-statistic increases from 2007-2010 so the competition is more intense. This is consistent with the finding of UK banking competition in the period of 2007-2010 in Weill (2013) and de-Ramon and Straughan (2016) in the year of 2007-2008. It is followed by a decrease in the value from 2010-2012 and quite a small change in value after 2012.[34] However, the value of H-statistics here is comparatively higher than their findings that calculated which is around 0.2-0.3 for the study period here.

Figure 5.1.1: H-statistic over 2007-2005

5.2 Boone Indicator

By using Equation (13), it is run under a panel regression with fixed effects. The regressions are run with robustness and clustering to eliminate the heteroscedasticity and intragroup effects. Follow the method from Scheack and Cihák (2014)[35] and de-Ramon and Straughan (2016), time dummies will be included for each year and it will also interact with the average costs (cit) in order to estimate the effects for each year. Therefore, the Boone indicator is the coefficient of ln(cit).

With the similar approach used from constructing the PR H-statistic, it has been included two situations which OBSAST and CASHDEP is removed in H1 when H2 still includes OBSAST. Table 5.2.1 shows the regression result, estimated Boone indicator (the coefficient of average cost,

ln(cit)), t-test for Boone indicator and some other related statistic. The result shows a similar result in Bonne indicator with the value of

-0.046in H1 and

-0.029in H2. As the value is closed to 0, it indicates that the UK banking competition is not really that intense even the industry is in monopolistic competition. This result is also consistent with previous studies which have been included in Table 2.1. The value of Boone indicator is quite similar to the finding in Scheack and Cihák (2010, 2014) but it is different with the value found in de-Ramon and Straughan (2016).

Table 5.2.1: Boone indicator for whole period: fixed effects

| Variables | H1 | H2 |

| ln(cit) | -0.0455***

(0.000) |

-0.0290***

(0.000) |

| ln(EQAST) | -0.00304

(0.300) |

0.00189

(0.385) |

| ln(AST) | 0.00107

(0.705) |

-0.00144

(0.433) |

| ln(LOANAST) | 0.00871

(0.235) |

-0.00148

(0.658) |

| ln(DEP ) | -0.00233

(0.818) |

0.000772

(0.944) |

| ln(CASHDEP) | -0.000823*

(0.013) |

|

| ln(OBSAST) | 0.00104

(0.142) |

|

| Constant | -0.0179

(0.493) |

0.0150

(0.356) |

| Observations | 685 | 561 |

| Adjusted R-squared | 0.426 | 0.215 |

| Boone indicator | -0.0455 | -0.0290 |

| t-test (

Boone indicator=0) |

-4.76 | -5.64 |

| Prob>t | 0.000 | 0.000 |

Note: p-value in parentheses

The table also shows the other coefficients and the t statistics of each variable. The coefficient of the average cost

(cit)is in negative in both H1 and H2 which is in line with the theoretical range of the Bonne indicator. It reflects that average cost has a negative relationship with the dependent variable (profit). By taking the t-test for the null hypothesis in which the Boone indicator is equal to 0 means that the market is not competitive. The result of the p-value with the value of 0 shows that the null hypothesis is rejected so that the Boone indicator is statistically significant and its value is different from 0.

Figure 5.2.1: Boone indicator over 2007-2015

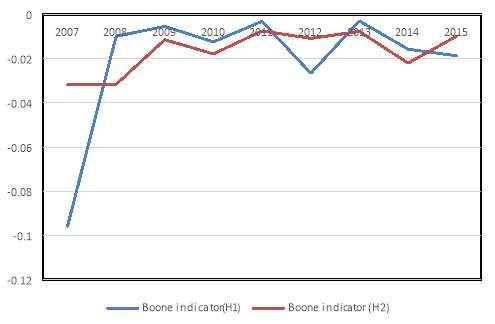

Moreover, in order to inspect the change in Bonne indicator in each year. Separated regressions are run to give the result of Bonne indicator with the specification in Equation (14) by adding time dummies. Figure 5.2.1 is the estimated value of the indicator over the year in 2007-2015. [36] The Boone indicator fluctuates over the whole study period which is consistent with the finding from de-Ramon and Straughan (2016, Figure 5.6). The pattern of Boone indicator of both H1 and H2 is similar to the finding to de-Ramon and Straughan (2016) and H2 almost has the same trend with them.

The Boone indicator is less negative from around 2007-2009 which indicates a reduction in competition.[37] This effect could be the result of Global Financial Crisis in 2007-2008. The global financial system was greatly affected by the crisis so that some financial institutions like banks were forced to close due to the insolvency which results in bankruptcy or acquired by the national government or other company.[38] The change in the pattern of Boone indicator from 2010-2013 is also reflected in de-Ramon and Straughan (2016, Figure 5.6). From 2010 to 2012, the indicator becomes more negative which may indicate a slow recovery in bank industry so the competition increases. The value of the Boone indicator is less negative between 2012 and 2013 which reflects a less intense competition. In 2014-2015, it shows a difference in change in competition in in H1 and H2. However, there still are not other similar competition studies which able to show the consistency for the trend after 2013.

5.3 Comparison between Two Competition Measures

Appendix C has shown the detail results of both H-statistic and Boone indicator with the associated test statistics and p-value in each year. In the case of Panzar-Roose model, the p-value of both H1 and H2 are equal to 0 in every year which indicates that the H-statistics are statistically significant in all the year. It shows that the UK banking industry is not a monopoly market in over the study period. However, it is different from the case of Boone’s model. By comparing H1 and H2, it seems that the Boone indicator is more statistically significant in H2.

Five of the years of nine years have a low p-value with p-value=0 in 2007 and 2008. The Boone indicator is relatively low in other year so that the Boone indicator is significantly greater than 0. In H1, except the p-value in 2007 (p-value=0) and low in p-value from 2010, 2012, 2014 and 2015, other years give out a comparatively high p-value which the p-value in 2013 is equal to 0.97. This can suggest that there is a high possibility that the Boone indicator of some years can be equal to 0 by using H1 which is not really accurate to the reality that the UK banking market is not a monopoly market. This can suggest that a better choice of estimation methods or more observations are needed in order to give a better result.

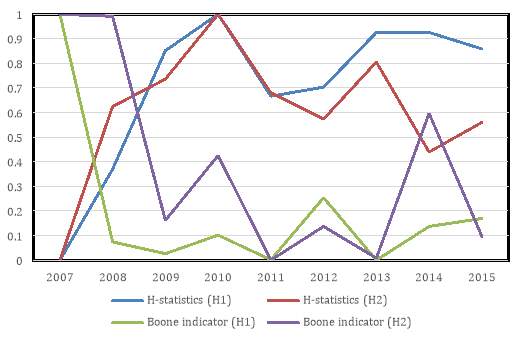

Figure 5.3.1 shows the evolution of two competition indicators along with the Appendix C. Due to the small change in the value of both indicators, they have been normalised and rescaled with the range between 0 to 1 so that they can be comparable.[39] The arrow indicates the direction of the degree of competition with 1 equal to a high competition.

Figure 5.3.1 Combined competition measures

Apart from the year of 2007-2010, both H-statistics and Boone indicator give the result are similar in the pattern. H-statistics increases initially while Boone indicator decreases at first in both H1 and H2. This inconsistency between two measures in 2008-2010 is indeed matched to the findings de-Ramon and Straughan (2016) which has a closed pattern. However, the level of the competition does not restore afterwards which Boone indicator does not increase as high as in 2007 and H-statistic does not decrease as low as 2007. H-statistics reaches the peak in 2010 while Boone indictor reaches the lowest point in 2011 and 2013. In spite of the difference in change in direction of competition intensity at 2007-2009, it shows the consistency in both measures after 2009.

6. Conclusion

This study includes two competition measures, Panzar-Roose H-statistics and Boone indicator, throughout the period of 2007-2015 which includes the financial crisis period (2007-2008) and post-crisis period (2009-2015). Two cases are used to investigate when H1 is the case excluding two variables (OBSAST and CAHSDEP) which have missing data and H2 including both variables. With the given data, it seems that H2 has a greater explanatory effect than H1 as the p-value of CASHDEP shows that it is significantly different from zero while OBSAST is not. This can be explained by having more missing data from OBSAST than CASHDEP and suggested that using H2 without OBSAST may be a better choice with the available dataset in this study.

There is an increase competition from H-statistic in competition over the period. On average, the indicator shows a high value of 0.6 in H1 and 0.7 in H2 which indicates a relatively strong competition. In the case of Boone indicator, the indicator takes the value of -0.05 in H1 and -0.03 in H2 which quite closed to 0. It means that the competition is not sufficiently high in the UK banking. Even the value of two indicators changes differently at first (2007-2009) in which H-statistics shows an increase in competition while the Boone indicator shows a decrease in competition, both of the measures seem quite consistent in the way they vary after 2009 as well the recent studies. As both of the measures fluctuates over the period, it is hard to estimate the trend after 2015.

All previous empirical studies show that the UK banking is indeed under a monopolistic competition which is matched to the reality. But it seems that the competition intensity in th UK in the 2010s is much lower than the 1990s and 2000s which also has been decreased throughout the year. In the line with the previous studies, it seems that accessing H-statistics and Boone indicator using H2 is a better approach. With the significant decrease in competition throughout the year, it may be better to update banking regulations and make sure it can restore the competition level in the 1990s to provide better services to customers with lower prices and maintain the financial stability.

References

Andrieşa A. M., & Căprarua, B. (2014). “The nexus between competition and efficiency: The European banking industries experience”. International Business Review. Vol.23. No. 3, pp.566–579.

Baumol, W. J., & Oates, W. E. (1988). The theory of environmental policy. Cambridge University Press.

Baumol, W., Panzar, J., & Willig, R. (1982). Contestable markets and the theory of market structure. Nueva York, Harcourt Brace Javanovich, Inc.

BBC News (2008, February 17). Northern Rock to be nationalised. Retrieved from http://news.bbc.co.uk/1/hi/business/7249575.stm

BBC News (2011, November 17). Northern Rock sold to Virgin Money. Retrieved from http://www.bbc.co.uk/news/business-15769886

Berger, A. N. (1995). The profit-structure relationship in banking–tests of market-power and efficient-structure hypotheses. Journal of Money, Credit and Banking, 27(2), pp.404-431.

Biker, Jacob A., Shaffer, S., & Spierdijk, L. (2012). Assessing competition with the Panzar-Roose Model. The Review of Economics and Statistics, 94(4), pp.1025-1044.

Bikker, J. A., & Groeneveld, J. M. (1998). Competition and concentration in the EU banking industry (Vol. 8). De Nederlandsche Bank NV.

Bikker, J. A., Shaffer, S., & Spierdijk, L. (2009). Assessing competition with the Panzar-Roose model: The role of scale, costs and equilibrium. Discussion Paper Series/Tijalling C. Koopmans Research Institute, 9(27).

Bikker, Jacob A. and Haaf, K., 2002. Competition, concentration and their relationship: An empirical analysis of the banking industry. Journal of Banking & Finance, 26(11), pp.2191-2214.

Boone, J. (2000). Competition. CEPR Discussion Paper Series (No. 2636).

Boone, J. (2004). A new way to measure competition. CEPR Discussion Paper Series (No. 4330).

Boone, J. (2008). A new way to measure competition. The Economic Journal, 118(531), pp.1245-1261.

Boone, J., Griffith, R. & Harrison, R. (2004). Measuring competition. In Encore Meeting.

Boone, J., Griffith, R. & Harrison, R. (2005). Measuring competition. Advanced Institute of Management Research Paper (No.22)

Boone, J., van Ours, J. C., & Wiel, H. V. D. (2007). How (not) to measure competition. TILEC Discussion Paper (No. 14).

Bresnahan, T. F. (1989). Empirical studies of industries with market power. Handbook of industrial organization, 2, pp.1011-1057.

Callen, T. S., & Lomax, J. W. (1990). The development of the building societies sector in the 1980s. Bank of England Quarterly Bulletin, 30(4), pp. 503-10.

Carbó, S., Humphrey, D., Maudos, J., & Molyneux, P. (2009). Cross-country comparisons of competition and pricing power in European banking. Journal of International Money and Finance, 28(1), pp.115-134.

Casu, B., & Girardone, C. (2006). Bank competition, concentration and efficiency in the single European market. The Manchester School, 74(4), pp.441-468.

Claessens, S., & Laeven, L. (2004). What drives bank competition? Some international evidence. Journal of Money, Credit, and Banking, 36(3), pp.563-583.

Colwell, R. J., & Davis, E. P. (1992). Output and productivity in banking. The Scandinavian Journal of Economics, S111-S129.

De Bandt, O., & Davis, E. P. (2000). Competition, contestability and market structure in European banking sectors on the eve of EMU. Journal of Banking & Finance, 24(6), 1045-1066.

Demsetz, H. (1974). Two systems of belief about monopoly. in H. J. Goldschmid H. M. Mann & J. F. Weston (eds). Industrail Concetration: the New Learning, Boston, MA, Little Brown, pp.163-184.

Friedman, J. W., & Samuelson, L. (1990). Subgame perfect equilibrium with continuous reaction functions. Games and Economic Behavior, 2(4), pp.304-324.

Friedman, J. W., & Samuelson, L. (1994). Continuous reaction functions in duopolies. Games and Economic Behavior, 6(1), pp.55-82.

Herfindahl, O. C. (1950). Concentration in U.S steel industry (Doctoral dissertation). Columbia University.

Hicks, J. R. (1935). Annual survey of economic theory: the theory of monopoly. Econometrica: Journal of the Econometric Society, 1-20.

Hirschman, A.O. (1945). National power and the structure of foreign trade. Berkeley: University of California Press.

Iwata, G. (1974). Measurement of conjectural variations in oligopoly. Econometrica: Journal of the Econometric Society, pp.947-966.

Lau, L. J. (1982). On identifying the degree of competitiveness from industry price and output data. Economics Letters, 10(1-2), pp.93-99.

Lepetit, L., Nys, E., Rous, P., & Tarazi, A. (2008), Bank income structure and risk: An empirical analysis of European banks. Journal of Banking & Finance, 32(8), pp.1452-1467.

Lerner, A. P. (1934). The concept of monopoly and the measurement of monopoly power. The Review of Economic Studies, 1(3), pp.157-135.

Matousek, R., Rughoo, A., Sarantis, N., & Assaf, A. G. (2015). Bank performance and convergence during the financial crisis: Evidence from the ‘old’ European Union and Eurozone. Journal of Banking & Finance, 52, 208-216.

Molyneux, P., Lloyd-Williams, D.M., & Thornton, J. (1994). Competitive conditions in European banking. Journal of Banking and Finance, 18(3), pp.445-449.

Nathan, A., & Neave, E.H. (1989). Competition and contestability in Canadas financial system: Empirical results. Canadian Journal of Economics, 22, pp.576–594.

Nedeland. Centraal Planbureau (2000). Measuring competition: how are cost differentials mapped into profit differentials?. CPB Netherlands Bureau for Economic Policy Analysis (No. 131).

Panzar, J. C., & Rosse, J. N. (1982). Structure, conduct, and comparative statistics. Bell Telephone Laboratories.

Panzar, J. C., & Rosse, J. N. (1987). Testing for “monopoly” equilibrium. The Journal of Industrial Economics, pp.443-456.

Rosse, J. N., & Panzar, J. C. (1977). Chamberlin vs. Robinson: an empirical test for monopoly rents. Bell Laboratories Economics Discussion Paper.

Schaeck, K., & Čihák, M. (2008). How does competition affect efficiency and soundness in banking? New empirical evidence. ECB Working Paper, 932.

Schaeck, K., & Čihák, M. (2010). Competition, efficiency, and soundness in banking: An industrial organization perspective. European Banking Center Discussion Paper, 2010-20S.

Schaeck, K., & Cihak, M. (2012). Banking competition and capital ratios. European Financial Management, 18(5), pp.836-866.

Schaeck, K., & Cihák, M. (2014). Competition, efficiency, and stability in banking. Financial Management, 43(1), pp.215-241

Schaeck, K., Cihak, M., & Wolfe, S. (2009). Are competitive banking systems more stable?. Journal of Money, Credit and Banking, 41(4), pp.711-734.

Schaeck, K., Cihak, M., & Wolfe, S. (2009). Are competitive banking systems more stable?. Journal of Money, Credit and Banking, 41(4), pp.711-734.

Schiersch, A., & Schmidt-Ehmcke, J. (2010). Empiricism meets theory: Is the Boone-indicator applicable?. DIW Berlin Discussion Paper, 1030.

Shaffer, S. (1982). ‘Non-structural Test for Competition in Financial Markets’, Bank Structure and Competition, Conference Proceedings, Chicago, IL, Federal Reserve Bank of Chicago, pp. 225–233.

Shaffer, S. L. (2004). Comment on” What Drives Bank Competition? Some International Evidence”. Journal of Money, Credit, and Banking, 36(3), pp.585-592.

Shaffer, S., & Spierdijk, L. (2015). The Panzar–Rosse revenue test and market power in banking. Journal of Banking & Finance, 61, pp.340-347.

Staikouras, C. K., & Koutsomanoli‐Fillipaki, A. (2006). Competition and concentration in the new European banking landscape. European Financial Management, 12(3), pp.443-482.

Stigler, G. J. (1964). A theory of oligopoly. Journal of political Economy, 72(1), pp.44-61.

van Leuvensteijn, M., Bikker, J. A., van Rixtel, A. A., & Sørensen, C. K. (2007). A new approach to measuring competition in the loan markets of the euro area. Applied Economics, 43(23). pp.3155-3157.

Vives, X. (2001). Competition in the changing world of banking. Oxford Review of Economics Policy, 17(4), pp.535-545.

Weill, L. (2004). On the relationship between competition and efficiency in the EU banking sectors. Kredit und Kapital, pp. 329-352.

Weill, L. (2013). Bank competition in the EU: How has it evolved?. Journal of International Financial Markets, Institutions and Money, 26, pp.100-112.Goddard, J and Wilson, J (2009). Competition in banking: a disequilibrium approach. Journal of Banking & Finance, 33(12), pp.2282-2292.

Appendices

Appendix A: Models used in the study and their assumptions1

| Panzar-Roose | Boone indicator | ||

| H-statistic | Equilibrium test | ||

| Assumptions | Translog revenue

function |

Translog production

function |

Linear

relationship |

| Perfect competition condition | No pricing market-power | Input prices are related to profits | |

| Dependent variable | Total revenue (scaled by total assets) | Return on assets | Profits/total assets |

| Explanatory variables | Input prices | Input prices | Average cost (proxy for efficiency) |

| Control variables |

|

||

| Testing hypothesis | F-test on the null hypothesis that H-statistics equals to 0 | F-test on the null hypothesis that H-statistics equals to 0 | t-test on the null hypothesis that Boone indicator equals to 0 |

| Source: de-Ramon and Straughan (2016, Appendix 1)2 | |||

Notes:

1 All above regressions are run with fixed-effects panel regression with clustering and robustness to eliminate any intragroup effects and heteroskedasticity.

2 de-Ramon and Strughan (2016) construct a similar table.

Appendix B: Equilibrium test for Panzar-Roose model

The following table shows the results of long-run equilibrium test. The p-value is equal to 0.055 H1 and 0.2123 in H2 on average which means null hypothesis (

F=0) cannot be rejected with 5%. This is applied to H2 and all the year. It can be concluded the null hypothesis is failed to reject for all the year in both H1 and H2 at 5%. Thus, the UK banking market was in the long-run equilibrium among the observations used in this study from 2007-2015. De-Ramon and Straughan (2016) does find out there were long-run equilibrium in 2007-2009 and 2011-2013 but not in 2010. The difference in findings can be explained by the choices of the control variables, number of observations and estimation methods. They include different variables such as risk weight, tier 1 to total capital ratio and provisions to assets ratio.

| H1 | H2 | |||

| Year | F-Statistic | p-value | F-Statistic | p-value |

| 2007 | 3.08 | 0.0833 | 1.34 | 0.2511 |

| 2008 | 3.71 | 0.0577 | 1.57 | 0.2141 |

| 2009 | 3.66 | 0.0594 | 1.38 | 0.2436 |

| 2010 | 3.75 | 0.0566 | 1.45 | 0.2324 |

| 2011 | 3.61 | 0.0611 | 1.59 | 0.2116 |

| 2012 | 3.75 | 0.0563 | 1.59 | 0.2117 |

| 2013 | 3.87 | 0.0526 | 1.6 | 0.2099 |

| 2014 | 3.81 | 0.0545 | 1.61 | 0.2094 |

| 2015 | 3.38 | 0.0699 | 1.16 | 0.2848 |

| Average | 3.80 | 0.0550 | 1.59 | 0.2123 |

Notes:

(i) H1 does not include OBSAST and CASHDEP in the regression.

(ii) H2 includes OBSAST in the regression.

Appendix C: H-statistic and Bonne indicator across years and associated significance test

The following table shows the value of both competition indicators which are estimated by the panel fixed effects with the control of the heteroskedasticity (robustness) and intragroup effects (clustering). The results of two indicators are calculated with two regressions (H1 and H2).(ii)(iii) The table also indicates the test statistic and p-value which is the significance test.

| Year | PRH | B | ||||||||||

| H1 | H2 | H1 | H2 | |||||||||

| H | F-statistic | p-value | H | t-statistic | p-value | B | F-statistic | p-value | B | t-statistic | p-value | |

| 2007 | 0.618 | 53.24 | 0.000 | 0.6977 | 118.68 | 0.000 | -0.0959 | -8.67 | 0.000 | -0.03183 | -5.23 | 0.000 |

| 2008 | 0.628 | 51.17 | 0.000 | 0.7112 | 109.46 | 0.000 | -0.009843 | -0.75 | 0.453 | -0.03162 | -4.43 | 0.000 |

| 2009 | 0.641 | 51.65 | 0.000 | 0.7136 | 108.97 | 0.000 | -0.005399 | -0.74 | 0.461 | -0.01138 | -2.54 | 0.013 |

| 2010 | 0.645 | 53.86 | 0.000 | 0.7193 | 112.7 | 0.000 | -0.01239 | -2.28 | 0.024 | -0.01782 | -2.35 | 0.02 |

| 2011 | 0.636 | 54.37 | 0.000 | 0.7124 | 112.7 | 0.000 | -0.003071 | -0.37 | 0.715 | -0.00744 | -1.70 | 0.093 |

| 2012 | 0.637 | 52.14 | 0.000 | 0.7101 | 112.84 | 0.000 | -0.02655 | -1.44 | 0.153 | -0.01080 | -2.38 | 0.019 |

| 2013 | 0.643 | 52.86 | 0.000 | 0.7151 | 111.430 | 0.000 | -0.002927 | -0.04 | 0.971 | -0.00765 | -1.14 | 0.255 |

| 2014 | 0.6430 | 53.49 | 0.000 | 0.7072 | 111.75 | 0.000 | -0.0157 | -2.48 | 0.014 | -0.02199 | -3.27 | 0.001 |

| 2015 | 0.6412 | 55.27 | 0.000 | 0.7098 | 115.03 | 0.000 | -0.01870 | -3.15 | 0.002 | -0.00979 | -1.56 | 0.121 |

(i) PRH: Ponzar-Roose Η-statistic; B: Boone indicator

(ii) H1 does not include OBSAST and CASHDEP in the regression.

(iii) H2 includes OBSAST in the regression.

(iv) The test statistic is calculated with robust standard error.

[1]Student Number: 1405267; Email: khchun@essex.ac.uk; Supervisor: Professor Katharine Rockett.; A dissertation submitted to the University of Essex in partial fulfilment of the requirements for the degree of BSc (Hons) Economics, Department of Economics.

[2]Special thanks to Professor Claudia Girardone for specific suggestions on my topic with her research experiences. I would also like to thanks Dr. Domenico Tabasso and Dr. Domenico for the advices on empirical and technical methods.

[3] The “corset” was imposed to penalise the banks that their interest-bearing eligible liabilities (IBELs) expanded faster than the regulated rate imposed by the Bank of England).

[4] HHI was first introduced by A.O. Hirschman in 1945 on investigating concentration in U.S. national and foreign power market. In 1950, O. C. Herfindahl extended the model and applied it on U.S. steel industry.

[5] Hicks (1935) suggested that managers enjoy a quiet life free from competition due to the monopoly power which increase in concentration will decrease the competition and hence the efficiency.

[6] See detail of the hypothesis in Section 3.2.

[7] Casu and Girardone (2006) conclude that competition is negatively related efficiency by finding out that the efficiency score is negative when they introduce it into the Panzar-Rosse model.

[8] Firms cannot maintain reasonable profits under a market with easy entry and exit condition for new firms. Even though the market concentration is sufficiently high, the incumbent firms will be forced to react strategically to deter entry of new firms. (Carbó et al., 2009).

a href="#_ftnref9">[9] Bikker et al. (2009) stated that previous empirical studies found that competition is more intense and market power can be greater than the industry suggested. Therefore, SCP is an “extremely unreliable” competition measures as the mismatch can go either direction.

[10] Shaffer (2004) argues that condition long-run equilibrium is only needed under a perfectly competitive market.

[11] Matthew et al. (2007) analysis the competition two sub-periods (1980-1991 and 1992-2004) while de-Ramon and Straughan (2016) include ehight periods (1989-1994, 1995-1997, 1998-2000, 2000-2003,2004-2007, 2008-2009, 2010-2011 and 2012-2013).

[12] PR H-statistics normally takes the value between 0 and 1 but some studies found that the indicator can be in negative. Higher the value is, higher the competition is.

[13] Caus and Girardone (2006) use Data Envelopment Analysis (DEA) to conduct the efficiency score of banking market include in the Panzar-Roose model and compare the regression without the DEA score. They found that the countries with highest score generate smallest total revenue per euro of assets.

[14] Boone indicator takes the value from

-∞to 0. The greater the value in absolute value, the higher the competition.

[15]A separate test is needed for checking whether most of the banks are in the long-run equilibrium.

[16] The PR model also has a strong assumption that the cost, demand and react function is continuous. It has been shown this is not restrictive assumption by Friedman and Samuelson (1990,1994).

[17]De Bandt and Davis (2000) suggests that using log-transformation is to improve the goodness-of-fit of the regression model so that possible simultaneity bias can be reduced.

[18]See table 1 in Bikker et al. (2012) for more examples of the choices of TR in some selected previous studies.

Rxi,zi =Axiαzi(e-1)/ewhere

Ais the total factor productivity. This can also mean that the firm is facing constant returns to scale in their business.

L=(e-1)/ewhere

H=1/L=e/(e-1)

[21]Using the total asset rather than the number of labour is because there are missing data of the staff numbers. There are similar practices found in previous literatures (Claessens and Laeven, 2004; Casu and Giardone, 2006)

[22] As there are no individual available data of short-term funding and different types of non-customer deposits, customer and short-term funding cannot be calculated and total deposits, money market funding and short-term funding has been replaced.

[23] See Casu and Giardone (2006) for the detail of the reasons of these chosen control variables.

[24] Same as situation as the proxy of

P3, therefore total deposits, money market funding and short-term funding has been used instead.

[25] Schaeck and Cihák (2014) stated that it is assumed that average cost is neither increasing nor decreasing with the change in output level which is consistent with the assumption on constant marginal cost stated from Boone (2004).

[26] Boone (2004) did not make references with intermediation approach to make assumptions on banks inputs and outputs.

[27] CPB (2000) uses the ratio of profits to total assets and dependent variable while Boone et al. (2004) uses the exact value of profits. However, van Levensteijn et al. (2007) uses market shares instead of profits.

[28] Van Levensteijn et al. (2007) uses marginal costs instead of estimating the average costs.

[29] All the data has been converted to British Pound by using the exchange rate on 19 April 2017.

[30] in order to keep the consistency of the data, only data in IFRS is used.

[31] The choice of using fixed effect has been used among different studies. Moreover, by using the Hausman test, it has been confirmed that using fixed effect instead of random effect is indeed suitable for the dataset and models in this study.

[32] In order to check the validity of the H-statistic results, different regression has been run for checking whether the market in the study period is in long-term equilibrium. See Appendix B for the test results.

[33] The value of H-statistic can be so varied due to the number of observations and the choices bank control variables and dependent variables.

[34] See Figure 5.3.1 in Section 5.3 to see a clear trend of the change in competition after normalisation.

[35] Scheack and Cihák (2014) use dynamic panel data estimators from Generalised Moment Method (GMM) based on the concerns on the jointly determination of performance and cost.

[36] See Appendix C for the regression result of each year. The value of Boone indicator is less negative here while de-Ramon and Straughan (2016) find the value from around

-2.6to

-3.4.

[37] Even though the result is consistent to de-Ramon and Straughan (2016), the small value of Boone indicator can be possibly caused by using different bank control variables and numbers of obervations.

[38] Northern Rock was nationalised by the UK government in 2008 (BBC News,2008 &2011). The bank was spilt into Northern Rock plc (banking) and NRAM plc (asset management) in 2010 which Northern Rock plc was sold to Virgin Money and NRAM plc is part of the UK Asset Resolution (UKAR) owned by government.

[39] By following de-Ramon and Straughan (2016), the indicators are normalised with the formula:

x’=(x-xmin)/(xmax-xmin), where

x’ is the value after normalisation, is the value of each year,

xmax is the maximum value of the indicator and

xmin is the minimum value of the indicator.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "Banking"

Banking can be defined as the business of a bank or someone employed in the banking industry. Used in a non-business sense, banking generally means carrying out activities related to the management of one’s bank accounts or finances.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: