Introduction of Microfinance to Empower Unemployed/Low Income Women

Info: 9281 words (37 pages) Dissertation

Published: 10th Dec 2019

Introduction of Microfinance to Empower Unemployed/Low Income Women in New Zealand

TABLE OF CONTENTS

Table of Contents

Executive Summary ………………………………………………5-7

Chapter 1 Introduction to Microfinance to empower Unemployed/Low Income women in New Zealand 8-10

1.1 Background………………………………………………..8

1.2 Reason……………………………………………………8

1.3 Objectives…………………………………………………9

1.4 Scope ……………………………………………………9

1.5 Limitations…………………………………………………9-10

Chapter 2 Literature Review ………………………………………….11-16

2.1 Introduction………………………………………………..11

2.2 Previous Studies on Factors that necessitate demand for Microfinance………12

2.3 Benefits of Microfinance ……………………………………..13

2.4 Microfinance in New Zealand…………………………………..14

2.5 Summary…………………………………………………15-16

Chapter 3 Method …………………………………………………17-19

3.1 Introduction……………………………………………….17

3.2 Secondary Research………………………………………….17

3.3 Quantitative……………………………………………….17

3.4 Qualitative…………………………………………………1

3.5 Scope……………………………………………………19

3.6 Limitations………………………………………………..19

Chapter 4 Findings and Discussion………………………………….20-22

4.1 Introduction……………………………………………….20

4.2 Findings………………………………………………….20

4.3 Discussion………………………………………………..21

4.4 Summary…………………………………………………22

Chapter 5 Conclusion and Recommendations…………………………..23-25

5.1 Conclusion………………………………………………..23

5.2 Recommendations ………………………………………….24-25

References……………………………………………………………… 26-28

Appendices……………………………………………29-33

Appendix A : Questionnaire…………………………………29-31

Executive Summary

Chapter one explores the introduction of Microfinance in New Zealand to empower unemployed and low income groups of women. This study examines the impact of Microfinance that has seen enormous growth in popularity in the recent past because it is a concept and model that, at its foundation, appeals to the inborn entrepreneurial spirit of human beings. People are not looking for a hand out, but instead a hand up; microfinance enables people to work their own way up the economic ladder, and that can be an extensively rewarding experience. Instead of poor people without opportunities, we begin to see micro-entrepreneurs with dignity and hope—working towards a better future for themselves and for their children. Academics and microfinance practitioners, advocate for much wider impact assessments of microfinance projects, other than financial impacts alone, for the true impact of microfinance to be understood. They argue that instead of using traditional financial impact assessments, assessments should be broadened to include social, cultural and political impacts on clients, their families and indeed the wider community. Applications of the findings from this research are cautioned. A small sample data set and inability to directly identify sources of causation, limited testing and interpretations from various authors can be drawn from this research.

Chapter two outlines the existing literature related to this topic. Microfinance tries hard to reduce poverty, augment productivity and income among the unemployed/ low-income households as well as a long term benefit of overall improvement in welfare amongst other things.To reach significant numbers of poor people; the easiest way was to form many informal groups such as self-help groups. Extensive evidence points to the fact that microfinance plays a major role in building their assets and lowering their vulnerability. Similarly this philosophy was applied to New Zealand and microfinancing is gaining more importance in today’s society.

Chapter three outlines the methodology employed within this report. Data used within this report emerges mostly from secondary research. The Fixed Effect Weighted Means model is used to test the associated estimates extracted for each microfinance and empowerment factors related to women and its association is provided. The qualitative part of the research is the primary research which consists of online surveys to women resident in New Zealand and an interview with finance personnel regarding Microfinance in New Zealand and their respective opinions.

Chapter four outlines the findings of the report. Historically, Microfinance Institutions (MFI) impact evaluations have been program assessments, basically every MFI that supports clients try to measure the overall effect of an MFI on client or community welfare. In many cases, the full package of program services includes many components: credit, educational social capital building, insurance, etc. Consequently, the weighted averages from the secondary research presented for the associations between microfinance measures and female empowerment measures, mainly point to either a significant association or a positive association. Supplementary findings from the primary research illustrates an apparent link between microfinance and the unemployed / low income women in New Zealand.

Chapter five explores the underlying drivers behind the findings emerging from this research. The minimum necessary sample size depends on the desired effect size (e.g desired percentage rise in income).Findings are not conclusive yet as I need a bigger sample size but even with a small sample there is a definite correlation between Microfinance and unemployed women. Extensive findings will be elaborated in the final submission of the research project.

Chapter six outlines the conclusions and recommendation of this research. The findings of this research though not conclusive (interim draft report) offers an indication of the perceived benefits and correlation between the introduction of Microfinance and unemployed / low income women in New Zealand. Formalized training within this area in New Zealand would expand knowledge base on Microfinance, enhance the capabilities of women within their community and align with international trends and leadership status for women.

Chapter 1 Introduction to Microfinance for Unemployed / Low Income Women in New Zealand

1.1 Background

Microfinance also known as Microcredit is a term used to offer financial services such as build up savings accounts, offer loans and insurance schemes against no collateral to people of low or limited income where access to traditional mainstream banking is very limited or facility of use is difficult (Burkett & Sheehan, 2009). Microfinance not only helps to reduce poverty but leads to lasting, holistic development of the individuals that avail Microfinance. It is not just a monetary means (financial tools) to an end but training provided alongside that helps empower entrepreneurs to build businesses, support their families and transform their communities. There are many groups within Microfinance that focus on women who are unemployed / low income which have transformed the lives of many women and their image in communities all around the globe. Microfinance has been and is very predominant in developing countries like Africa, Bangladesh, India but not so much in developed countries such as New Zealand.

1.2 Reasons

The motivation for this research is based on the number of unemployed people especially women in New Zealand who are very willing to work but are unable to find jobs or have very low income jobs (stuck at the same job for more than 10 years).The official unemployment rate in New Zealand is currently at an 8 year low of 4.8 percent. Seems like the kind of employment environment where the worker rules – where there is little competition for jobs, and bosses are so desperate for workers, hence offering great salaries and benefits but this is however not the real picture. The number of people who are jobless and ‘disheartened’ rivals the official number of unemployed – which was 128,000 in July 2016. There are 1 million New Zealanders not in jobs and not counted in either the unemployment or employment rate. Many of the 1 million people ‘not in the labour force’ are doing things like studying or caring for a family member (Worrall, 2017). Women and men have quite different patterns of participation in the labour market, principally because women take time out to care for their children.

Specifically, women who participate in the labour force, are more likely to work part time, and earn less than men (Appendix C – Table 2).

1.3 Objectives

Objectives within this research strive to;

- Understand the magnitude of unemployed / low income groups in New Zealand especially focussed on women

- How best to serve and help the unemployed / low income groups who live off monthly welfare benefits from the government within New Zealand;

- How training / collaborative measures have an impact on the empowerment of women; and it’s not just monetary

- Help women understand what Microfinance is in order to improve their lives and their outlook to future.

1.4 Scope

The scope of this research within this chapter is limited to an assessment of unemployed/ low income women within New Zealand and with the introduction of Microfinance how it can best reduce/ alleviate poverty, help them lead a better lifestyle.

1.5 Limitations

Limitations of this research arise from sensitivity to time, inability to meet key personnel who run Trusts, not for profit organisations for Microfinance in New Zealand and data availability. The collection of data, perceptions of key personnel experience, the definition of Microfinance performance in New Zealand within this report are reflective of data obtained from secondary research through reports and publications. Limitations bound to the collection of data is dependent on data from websites and annual publications.

Chapter 2 Literature Review

2.1 Introduction

Microfinance is the supply of financial services at a very small scale level and this in turn helps catering to the needs of poor individuals and households (Otero, 1999). The primary focus is on low-income households with the objective of promoting their quality of life. Microfinance was first introduced in developing countries and its popularity has caught attention worldwide. From the early 1970’s, microfinance is rapidly growing especially in the developing countries and definitely contributes to the commercial growth of a country (Ledgerwood, 1999). With the advent of microfinance the promise of reduction of poverty was fulfilled with goals set to make arrangement for providing financial assistance to the poor. In the same context microfinance can be introduced as a financial tool to help implement better lifestyles for women in New Zealand as there are many in the low income groups who cannot afford a square meal on their own. In general, Microfinance tries hard to reduce poverty, augment productivity and income among the unemployed/ low-income households as well as a long term benefit of overall improvement in welfare amongst other things (Armendariz & Morduch, 2010; Torre & Vento, 2006). According to Heen (2004), microfinance institutions have many different types of clients, females forming a vast majority, downsized workers, small farmers and micro-entrepreneurs living below the poverty line and gain from the benefits of the various microfinancing options. In addition to this it has been proved that women find it very restricting to borrow on credit terms and also have limited access to casual labour wage jobs (Pitt, Khandker, & Cartwright, 2006). In conclusion, most microfinance institutions lean toward giving more leverage for women with the hope to empower them in society. (Mayoux, 2001). The expectation is that targeting microfinance programs towards women would enable them to be empowered in various aspects of their lives. In comparison to men, women are better at managing credit risk and are considered a lesser risky proposition for Microfinance Institutions as they do not misuse credit (Garikipati, 2008). Even though New Zealand is a developed country there is a stark difference between the low incomes versus the high income groups. Microfinance if introduced in the coming years in New Zealand will definitely help to improve women’s lives and give them a better standing in society.

This section of the report looks to provide an overview of the background literature associated with the empowerment of women through microfinance in other countries and to prove there are similar circumstances within New Zealand and there is a definite demand through the primary research carried out. Microfinance is to be looked at as a good option within New Zealand to support lower income / unemployed women to help them have a place in society. This will be achieved through assessing the background literature associated with microfinance and women empowerment within an international setting and also formal literature specific to the field of women empowerment through microfinance as an option in New Zealand.

2.2 Previous studies on factors that necessitate demand for Microfinance

The demand for microfinance stems from the fact that the people are at a disadvantage in certain societies and are very poor. The access to loans from financial institutions is very limited either because of lack of collateral or very low income and hence excluded from regular banking practices (Helms, 2006). Small loans (Microcredit) is just one of the ways to help empower women; there are many other financial products that can be designed to help specifically target the low income groups. “In essence, the schemes involve non-collateralized, jointly liable, group-based lending with a frequent instalment schedule. Today, group lending is just one element that makes microfinance different from conventional banking. There are several other elements that make microfinance work effectively, including progressive lending, repayment schedules with weekly instalments, public repayment, and the targeting of women” (Armendáriz de Aghion and Morduch 2005). High interest rate can limit poor people’s access to financial services; For example the more money a person can put towards a down payment lowers the rate of interest, but the fact of the matter is there are many people who do not have any savings in the bank accounts and it is very difficult for many households to keep aside money (Otero, 1999). To reach significant numbers of poor people; the easiest way was to form many informal groups such as self-help groups. The current model links Self Help Groups with around 10-20 people made up especially of women to sources of finance from NGO’s or financial institutions (Ruthven, 2011). In addition to the above one of the key constraints is the lack of institutional and human capacity. Not only financial sustainability, it is the guidance, advice and support given by help groups that empower women to get on their feet, learn to survive and help create assets for themselves (Dichter, 1999).

2.3 Benefits of Microfinance and current trends in different markets

Eradicate Poverty and Hunger – Extensive evidence points to the fact that microfinance plays a major role in building their assets and lowering their vulnerability. For example Khandker’s 1998 study for the World Bank notes that: In Bangladesh 5% of the Grameen clients graduated out of poverty every year, were able to build assets and sustain in the coming years by participating in Microfinance programmes. To further add World Development Report (WDR) 2000/1, Sebstad and Cohen conclude, “Findings from a growing number of impact studies support the proposition that microcredit reduces vulnerability by building a strong and diversified base of household assets.”

Achieve universal education – This results in households that have access to microfinance spend more on education and the absenteeism is very low. Participation in microfinance programmes helps women to send their children to school especially in the higher primary grades. Furthermore, results from the BRAC-ICDDR, B studies (Chowdhury and Bhuiya, 1998) give us an indication of positive trends. “The percentage distribution group of children (11-14 years) achieving “basic education” (pre-determined level of mastery in reading, writing and arithmetic, as well as “life skills”) rose from 12.4% in 1992 (before the BRAC programme began in the area) to 24.0% in 1995 among the children of BRAC members” (Chowdhury and Bhuiya, 1998).

Promote gender equality and women’s empowerment – Many of the microfinance clients are female and therefore practically supports the theory of empowering women by increasing their contribution to household income, the value of their assets, and control over decisions that affect their lives. Cheston and Kuhn in their 2002 study for UNIFEM, found that decision-making roles of women clients from different regions increased tremendously after getting involved with microfinance programmes. For instance, the Women’s Empowerment Programme in Nepal found that 68% of its members were making decisions on property, family planning and daughters’ education, and also negotiating their children’s marriages (Littlefield, Murduch and Hashemi, 2003).

2.4 Microfinance in New Zealand

The first microfinance-like initiative in New Zealand was established by the Mäori Women’s Welfare League in 1987, and the first formal microfinance initiative was established by Nga Tangata Trust in 2011. As such, this is a relatively new sector in New Zealand. (Ayres-Warne & Palafox, 2005) found that access to no-interest loan schemes (NILS) in Australia:

“ offered real solutions to essential needs; assisted in helping people who were experiencing hardship and distress to feel better; improved people’s day to day lives; enabled parents to spend more time with children; reduced people’s embarrassment about their homes; created community advocates of the loans programmes; strengthened people’s money management skills; and improved people’s outlook on the future”. Similarly this philosophy was applied to New Zealand and microfinancing is gaining more importance in today’s society. In addition (Corrie, 2011) found that microfinance had positive impacts, but needed to be available in the context of other social services because of the complexity of the issues faced by vulnerable low-income families. Both the above were small Australian studies and there is limited information about microfinance in New Zealand. A 2012 article about the Nga Tangata Trust stated that in developed countries such as New Zealand, “the role of microfinance is to provide a path to engagement with mainstream lenders through access to financial literacy and affordable credit for asset-building.” In 2009, the Families Commission undertook research on issues faced by families accessing budgeting services. This report found that the causes of debt were complex and included income being inadequate, personal behaviours, family members having health and disability needs, and changes of circumstances (e.g. unemployment, birth of a child). It found that the easy availability of consumer credit was problematic, and that debt had major impacts on family well-being and led to children missing out on experiences. The study also found that many families prioritised debt repayments over food, which is of particular concern when there are young children in the family.

2.5 Summary

The literature reviewed here found microfinance more particularly leaning towards women, to be an opportunity, a tool to be used to alleviate poverty and live above the poverty line. In comparison to other countries Ministry of New Zealand stated that microfinance via social lending should be encouraged. Social Lending is “an organisation provides no or low cost loans to people where a social benefit, rather than a profit, is the main outcome. It is not well developed in New Zealand but there is an increasing appetite for it” (Ministry of Consumer Affairs, 2011). Clear criteria needs to be established regarding loans for necessities as opposed to wants. Partnerships between communities and non-finance groups with financial organisations – be it banks, second or third tier lenders, and especially credit unions, perhaps with some funding and promotional assistance from government. In addition, a range of microfinance service providers have been identified which are mostly Trusts that provide budget advice, help the member to start up a small scale enterprise and reduce vulnerability. An alternative approach would be for the Government itself to provide microcredit, for example, through Work and Income (as it already happens). However it would be preferable to generate a tailored response from the private and community sectors (Children’s Commissioner, 2013). One of the other opinions from the Children’s Commisioner in 2013 was that a KiwiBank can be given the role of prime provider of commercial capital to any new Government-mandated microfinance scheme.

In conclusion based on various sources of Microfinance one has to note that one size will not fit all because of the diverse range of circumstances that New Zealand families face. Therefore it is important that any microfinance programme that is recommended has to incorporate a robust systematic evaluation, including a good baseline of information, and agreed performance standards that should in my view be reported on publicly (Mallet, 2012).

Chapter 3 Methods of Research

3.1 Introduction

The fundamental measures of female empowerment are constructed mainly to capture the

multidimensional nature of the status of women with regards to key indicators such as mobility, decision making and independence, amongst other things (Mason, 1986). Hashemi, Schuler, and Riley (1996) argue that in conducting female empowerment assessments, the most challenging task is the development of a valid and reliable measurement index, given that empowerment can be considered from various perspectives. From the existing literature, it is apparent that there is no coherent measure of female empowerment. However, some indicators have been consistently considered as key determinants of empowerment mobility, political and legal awareness, economic security (Hashemi et al., 1996; Steele, Amin, & Naved, 1998), decision making ability (Hashemi et al., 1996; Mizan, 1993; Steele et al., 1998), and increase in assets and control over these assets (Goetz & Gupta, 1996; R. Montgomery, Bhattacharya, & Hulme, 1996).

3.2 Secondary Research

For the purpose of this report, quantitative data used stems from secondary research. The purpose of the report is to provide an indication of the proportional relationship between Microfinance and empowerment variables. This secondary research has been collected from reports of key authors in Microfinance.

3.3 QuantitativeModel Specification (Fixed Effect Weighted Means (FEEs)

One of the methods of calculation is fixed effect weighted means (FEEs). FEEs are less affected by potential publication bias than the random-effects weighted averages (Henmi & Copas, 2010; T Stanley, 2008; T. D. Stanley & Doucouliagos, 2014). Thus, we estimate FEEs and depend mainly on these for the relationship between our microfinance variables and female empowerment variables. The FEEs are calculated using the approach used by Thomas Stanley and Doucouliagos (2007) and De Dominicis, Florax , and Groot (2008), amongst others. It is reported as follows;

_ 2

X FEE = ∑ri ( 1 / SE^ ri )

___________________

2

∑ 1 / SE^ ri

__

Where X FEE is the fixed effect estimate weighted mean, and ri and SE ri remain as explained above. The FEEs account for the within-study variations by distributing weights, such that estimates that are less precise are assigned lower weights, while higher weights are assigned to more precise estimates.

3.4 Qualitative Methods

Qualitative methods (Survey – Appendix A, Interview script – Appendix B) allowed greater flexibility, spontaneity and adaptation of the interaction between me and the study participant. Qualitative methods such as interviews ask each participant questions which are open ended so as participants have the opportunity to respond in greater detail than is typically in the case of quantitative methods. In qualitative approach participants can answer in their own words, rather than choose from limited fixed options as in a quantitative methods (surveys, questionnaires).

3.5 Scope

The scope of this research within this chapter is limited to an assessment of unemployed/ low income women within New Zealand and with the introduction of Microfinance how it can best reduce/ alleviate poverty.

3.6 Limitations

Limitations of this research arise from sensitivity to time, inability to meet key personnel who run Trusts for women, not for profit organisations and various banks for Microfinance in New Zealand and data availability. The collection of data, perceptions of key personnel experience, the definition of Microfinance performance in New Zealand within this report are reflective of data obtained from primary and secondary research through online surveys, direct interview with finance personnel, reports and publications. This research report has further been limited as it is bound to the collection of data which is dependent on data from websites and annual publications.

Chapter 4 Findings and Discussion

4.1 Introduction

Impact evaluations can be used either to estimate the impact of a program or to evaluate the effect of a new product or policy. In either case the fundamental evaluation question is the same: “How are the lives of the participants different relative to how they would have been had the program product, service or policy not been implemented?”(Karlan and Goldberg, 2011). The first part of the question, how are the lives of the participants different, is the easy part. The second part, however is not. It requires measuring the empowerment factors as to how their lives would have been had the policy not been implemented (Karlan and Goldberg, 2011).

4.2 Findings

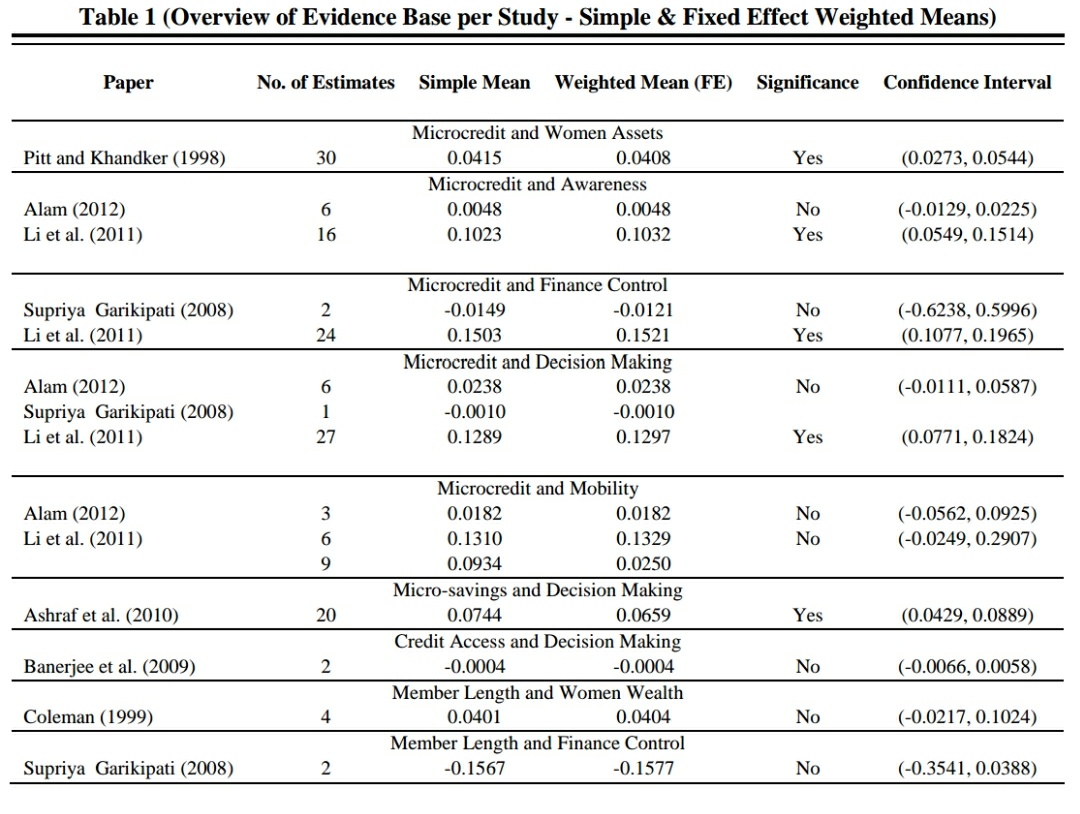

FEEs are reported in table 1. Pitt and Khandker (1998) report on the association between microcredit and women’s assets. The fixed effect weighted mean for 30 estimates reported for this relationship is positive and statistically significant. However, drawing on inferences put across by Cohen (1988), we conclude that this effect size (0.04), although statistically significant, is of no practical relevance. According to Cohen (1988) an effect size represents a large effect if its absolute value is greater than 0.04, medium effect if it is 0.1≤ x < 0.4 and small effect if it is less than 0.1. Still related to women’s assets, we find evidence of an association between the length of credit programme membership and women’s wealth. This conclusion is drawn based on evidence from four estimates presented by Coleman (1999).

Li, Gan, and Hu (2011) and Alam (2012) both report on the effects of microcredit on awareness. Of the 22 reported estimates on this relationship, 16 estimates present a positive and statistically significant weighted average of 0.10. Thus, based on the reported evidence, there is a positive association between microcredit and awareness. Similarly, evidence suggests a positive association between microcredit and control over finance. This is however a medium effect and is mainly drawn from 24 estimates extracted from Li et al. (2011). On the contrary, based on two estimates extracted from Supriya Garikipati (2008), we find significant association between the length of credit programme membership and control over finance.

Two estimates presented by Supriya Garikipati (2008) are associated with an insignificant weighted average. With regards to microcredit and decision making, we report 34 estimates extracted from three primary studies (Alam, 2012; Supriya Garikipati, 2008; Li et al., 2011).

Of the 34 estimates, 27 from one study (Li et al., 2011) is positive and statistically significant with a medium effect size of 0.13. Further, based on 20 estimates reported by Ashraf et al.

(2010) on the effect of micro-savings on decision making, we estimate a significant weighted average of 0.07, which represents a weak positive association between these two variables. In contrast, two estimates drawn from Banerjee et al. (2009), which report on the association between access to credit and decision making present a statistically insignificant average.

Lastly, a total of nine estimates drawn from two studies (Alam, 2012; Li et al., 2011) present significant association between microcredit and mobility. Consequently, the weighted averages presented for the associations between microfinance measures and female empowerment measures, mainly point to either a significant association or a medium positive association.

4.3 Discussion

We focus on four measures of microfinance, namely microcredit, access to credit, micro-savings and length of microfinance programme membership. Most observations reported in this meta-analysis are for the effects of microcredit on the various proxies of female empowerment. Two studies (Banerjee, Duflo, Glennerster, & Kinnan, 2009; H. Montgomery, 2006) use access to credit, in which cases, the independent variables captures whether or not households or individual have access to credit or participate in microcredit programmes. Coleman (1999) and Supriya Garikipati (2008) report effects using length of time in microcredit programme as a measure of microfinance. Lastly, Ashraf, Karlan, and Yin (2010) report effects using micro-savings.

For a study to be included in this meta-analysis, it had to be an empirical study that reports effect sizes on the association between at least one of the above mentioned measures for microfinance and at least one female empowerment proxy. A few estimates from the primary studies are reported based on empowerment indices created by putting together two or more of the above mentioned empowerment indicators. However, there is no common trend which determines how many, and which indicators should be combined to form the index. Thus, we do not report on empowerment indices. The findings through the online survey conducted and via interviews will be analysed and discussed in the Final Report.

4.4 Summary

Evaluating the impact of a microfinance program requires measuring of the impact of receiving the program’s services (typically credit, and sometimes savings), versus the counterfactual of not receiving the services. This proves to be more difficult than evaluating new products or policies because the self-help group must be drawn from non-clients, with whom the Microfinance Institution does not have a pre-existing relationship. In experimental evaluations of surveys online for Microfinance in New Zealand, participants are selected at the outset as if potential clients. When evaluating the impact of responses to the survey conducted almost all women are either unemployed or majority from low income groups would like to understand Microfinance better as their knowledge is limited on Microfinance, avail microfinance services and improve their lifestyle.

Chapter 5 Conclusion and Recommendations

Conclusion

Microfinance will generate positive impacts on the client’s business, the client well-being, the client’s family and the community. A thorough impact evaluation will trace the impacts across all of these domains. In entrepreneurial households, money can flow quite easily between the business and different members of the household. Credit is considered transferable, meaning it would be wrong to assume that money lent to a particular household member for a specific purpose will be used only by that person for that purpose. It is well-known, for instance, that loans dispersed for self-employment can often be diverted to more immediate household needs sue as food, medicine, and school fees, and that, even though a Microfinance Institution may target a woman, the loans may often end up transferred to her husband(Children’s Commissioner, 2013). As noted true microfinance programmes have the goal of poverty alleviation or prevention therefore this key principle leads to the criteria that loans should be to smooth a family’s income over an expense that is not part of day-to-day living only, and that will reduce the family’s poverty or likelihood of entering poverty by improving the quality of the family’s asset base, for example through the purchase of a car (which can support employment and participation in education).

Government providing administrative funding, setting policy, minimum standards, and outcome requirements, and promulgating best practice guidance. The role of commercial banks or private investors should be to provide capital and the link to the banking system required (with the intention of transferring these clients to mainstream financial services when possible), with NGOs and communities providing front-line services and feeding into future policy design and decisions. A coordination role may be necessary: this could be either undertaken by Government itself or contracted out to smaller financial institutions. Many female clients pride themselves of being able to manage a business and not having to be as dependent on their husbands as they used to be prior to joining the projects, even for small personal items such as cosmetics. They now have their own financial capital, and speak of their new skills and their confidence, as a result of the training they received and being part of the social network of the village bank groups. This research study contributes to the overall literature on microfinance from the perspective that it highlights that microfinance can be a very positive poverty alleviation tool. However, if impact assessment is not conducted then the role of microfinance in development is being undermined. In order to enhance donor-client relationships, this study also highlights the importance of understanding client’s needs and of how the project is impacting on their livelihoods, both positively and negatively. It is by having this level of understanding that an MFI can tailor its products to serve the needs of its clients and ultimately improve the lives of clients but also help the MFI achieve financial sustainability.

5.1 Recommendations

In order to gain an understanding of the role microfinance is playing in its focus on livelihood security, it should encourage and support partners to analyse and assess the wider impacts of the projects they are involved in. Microfinance partners should be encouraged to strive for financial sustainability, but not at the cost of their social mission. If donors put too much emphasis on financial sustainability, partners, worried about losing funding, will begin to ignore the poor and focus on more profitable clients. The onus therefore is on donors to commit to long-term funding with partners and map out sustainability plans with them. Partners should pay close attention to the nature and quality of financial services they offer if they are to serve the needs of their target market (Wright, 2000). Client’s needs change over time so MFIs need to be flexible and change their products and services when necessary so that their clients’ needs are met. The savings-first element in the projects enhances the impact of the projects in that it encourages clients to save and allows time for the banks to assess the credit worthiness of clients (Dichter, 1999). This savings element should be continued in each project and ongoing savings sensitisation should take place. The training element of each project is having a major impact on the skills and coincidence of clients and this should continue, and be expanded where possible.

REFERENCES

Armendariz, B., & Morduch, J. (2010). The Economics of Microfinance: MIT Press.

Ayres-Warne, V. and Palafox, J. (2005). NILS: Small Loans, Big Change. Good Shepherd Youth & Family Service, Collingwood, Melbourne.

Burkett, I & Sheehan, G. (2009). From the Margins to the Mainstream: The Challenges for Microfinance in Australia. Brotherhood of St Laurence and Forrester’s Community Finance, Melbourne.p.v

Cheston, Suzy and Lisa Kuhn. (2002). Empowering Women through Microfinance, Microcredit Summit, Washington and UNIFEM.

Children’s Commissioner, (2013). Mitigating Poverty with Microcredit. Retrieved from: http://www.occ.org.nz/assets/Uploads/Reports/Poverty/Mitigating-poverty-with-microcredit.pdf

Chowdhury, A.M.R. and A. Bhuiya. (1997). Socio-Economic Development and Health: some early tables from the BRAC-ICDDR, B Project in Bangladesh, Paper presented at “Economic Development and Health: Status”, Ottawa.

Corrie, T. (2011). Microfinance and the household economy: Financial inclusion, social and economic participation and material wellbeing.

Dichter, T.W. (1999). NGO’s in Microfinance: Past, Present and the Future.

Escaping the Debt Trap (2009). Experiences of New Zealand Families Accessing Budgeting Services. Retrieved from:

http://www.familiescommission.org.nz/sites/default/files/downloads/escaping-the-debt-trap.pdf

Family Health International: Qualitative Research Methods: A Data Collector’s Field Guide. Retrieved from:https://course.ccs.neu.edu/is4800sp12/resources/qualmethods.pdf

Garikipati, S. (2012). Microcredit and Women’s Empowerment: Through the Lens of Time-Use Data from Rural India. Development and Change, 43(3), 719-750. Retrieved from: http://www.blackwellpublishing.com/journal.asp?ref=0012-155X

Heen, S. (2004). Microfinance and Conflict: Toward a Conflict-Sensitive Approach. Fletcher School of Law and Diplomacy.

Helms, Bigit. 2006. Access for All: Building Inclusive Financial Systems. Washington, D.C.: World Bank

Ledgerwood, J. (1999). Microfinance Handbook. Sustainable Banking with the Poor. An Institutional and Financial Perspective, The World Bank, Washington D.C.

Littlefield, E., Murduch, J. and Hashemi, S. (2003). Is Microfinance an effective Strategy to reach the Millennium Development Goals. World Bank. Retrieved from: http://documents.worldbank.org/curated/en/982761468319745482/pdf/334540ENGLISH0rev0FocusNote124.pdf

Karlan, D., Goldberg.N (June 2011). Microfinance Evaluation Strategies: Notes on Methodology and Findings, The Handbook of Microfinance

Khandker, Shahidur, Microfinance and Poverty: Evidence Using Panel Data from Bangladesh, World Bank, Washington. (2003), and Fighting Poverty with Microcredit: Experience in Bangladesh, New York: Oxford University Press, Inc., (1998).

M. Claire Dale, Fiona Feng & Rhema Vaithianathan (2012). Microfinance in developed economies: A case study of the NILS programme in Australia and New Zealand, New Zealand Economic Papers, DOI:10.1080/00779954.2012.687543

Mayoux, L. (2001). Tackling the Down Side: Social Capital, Women’s Empowerment and Micro Finance in Cameroon. Development & Change, 32(3).

Ministry of Consumer Affairs (2011). Financial Summit 2011 – Access to Affordable Credit / Social and Community Lending Breakout Group. Wellington: Ministry of Consumer Affairs. Retrieved from: http://www.consumeraffairs.govt.nz/pdf-library/Access-to-Affordable-Credit- Social-and-Community-Lending-Breakout-Group.pdf.

Ministry for Women (2016). Annual Report for the year ended 30 June 2016.

Retrieved from: http://women.govt.nz/work-skills/paid-and-unpaid-work/labour-force-participation

Otero, M. (1999). Bringing Development Back into Microfinance. Journal of Microfinance, Vol. 1, No. 1, 8-19.

Pitt, M. M., Khandker, S. R., & Cartwright, J. (2006). Empowering Women with Micro Finance: evidence from Bangladesh. Economic Development and Cultural Change.

Mallet, R. (2012). The benefits and challenges of using systematic reviews in international development research. Retrieved from: http://www.tandfonline.com/doi/abs/10.1080/19439342.2012.711342

Ruthven O. (2001). Money Mosaics: Financial Choice and Strategy in a West Delhi Squatter Settlement.

Sebstad, and Monique Cohen. (2001). “Microfinance Risk Management and Poverty”, CGAP, Washington, USA.

Torre, M. L., & Vento, G. (2006). Microfinance. New York: Palgrave Macmillan.

Worral, A. (2017). Unemployment: Bad News NZ, It’s Much Worse Than You Think. Retrieved from:

Wright, G.A.N. (2000). Microfinance Systems, Designing Quality Financial Services for the Poor, Zed Books Ltd., London and New York.

Draft Questionnaire

The project is based on Microfinance as a tool to empower unemployed/low income women in New Zealand.

This questionnaire is for research purposes only and is strictly confidential. Details will not be shared in public unless express consent is given by participant.

Please tick the option below that best describes you!

1. Select your age group:

26-35

36-45

46 – 55

older than 55

2. Gender:

Male

Female

3. Highest Level of Education Achieved:

Secondary School

High School

College (Diploma, Bachelors)

University (Masters, PhD)

Other (please specify)

4. Current Working Status:

Student

Working in Public Sector

Working in Private Sector

Self Employed

Not Currently Working

5. How long has it been that you are with current working status?

Less than 2 years

2-5 years

More than 5 years

6. At the moment, you would consider your current income classified as:

Lower Class

Lower Middle Class

Upper Middle Class

Upper Class

7. Nationality: _________________________________

8. In your opinion, how much you know about microfinance?

In detail

In brief (not clear)

No idea

9. Do you think that you might be interested in getting microfinance services (for example, small loans without presenting any collateral) in future?

Yes

No

10. In your mind to what extent do you think that microfinance institutes will have most direct positive impact on the following?

| Description | Most Direct Impact |

| Poverty | |

| Education | |

| Women Empowerment | |

| Health | |

| Other Social Welfare |

11. Do you think that microfinance services should be introduced and promoted in developed countries (e.g NZ, Australia, USA, UK)? Please explain the reason.

Yes

Yes

No

Please Explain Why?

12. Do you give express consent to share information to public if my research is published?

Yes

No

Appendix B : Interview Transcript

Is microfinance becoming popular in New Zealand?

The nature of the microfinance’s clients and their needs change in accordance with a country’s stage in the process of sustainable growth. Do you think that microfinance institutions should adapt their services to the needs of their client’s especially unemployed women or women from low income levels?

What are the main internal challenges microfinance is facing nowadays?

How can new technologies contribute to the development of microfinance?

Can microfinance institutions assure their donors that their investments contribute to poverty reduction?

How should be the approach from the banks in developed countries towards microfinance in developing countries?

Appendix C : Employment Rates for 2016

(Overview of Evidence Base per Study – Simple & Fixed Effect Weighted Means)

Associated estimates extracted for each microfinance-empowerment association is provided in table 1.

The following table 2 gives the most recent information on employment rates.

| Description | Female | Male |

| Labour force participation rate | 64.6% | 75.2% |

| Unemployment rate | 5.4% | 4.7% |

| Employment rate | 61.1% | 71.6% |

| Youth (aged 15 to 24 years) not in employment, education, or training (NEET) rate* | 12.3% | 8.5% |

| Not in the labour force (number) | 675,000 | 450,000 |

| Underutilisation rate | 15.6% | 10.1% |

Source: Household Labour Force Survey 2016

*These figures have not been annually adjusted.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "Equality"

Equality regards individuals having equal rights and status including access to the same goods and services giving them the same opportunities in life regardless of their heritage or beliefs.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: