Analysis of China's Foreign Direct Investments

Info: 57110 words (228 pages) Dissertation

Published: 26th Nov 2021

Tagged: International StudiesInvestment

Abstract

Many studies have focused their attention on the impact of the Foreign Direct Investments worldwide. Instead, I, through this thesis, would like to focus on the analysis of the Foreign Direct Investments in general, talking about their characteristics and the different types of them that exist, but especially I would like to focus on the importance that, especially in the last period they have had in the entire global economic context, and the role played in terms of FDI by China.

The work starts with the analysis of the FDI in terms of growth effects that they have had in the market and the more various forms that the capital movements there has been across the countries. The FDI in fact, plays an important role in the development of the international trade and in the building of long-run and direct contacts between the countries, in a world that is always more interconnected and that is always more global and for this reason the relations and the contacts with the other states are fundamental. In the first part, I show that the FDI determinants

Table of contents

Click to expand Table of Contents

Chapter 1. The Foreign Direct Investment

1.1 The definition of Foreign Direct Investment

1.2 Types of FDI: Inward and Outward, Horizontal and Vertical FDI

1.3 The major FDI theories and the eclectic paradigm of Dunning and the VRIO framework

1.4 Political ideology toward FDI

1.5 Forms of FDI

1.5.1 Join Venture enterprise

1.5.2 M&A (Mergers and Acquisitions) and Greenfield Ventures

1.5.3 Wholly owned subsidiaries

1.5.4 Exporting

1.5.5 Licensing and the power of the Intellectual Property Rights

1.5.6 Franchising

1.5.7 Turnkey Project

1.5.8 Strategic Alliances

Chapter 2. Role of FDI for development of an economy

2.1 The global context: economic policies and new technology and the global supply chain theory

2.2 The advantages and disadvantages of the FDI

2.3 Foreign direct investment and international trade like as inseparable binomial and the importance of MNEs

2.4 FDI promotes the changing market structure and the integration in the global economy, enhancing the technology

2.5 Factors of attraction of the FDI in the new economy and the key role of job creation

2.6 The competitive policy as an element determining the investment in the international markets

Chapter 3. China as destination

3.1 Chinese conditions

3.1.1 Political environment

3.1.2 Economic environment

3.1.3 Social/Cultural environment

3.1.4 Technological environment

3.1.5 Legal environment and the fiscal incentives for the FDI

3.2 The development path and the political attractions of the FDI

3.2.1 Experimental stage: towards liberalization

3.2.2 Stage of gradual development

3.2.3 Stage of developing rapidly

3.2.4 The stage of consolidation and improvement

3.2.5 Views on the development of the FDI in the twelfth five-year plan

3.3 The destination of the FDI and the incentives in the related sectors

3.3.1 The main countries of origin of FDI

3.3.2 Sector distribution of the FDI

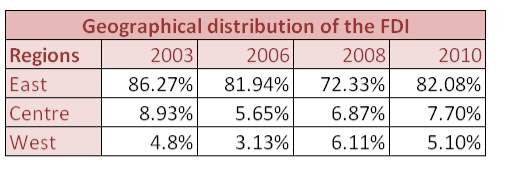

3.3.3 Geographical distribution of the FDI

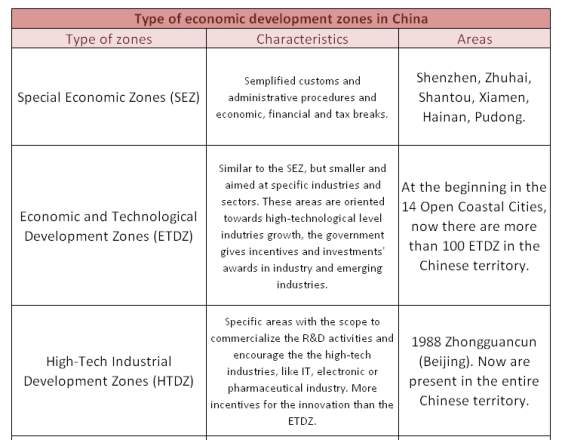

3.4 The classification of the economic development zones and the principal interesting zones

3.5 The historical development of the Special Economic Zones (SEZ)

3.5.1 Exploration phase

3.5.2 Expansion phase

3.5.3 Constant Growth

Chapter 4. China as investor

4.1 The transition from a destination of the other investors to a principal investor abroad

4.2 The Chinese economic growth and its go out policy

4.3 New normal

4.4 The Chinese shopping in Europe, especially in Italy, and in Africa

4.4.1 The Chinese investments, the case of the United Kingdom, of Polish and of Hawuei

4.4.2 Chinese investments in Italy, in Switzerland and in Africa

Conclusion: The future predictions

References

Chapter 1. The Foreign Direct Investment

1.1 The definition of FDI

Nowadays we live in a world that is always more characterized by the concept of globalization, a world that does not know boundary, a world that, many scholars define like as integrated, where differences between people or goods do not still exist. Exactly regarding this latter consideration, it is fundamental to talk about the central role that the Foreign Direct Investment and the Multinational Enterprises are having in the current period.

At this time the debate about the MNEs and the FDI is still very heated between many economists and also the definitions about these concepts are really different and varies, with a literature that covers both theoretical and empirical studies. Nevertheless the topic is really important and current, “their scientific analysis constitutes a young discipline, in fact most studies begun in the 1960s when the FDI was experiencing an enormous growth, which attracted economists’ attention”[1].

Before talking about the Foreign Direct Investment, it is fundamental to give the definition of Multinational Enterprise, considering that we are operating in a global world. “The multinational enterprise is a firm that controls and manages establishments located in at least two countries. More precisely: MNEs are firms that own a significant equity share of another company or operating in a foreign country”[2]. Through this definition, it is easier to understand the concept of FDI and how this mechanism has been used, since in the past, by the firms to become international and to increase their profit, creating an integrated world and exploited the strengths of the different countries, facilitating their growth, reducing their costs and increasing their efficiency.

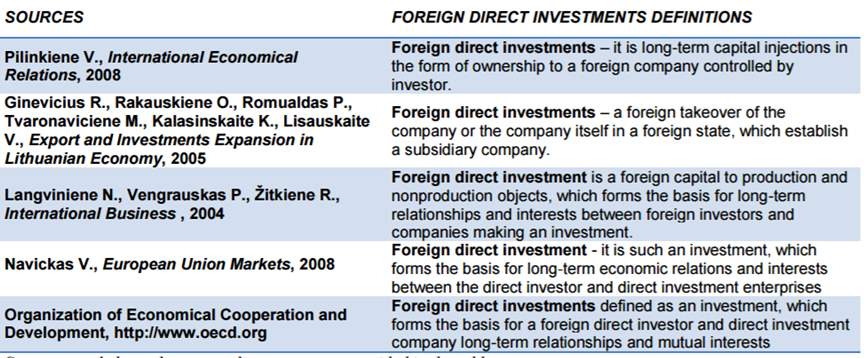

The definitions of FDI are varies and different such as possible to read in the table below:

In addition to the definitions above I would like to add other definitions that I consider useful in order to better understand the FDI and their evolution in the world economy. “The Foreign Direct Investment is an investment in a foreign company where the foreign investor owns at least 10% of the ordinary shares, undertaken with the objective of establishing a lasting interest in the country, a long-term relationship and a significant influence on the management of the firm”[3].

Foreign Direct Investments are, in fact, distinguished from “portfolio investments in which an investor merely purchase equities of foreign-based companies”[4], FDI implies a direct or lasting interest in, and control of, an enterprise (Loungani & Razin, 2001).

The International Monetary Fund’s Balance of Payments Manual defines FDI as “an investment that is made to acquire a lasting interest in an enterprise operating in an economy other than that of the investor, the investor’s purpose being to have an effective voice in the management of the enterprise”. (Imad A. Moosa-2002-p1).

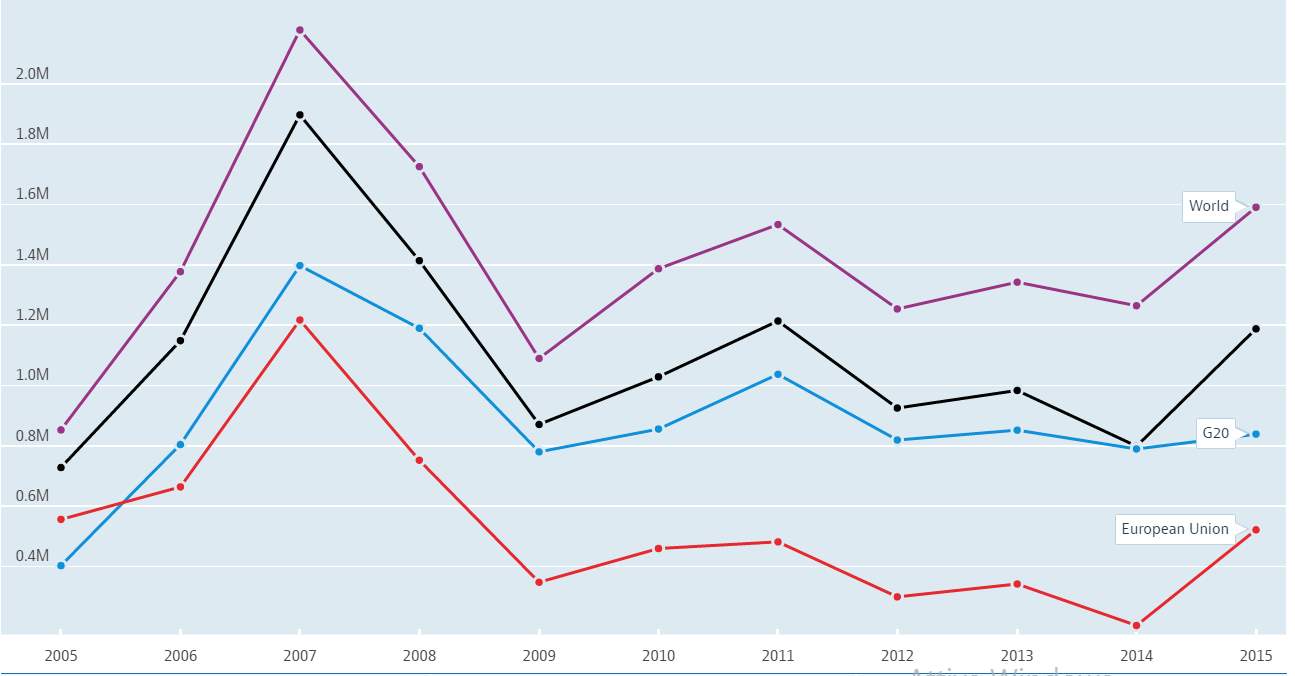

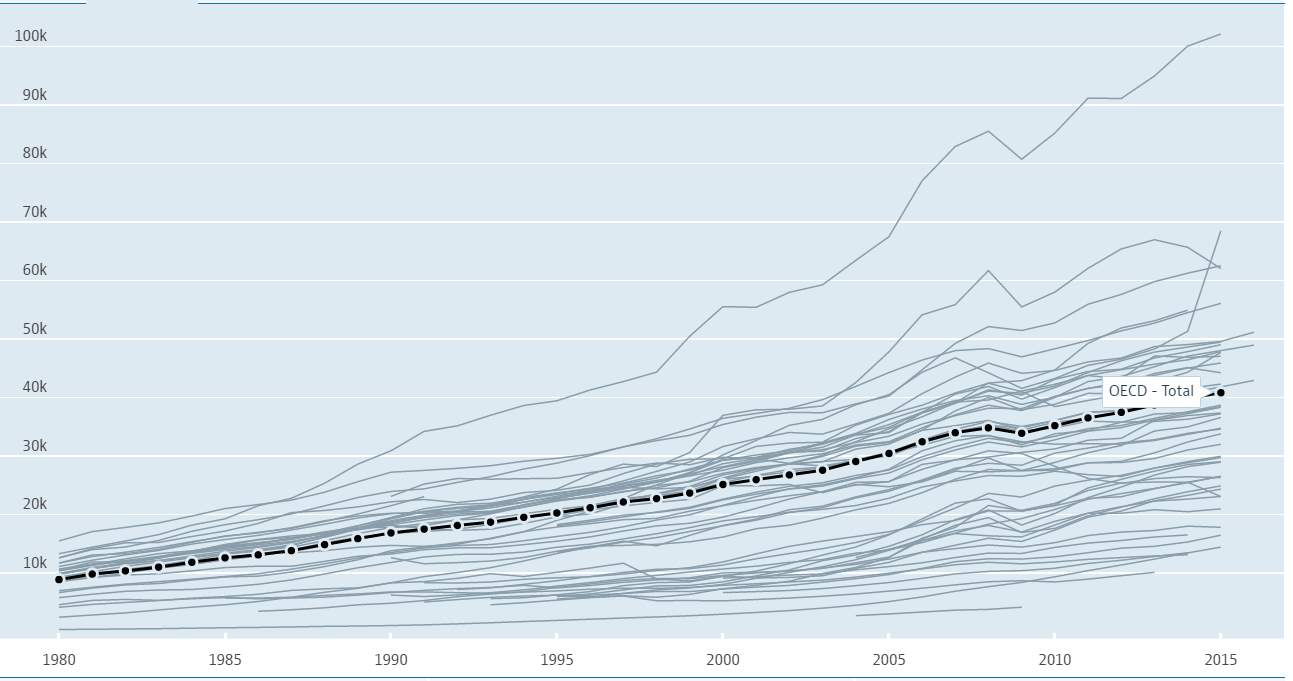

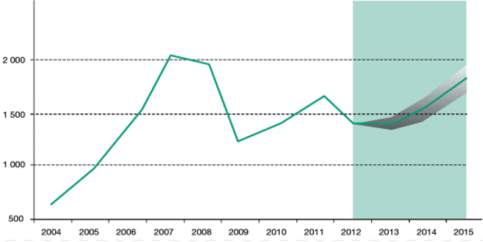

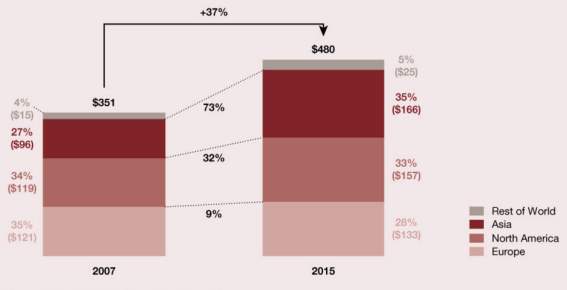

Another definition is present on the website of the United Nations Conference on Trade and Development, where the Organization for Economic Cooperation and Development (OECD) states “Foreign direct investment (FDI) is a key element in this rapidly evolving international economic integration, also referred to as globalisation. FDI provides a means for creating direct, stable and long-lasting links between economies. Under the right policy environment, it can serve as an important vehicle for local enterprise development, and it may also help improve the competitive position of both the recipient (“host”) and the investing (“home”) economy. In particular, FDI encourages the transfer of technology and know-how between economies. It also provides an opportunity for the host economy to promote its products more widely in international markets. FDI, in addition to its positive effect on the development of international trade, is an important source of capital for a range of host and home economies”[5]. According to this latter concept that it is possible to note how the importance of the FDI has grown in the last period (Figure 1) and also the related GDP (Figure 2) in the countries that have collected the benefit of this mechanism or that have operated investing abroad. How it is possible to see in the charts below the only moment of default was recorded in the 2008 due to economic crisis.

(Figure 1[6])

(Figure 2[7])

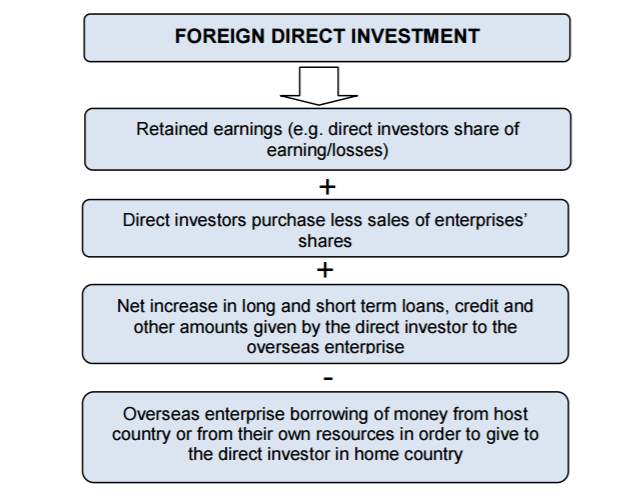

At the end, it is fundamental to highlight that the FDI is not just linked to the initial investment made by a firm in a foreign country, but also all transactions which follow one another between the investor and the investment company. Organization of Economical Cooperation and Development gives a model about the FDI calculation in the graph below, demonstrating that the total benefit of the investment is given by different elements, the sum between the first three minus the last one. The first element is formed by the retained earnings directly connected with the investment, the second one by the less purchases that the investor has to sustain, the third by the increase in the long-term and short-term loans or credit that the investor gives to the enterprise and the last one by the capital that the foreign enterprise borrowed by the investor:

Procedure for calculating FDI flows

Sources: OECD

1.2 Types of FDI

FDI can be distinguished by two different perspectives: host and home countries, through two diverse perspectives: the Direction and the Target.

Regarding the direction the definitions are between the Inward FDI and the Outward FDI.

The inward FDI regards the perspective of hosting country, when a foreign owned company buys a national company or opens a new affiliate in the host country.

The outward FDI regards, instead, the perspective of the home country and occurs when a domestic firms acquires a foreign firm or opens a new affiliate in the foreign country.

According the definition of the United Nations the “FDI net inflows are the value of inward direct investment made by non-resident investors in the reporting economy, including reinvested earnings and intra-company loans, net of repatriation of capital and repayment of loans”, while the “FDI net outflows are the value of outward direct investment made by the residents of the reporting economy to external economies, including reinvested earnings and intra-company loans, net of receipts from the repatriation of capital and repayment of loans”[8].

Both the inward and the outward FDI have positive and negative effects.

The inward FDI is encouraged by the tax breaks, low interest loans and subsidiaries, in addition the long-term gain is stronger than the short-term loss. The disadvantages are linked, instead, by ownership limits and different level of performance required.

The outward FDI is encouraged by the incentives given by the government to cover the risks, but the restrictions regard the subsidiaries given to local business rather than to international one and for tax incentives or disincentives for firms that invest abroad.

A striking example of inward and outward FDI is that of Coke that opened a subsidiaries in Italy. From the Italian point of view this is an inward investment while from the American perspective this is an outward point of view.

Analyzing the FDI from the target definition, it is fundamental to distinguish the horizontal FDI from the vertical FDI. The first one occurs when a firm invests abroad in the same industry, with the same activities in which it works in house. An example is Toyota because its production system is based on the owned assembly plants, obtaining the necessary components by external suppliers. This mechanism is in contrast with the option to produce the good domestically and then export it to the foreign country, if this could be convenient on one side because in this way the firm exploit plant-level economies of scale in its domestic plant, on the other side the Horizontal FDI is convenient because in this way the firm can save trade costs, principally costs linked to transport and tariffs though adapt to local tastes and local laws or culture is more difficult. This is known as the proximity-concentration hypothesis to whom Lael Brainard in the 1997 found strong evidence. The horizontal FDI are seen as Geographical extension. Many economists refer to this concept as Internationalization, and this foreign expansion can create profit because it is a source of competitive advantage, thanks to exploitation of new strengths. In addition this should be a strategy in order to exploit the current competitive advantage, exploiting the current strengths in a new market or seeking new competitive advantage with new strengths in new market. The benefits of this strategy are many, first of all on the demand side the transactional benefits with the market, natural resources and low-cost seeking, in addition the arbitrage opportunity that can arise, with regard the collection of financial resources and the possibility to exploit the more favourable institutional framework and fiscal burdens, and at the end the possibility to use the competitive leverage in terms of risk reduction, new knowledge bases or communication strategies. This strategy is useful in order to operate, in new market, exploiting the better transportation costs and transport conditions, in order to continue to sell the product that in the current market has achieved the maturity phase and in order to exploit the band-wagon effect and exchange the threat, if we consider that the foreign companies can entry in the national market and capture part of our consumers.

Regarding the vertical FDI, it occurs when a firm invests abroad in a different industry and with different activities in which it operates in the home country, the different industries are usually positioned upstream or downstream from the domestic industry. Sometimes we talk about vertical MNEs separated geographically according to economic convenience of different stage of production. This mechanism, in fact, is based on the search for low-cost inputs and the possibility to sell their output to their subsidiaries “through intra-firm export”[9]. The concept of intra-firm export cannot be overlooked because, especially in the current period, it characterizes a part always bigger of international trade.

The vertical FDI is associated with the concept of Vertical Integration or better with the choice between Make or Buy. In fact, the vertical FDI concerns the boundaries that the company choices to have, this is linked to the choice regarding the activities that a firm wants to produce on its own with respect to those that it decides to purchase from the market.

The comparison is between the market and so the price mechanism rather than the hierarchy and so the administrative mechanism. The choice is made according to what in economic language is known as Transaction cost. Coase, in the 1937, defined these costs as the non operation costs of the market price mechanism, but the costs that occur when there is an economic exchange in the market and that characterizes the transaction before, during and after itself. The transaction costs are determined by the actors involved that are characterized by limited rationality and opportunistic behaviour, being human, by the resources involved that are specific and rare and by the goods or services exchanged, elements characterized by high degree of uncertainty and volatile frequency.

These kind of costs concern the research and selection for choosing the best transaction, the renegotiation and monitoring costs during the transaction itself and at the end the costs linked to the management of the transaction consequences and the related control, in this latter step it is useful to mention the opportunity and agency costs. The vertical integration is characterized by four dimensions: degree, width, direction and extension. Regarding the degree, it concerns the involvement of the company for each input important for the final production, and this involvement can be total, where the firm own 100 percent of activities that formed the value chain or near, where the company does not own all activities necessary for the final goods.

In addition, many economists talked about the conic integration, when a firm depends in part from external source, quasi integration, when a firm creates a long-term relationships, having in this way control on the partners, but not being integrated and No or DE-integration, when a firm uses only the market for the entire needs, the advanced form of this strategy is the offshoring. The width is, instead, the degree of dependence of the company from his own sources, while the extension regards the length of the activities made in house. This strategy can create many problems with regard the increasing bargaining power of the buyers and suppliers when they become necessary in order to obtain the inputs or outputs necessary for the production, the risk of diffusion and especially the risk of quality erosion because the processes to control are many and the complexity increases and, at the end, the strategic risk in missing material. The best choice should be a fair compromise in order to produce part of the inputs in house and externalize certain activities to external companies, activity that is known as outsourcing.

At the end, it is useful to note how the benefits of the vertical integration are high. I would like to mention the cost reduction because the company exploits the economies of scale and the scope economies and eliminate the transaction costs, in addition it defends the market power, eliminating the risks to transfer know-how, but having in this way exclusive rights and quality control, with the possibility to apply successful differentiation strategy and attack forward and backward the business.

Nevertheless also the disadvantages are high. The costs increase because the control is bigger and also the level of investments, the flexibility will be lost and this implies less diversification and high exit barriers, necessity to maintain a determined level of balance between the differences activities in order to not spent useless time and at the end the managerial problems for the higher heterogeneity and complexity of the structure. At the end it is possible to say that the choice between make or buy depends by the following formula: Cp + Ca >

An example of vertical FDI is Intel, that has located the skilled-labour-intensive part of production process in developed countries while the unskilled-labour intensive part in developing one, but everything is fully owned by its. In this case it is fundamental, before taking this decision, to valuate the average cost at which the firm wants to produce the good and especially the activities of the entire value chain that it wants to make rather than to acquire from the market. One option should be to produce all activities domestically while the other one could be to invest in vertical FDI and produce part of the activities abroad. In the former case the firm could save a lot trade costs that otherwise occur, but in the latter case the firm could exploit cross-country differences in factor price.

This is possible exploiting the skilled-labour-intensive activities in skilled-labour-abundant countries, where the related price will be of course lower, and unskilled-labour-intensive activities in unskilled-labour-abundant countries, because also in this case, being the supply large, the price will be low. Regarding the vertical FDI the importance of the economies of scale is less than in the horizontal one, because in this case occurs the concept of outsourcing. In fact, in this case the trade-off concerns the trade costs and the possible reduction in production costs.

1.3 The major FDI theories and the eclectic paradigm of Dunning

Like it is possible to note above, different authors give different definitions of FDI and this has characterized the entire economy since their birth in the world. Birth that was before the 1960s, in fact, “Baldwin and Martin (1999) describe two waves of globalisation which are related to a rise in FDI flows. The first in the period between the 1820 and the 1914 and was characterized by North to South FDI in primary product sectors and railroads, while the second started in the 1960s and still continues nowadays, this latter wave is more concentrated on the developed nations with a focus on manufacturing, services and outsourcing”[10].

The first definition about the FDI, it is linked to Perfect Competition Approaches in 1960s, when the FDI was considered like a capital movement across countries and the model aligned with the Neoclassical Trade Theory. Through this view, Mundell (1957) and MacDougall (1960) predicted that the flow of FDI was directed from the countries with abundant capital to poor counties.

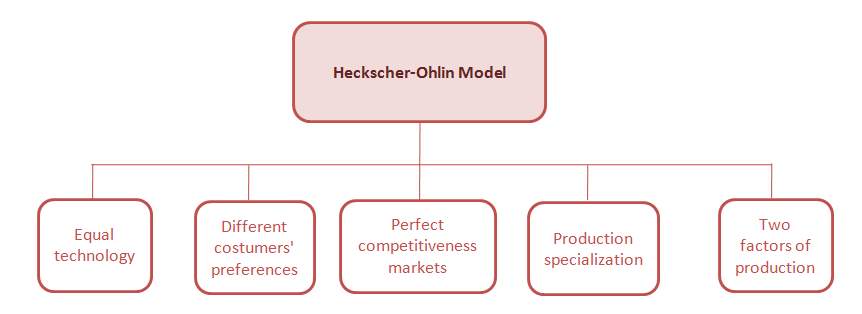

Mundell tried to explain this concept through the model of Heckscher-Ohlin (2x2x2)[11], taking in consideration two sectors, two countries (foreign and home) and two factors (labour and capital). He was able to demonstrate that a capital inflow does not influence the product and factor prices, and so “the factor price equalisation theorem does not hold, unless factor endowments differences between two countries are extreme”[12].

This occurs because the countries with a high amount of capital produce and export capital-intensive goods, especially in countries where there are not goods and in this way the country-producer can obtain a benefit because the return on capital will be much higher, while on labour much lower and this continues until prices will become exactly the same (Feath 2009). The important element of this model is that the firm can have advantage because it has to operate using the abundant resources that it has available.

As it is possible to note below, this model is based on five assumptions. The first assumption is based on the same technology to which all producers have to have access, in this way should be possible to eliminate the costs advantages. The different customers’ preferences and tastes are, instead, not taken in consideration. The same Pilinkiene said that the trade relationships are more frequent and useful when among countries there is similar history, development level and similar economies.

The third assumption is based on the concept that the firms have to operate in a condition of perfect competition, in this way nobody has the possibility to influence the price of the goods or services, but they have to purchase accepting the price imposed by the market itself. In the reality this kind of market does not exist. According to the forth assumption the goods become always more specialized, while the last one is based just on the two factors of production. This model is also more aligned with the theory of Feith (2009) who said that companies belonged to the richer countries and having stronger currency and subsequently lower fluctuation, used to borrow money from countries that have lower power especially from the currency point of view, this because the interest rate is low and the related risk too.

Basic Heckscher-Ohlin Model Assumption

Source made by author according Pilinkiene (2008)

Through this model Mundell demonstrated also that the capital inflow automatically reduced imports, this implies that the “trade in factors is a substitute for trade in goods”. According to this model MacDougall demonstrated a positive effect of the FDI in receiving economy, telling that this mechanism was able to increase the labour productivity and consequently the welfare of the country. This theory was linked to a consideration of investment responding “to differences in the expected rates of return on capital”[13]. According to this model, it is really hard to calculate the rate of return, especially if we consider that the attention of the MNEs is focused on the accounting side rather than economic criteria. This implies, for example, that they make transaction and use the differences in price only to obtain profit by the differences in term of tax environment.

Between the 1960s and the 1970s, other economists created “the portfolio theory”, after studying the relationship between the FDI and the rate of return, adding a third element that was defined as risk. Through this model they linked the concept of FDI to a concept of portfolio composed by stocks or bonds. In fact, they considered that only through a perfect diversification that should be possible to reduce the risk, in this way they were going to extent the vision of FDI from capital movement to movements of firms.

Another variant to the model of Heckscher-Ohlin, was the model of Feenstra and Hanson (1996), model in which they focused on the concept of skilled and unskilled labour, the principal factor of production. In this way they considered that the MNEs transferred capital from North to South in order to open new plants, but this mechanism weighed on wages, that were always higher for skilled labour and always lower for unskilled labour.

Considering about the major theories of FDI, it is important to talk about another movements, in 1970s, the Imperfect Competition Approaches. This approach focused a lot its attention on the MNEs, in fact, Hymer (1976) showed how considering the FDI as a capital movement, did not match with the activities of the big multinationals. He explained how was difficult for the MNEs to transfer their assets because of market imperfections. The principal types of problems are two: the advantages of the multinationals in comparison with firms without foreign activities and the transaction costs.

Regarding the advantages that the multinationals have in investing abroad, they are linked to particular incentives that the same government can give them or however the access to determined resources and information that, instead, do not characterized the local firms. These advantages compensate the negative elements, that on the other hand, regarded the MNEs, as ignorance of customers’ tastes or preferences or again the legal system or the business environment.

Transaction costs arise, instead, when the transactions are made on the market, as for example the necessity to purchase the intermediate product required for the final one, costs that if the product is produced entirely internally, do not occur, this happens because organise the transactions on the market is difficult and the costs do not depend by the producer.

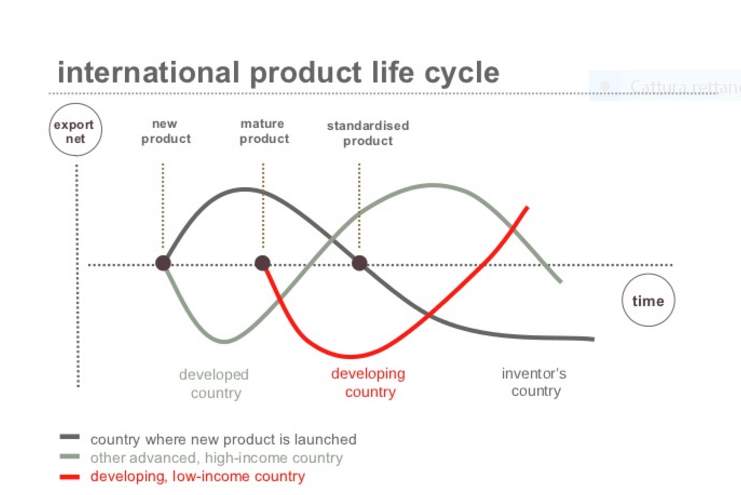

Another important theory about the FDI regards “The product-cycle theory” (Vernon 1966), the model arose after the World War II and it is useful in order to explain the growth of the American MNEs.

International product life-cycle

Based on Vernon, 1996 International investment and international trade in the product cycle. The Quarterly Journal of Economics.

Through this model the FDI are seen like an answer to the fair to lose market when the product achieves the stage of maturity and as mechanism of searching cheaper factor to face competition. According to this theory, during the first stage the product is innovative and it is sold in the country in which it is produced, usually in developed country because the technology is developed and it is easier to get consumers with higher income. In this way the producer tries to satisfy the local demand and at the same time to acquire notoriety and coordinate in efficiency way the three most important activities for a firm: research, development and production.

During the second stage the product could be exported, this implies that in this countries could arise some competitors, but in the third stage the home country could start to think about the possibility to open a subsidiaries both there and in less developed countries to exploit the cheaper resources as labour. The only positive reason of this mechanism is the major competitiveness that the firm can create in the market, enlarging its piece of market. Also this theory is not so simple to take in consideration, as the same Vernon said, because the market is evolving and because many firms could prefer the exportation rather than the FDI especially if we considered the developing countries where to find skilled employees is, of course, really hard (Hymer 1976).

According to this theory, it is necessary to say that in order to develop a new products or services into the market, it is necessary to have high amount of capital and technology and also qualified labour, all elements that characterized the rich countries. In the mature stage, it is possible to transfer the product to developing countries gaining advantage thanks to cheaper labour that characterizes them and the possibility to exploit the economies of scale. Thanks to this model, Pilinkiene said that it is possible to valuate when a product has to be produced in mother country and when it is more convenient to transfer the production abroad.

Vernon’s view focuses on the attention that the firms decide for the FDI in a particular stage of their products’ life cycle. This particular moment is exactly equal to the moment in which the “product standardization and the market saturation give rise to price competition and cost pressures”[14]. The only merit of Vernon is that he explained how the firms could invest in foreign countries and, especially in this case we talk about the developing ones, only in the moment in which the demand is enough large to support local production, and at the same time this is an useful element because takes the firm to invest in low-costs countries exactly in the moment in which the pressures becomes heavy.

The problem, of this model, is that it, completely, ignores the possibility to export or to license, simply focusing on the concept that when the foreign market is large and can sustain the local production, the firms must operate through the FDI. It is really useful to note how this model is more connected with the model of the industry life cycle that will be, exactly, the supply-side equivalent of the product life cycle. This model gives rise to S-shaped growth curve with four stages: introduction, growth, maturity and decline.

The first one is characterized with low sales and market penetration because the products are unknown and customers are few, but at the same time risk-tolerant and innovation-oriented, this explains the reason why the products are developed in the developed countries, there where the consumers have the possibility to spend part of their income for a product that is not perfect and for which they do not know the efficiency and efficacy.

In addition the driver of the industry life cycle is the Knowledge and this gives the possibility to understand why a product necessary has to born in a developed country, where “over the course of the life, consumers become increasingly informed”[15]. The growth stage is based on increasing efficiency and market penetration, thanks to technical improvement, and this implies more notoriety and larger piece of market.

The maturity stage comes exactly after the market saturation that arises with the growth of the market share, this stage implies that the consumers are ready for replacement, this means that the producers should they wish to continue to earn on that products, should invest abroad. This is exactly what Vernon had explained through his model. He did not want to avoid the decline stage, a period in which the new technology creates superior substitute products, and where a competition becomes a really price wars, from which you should flee focusing on differentiation, even if because this is impossible, but he wanted only to permit to the producers to exploit as much as possible the profit linked to their investment also if this implies to invest abroad and at the same time to be forecast in the home country and answer to new needs of their consumers.

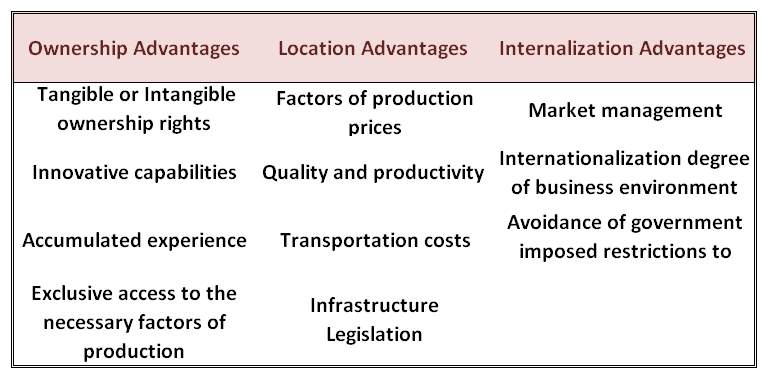

Before talking about the modern theory of the FDI, it is fundamental to give attention to the work of Dunning, what is known as eclectic paradigm. He started with the importance to talk about MNEs before focusing on the FDI, and so for firms become Multinational enterprises is possible only through three conditions: “Ownership, Location and Internalisation” (Brouthe et al., 1999)[16].

This model explains that the firms use the FDI in order to enter into the foreign market, but Dunning, through his theory, wants to demonstrate also why products can be produced and sold into foreign market. This method stresses not only concept as elements that affect the demand and prices, but also elements as risk, market size and especially the three advantages that it is possible to note in the table below.

Source made by author, according Dunning and Lundan (2008)

FDI advantages according eclectic theory

The ownership advantages are based on the “power” that the firm could have in obtaining patent rights and so the following possibility to use the right alone exploiting as much as possible the monopoly power. The ownership rights could be tangible because linked to machines or plants that the firm has rather than intangible and so obtained in legal way. Other kind of ownership advantages are the innovative capabilities and this is stronger especially if we talk about the developed countries and their ability to work with the skilled employees especially the younger one that have a greater propensity towards the technology and the innovation.

Another important element is the accumulated experience, in fact, it is possible to note in many studies during the past how to do always the same activities reduce the time required and increase the efficiency of the product. In addition with the experience it is possible to avoid to make the same mistakes. The last benefit linked to the ownership is the possibility to have access to factors of production and so to build a competitive advantage on this factors that the other firms cannot have.

The location advantages is a concept linked to a possibility to exploit the FDI theory in order to enter and operate in a market where the conditions are favourable, considering different elements like: lower price for the primary factors of production, access to the secured domestic market because the firm knows the tastes and the preferences of its country better than the competitors, lower transportation costs or production costs, with high level of productivity and low level of risk and again favourable taxation policy.

This explains why the major part of the companies belonged to the developed countries have decided to transfer part of their production abroad, especially in country where the legislation and the costs of the labour is low.

Considering the internalization advantages, Dunning explained that for a firm should be more convenient to obtain benefit for the market management, but considering its ownership in the mother market rather than to sell license to other independent firms and consequently to risk to suffer the restrictions imposed by the government of the foreign countries.

At the end of this analysis Dunning wanted to highlight the difference between who uses the FDI in permanent way, being willing to get production effectiveness, and who is focused in one time investment, trying to capture as much market as possible through the natural and human capital, focusing on the location and internalization advantages. The same Dunning tries to test the theory through two hypothesises:

- First hypothesis: international competitiveness, companies obtain benefit thanks to a competitive advantage linked to a domestic production and ability to export;

- Second hypothesis: location advantage, based on a ratio between the amount exported and the local production, ratio known as form of involvement.

Dunning at the end of the test, made through the analysis of data related to American manufacturing companies, operating in seven countries, showed how, regarding the first hypothesis, market side had negative effect in comparison with skilled employees. Considering, instead, the second hypothesis, he discovered that the ratio export-import was negative respect of the ratio export-production. Finally, it is possible to say that the FDI depends on various elements like ownership advantages, infrastructures, property right, transportation costs, market size, government restrictions and so on.

The most important concepts “of the OLI paradigm have also been introduced in a dynamic framework known as the Investment Development Path (IDP)”[17], this concept is linked to inward and outward investment, elements of which I have discussed above. It is possible to say that the model of Dunning is considered a sort of summary of all FDI theory above explained because takes into account different and crucial determinants, considering also the concept of Horizontal and Vertical FDI.

Dunning, through his model, wanted to focus on the concept of the location-specific advantages. This concept means that the advantages arise in a moment in which the firm combines specific resources endowments or assets that are characterized of a specific location with its own unique assets, like technological or management capabilities, this is for Dunning more useful than to license or export. The only way to exploit the foreign resources is to undertake FDI. Penrose in the 1959 stated that “The firm is a collection of resources”, resources that can be divided into three categories: tangible, intangible and human.

The tangible ones are the financial and physical assets, for example we talk about the borrowing capacity or the internal funds generation or the plants, the raw material, the buildings and the land required for the production.

For intangible resources we refer to technology, reputation, knowledge and relations assets. The patents, the copyrights, the intellectual property rights or again the customer loyalty, the company reputation with the government or with the consumers or again with the suppliers and the brands belonged to this latter category of resources too.

At the end there are human resources characterized by training, loyalty of employees or adaptability and especially by experience. Through the VRIO framework, a manager can understand if it is possible to invest abroad focusing on their resources or not. In fact, this framework permits an analysis about the value, the rarity and the imitability of the resources and an analysis that regards the structure in terms of control mechanisms of the organization, in order to valuate if it fits with the ability of the employees, giving them the right incentive in order to exploit the resources.

The analysis of the value of the resources gives the possibility to understand if that resource permits to firm to increase its revenue and decrease the costs, exploiting an external opportunity. Regarding the rarity’s analysis, it is important because only if the resource is rare that the perfect competition has not set in and the firm can gain profit from its competitive advantage. At the end the analysis of the imitability gives a sort of time in which the firm can operate in terms of “monopoly” in the market because the competitors do not know the resources on which the firm base its competitive advantage and they do not have access to them.

This time will be longer of the competitive advantage is based on intangible resources because those are more difficult to be imitated thanks to legal forces too. The theory of Dunning and the VRIO framework explain why the developed countries have decided to undertake FDI in the oil sector, exploiting this location-specific resource with their valuable managerial capabilities and it is the same considering the cost of the human labour and the reason why the most famous brands have decided to invest abroad, in developing countries, brand as Nike for example.

Another important example regards Apple or Hewlett-Packard and Intel, the world’s major computer and semiconductor companies that are located in California at Silicon Valley. There, where, probably, according to the study of Dunning, there is a concentration of intellectual talent. This could arise by a sort of informal contacts that bring firms to have benefits from each other’s knowledge, many economists called this phenomenon like Externalities and many studies have demonstrated that many firms have obtained large benefit, locating their plants close to these sources.

Another demonstration of this useful mechanism is given by the investments that the same Europe and Japan have made in that place in order to wish to gain benefits and knowledge by these externalities.

1.4 Political Ideology toward FDI

Now, I would like to talk about the political ideology toward FDI, ideology that sees on one hand the completely hostility to all inward FDI for the host countries and on the other hand the idea of the free market economics. Between these two really opposite theories there is another approach that is known as pragmatic nationalism.

Before talking about this new approach, I would like to introduce what means the “radical view” and the “free market view”. With the first theory, many economists saw the MNEs like “an instrument of imperialist domination”[18], in fact according to this concept that the FDI are seen not just as an instrument of development, but as an instrument of domination. This because, the home countries invest abroad and try to obtain benefits and profits, bringing them to their countries, giving nothing in exchange to the host countries, but only exploiting them as much as possible.

This view was famous and frequent in the past especially if we consider the Easter Europe between the 1989 and the 1990 or many socialist countries in Africa or again nationalistic countries as Iran or India. At the end of the 1980s, it is necessary to underline that this concept saw its collapse thanks to three important historical reasons: the end of the Communism in Easter Europe; the economic performance that at the end of this historical moment characterized that countries and the volunteer to go out from this poor condition also encouraged by the growing belief that the FDI was an important source for technology and jobs, increasing the economic growth; the intensive growth that the countries that embraced the capitalism view, had.

The free market view is based on the concept of the comparative advantage. In fact, according to this concept that countries have to focus on the productions of goods and services for which they are more efficient and specialize, purchasing from the other countries the goods that they are not efficient to produce. According to this concept, the FDI should increase the efficiency of the entire economic world. Great Britain and the United States are the countries that more than the other undertake the FDI even if many restrictions from the government exists in terms of inward FDI, regarding for example the limits of 25 percent that the foreigners cannot outweigh in purchasing the U.S. airlines.

The intermediate approach is completely different from both the two theories discussed above. In fact, according to this concept, the FDI are seen as elements that have the positive and negative effects. Of course the FDI strategy is convenient only in the moment in which the benefits outweigh the costs for a country that undertake it, but it is also more important to underline that the benefits are however a lot also for the host country. An important example regards the possibility that, investing abroad, the developed country brings there capital, technology, skills, all elements that can give a contribution for the development of those poor countries.

Many countries are, however, concerned that the foreign firms can bring many components from its home country and this implies a negative answer for the host country’s balance of payments. Another important aspect of this approach is the tendency of the host country to give grant and tax benefit to foreign MNEs, this is exactly what is happening in Europe, in the countries that at all costs want to host the American investments or the Japanese FDI.

In a world always more global, many countries have adopted the free market policy, but not the free market view that is so radical and difficult to apply in the reality. Exactly for this reason that many countries are embracing the latter strategy, countries as Italy, Spain or Japan, but also countries that have recently liberalized the FDI as some countries of Latin America or China.

1.5 Forms of FDI

The MNEs decide to invest abroad in order to increase their profits. This kind of decision is linked to what in economy is defined as strategic decision and it is of course not easy and with a grade of risk so high. In fact, the companies arise for creating value for the society, for the organization and for the capital and product market and through this decision that they have to satisfy the shareholders and the stakeholders, gain profit and consequently grow.

Before deciding to entry in a market a company has to do what is defined like PESTEL analysis, an analysis that bring it to be sure about the industry in which it wants to entry and the possible profit that it can gain. This analysis is focused on the Government and Politics, the natural environment, the social structure, the technology, the national and international environment and the demographic and legal structure. After this analysis the company can decide through what form it wants to enter in new market. In the following paragraphs, I am going to explain the different possible way for entering.

1.5.1 Joint Venture enterprise

A joint venture is a separate business entity created by two or more other independent companies that have decided to share ownership, risks and returns and the entire governance of the new company that they create. To enter in a new market the most popular way could be the possibility to create a joint venture with the foreign firm. The most common way to create this kind of company is the 50/50 venture that implies that the two parties have the same risk, the same ownership stake and the same control on the new company through a team of managers. A famous example of Joint Venture is given by Fuji-Xerox that arise by Xerox and Fuji Photo in the form of 50/50 venture even if nowadays it is characterized by 25/75 venture with Fuji Photo holding 75 percent.

The main characteristics of the Joint Venture are: the number of the parties involved in this mechanism and the contribution that each part decides to give to new venture and the relative ownership that each part has. All other elements regard the post-deal, in terms of profit shaping for example, if this happen in proportion to equity ownership or not, the governance and the control, the structure that the parties decide for the new company and the relative Human Resources model and at the end the technology, the production and the entire value chain within which the parties want to operate and then create the Joint Venture.

The operation of the Joint Venture is based on the capital that each part gives to the new entity. So as all other forms with which the company could decide to enter in new market, also the Joint Venture has advantage and disadvantage. Regarding the advantages, first of all the firm that decides to invest through this mechanism can benefit from the local partner’s culture, language, knowledge, political and business system and especially the possibility to benefit from the reputation that the company already has in the market and the loyalty created with the local consumers.

Regarding this point the most important element regards the culture. In fact, for a company, in order to obtain notoriety in the market and increase its reputation among the consumers, it is necessary to know the local culture because this is the only way through which will be possible to meet the needs of the consumers and to obtain their trust. In addition, the culture is the only asset that is not possible to purchase through capital, but that should be achieved through the passage of time because it is necessary to endorse the local values and principles and this requires time and experiences, time that should be cut if the company decides to gain new market exploiting the knowledge and the experiences that the local firm already has.

Another important advantage is the substantial costs and risks that a company that decides to invest abroad, necessary, has to sustain. In the case in which it decides to invest through the possibility to create a Joint Venture, this ,of course, reduces the expenses required to open new plants and to purchase new machines and at the same time, this reduces the risk exposure for each individual company. The third and latter advantage concerns the case in which from the political view the only way through which it is possible to enter into determined market is the creation of Joint Venture. This occurs, because in many cases this mechanism reduces the interferences of the government, especially in countries where the nationalism is high. In this way the local partners can have positive influence on host-government policy.

Regarding the disadvantages, the first, that is fundamental to take in consideration, is that creating a Joint Venture the company risks to reduce its competitive advantage based on particular technology that during the time it had achieved. In fact, it has to share everything with the other part, sharing of course also the control of the technology or of particular know-how. It is fundamental also to say that Joint Venture agreements can be created minimizing this risk.

First of all the company can choose for a majority ownership and in this way it has more control and reduce the necessity to communicate everything to the other part and to give to it the control on all, but this of course is not the simply way, considering that to find a company that choose for the minority is not easy. A second disadvantage is based on the element that is difficult to find in the market a Joint Venture that gives a company the tight control over the other partner, having for example need to realize location economies or to increase its knowledge for operating alone after. This fair arises in the local companies of the host countries from the possibility that the foreign companies could want to do global market attacks against its rivals and for this exploit this strategy.

Another disadvantage is the shared ownership that can create battles among the parties or because they do not share the same vision and strategy through which to manage a company or because the goals of the investor can change during the time and this create conflict if it is not shared. Many studies have demonstrated that this conflicts are many especially because the ideas and the goals and especially the strategy that each part wants to apply are different and this is more intensive between parties of different countries and at the end this conflicts bring to the dissolution of the Joint Venture, with the ownership in the hand of the part that at that time has more bargaining power. During the time the foreign firm acquires always more knowledge about the local policy, culture and values and so will have always less need of the local part and this increases its power reducing those of the other part.

1.5.2 M&A (Mergers and Acquisitions) and Greenfield Ventures

Through the world merger and acquisition we refer to a concept in which the ownership of a company will be transferred or combined. Through this choice the company can grow or die or change the nature of its business and its competitive advantage. A merger arises when two or more companies combine creating a new entity. An acquisition, indeed, arises when one company decides to purchase another one and this does not create a new entity, this is frequent when a small firm will be absorbed by the parent organization.

The advantage of the M&A is that, first of all, the company can increase its competition, because the name of producer is known and because in this way it can reduce the expenses of the Research and Development activities and the costs linked to delivery costs. The disadvantage is not only to create job, but the jobless on the host country and this could remark the interferences of the host government.

Regarding the acquisition, it is a lot compared with the Greenfield Venture, in fact, in the following paragraph I would like to discuss about the differences and the advantages and the disadvantages of the two different mechanisms.

The first and most important advantage of the acquisition is the ability for a firm to acquire a local firm and entry directly into new market, the target one. This is important because in this way the company is able to cut the time and gain competition and profit. The second advantage is the pre-emption of the competitors especially if we talk about markets in which the globalization is high. This mechanism is important and efficient especially in markets where the deregulation and the liberalization are high and so consequently the possibility to enter through FDI. At the end the last advantage is that the managers consider the acquisition less risky than the Greenfield venture.

In fact, through the acquisitions the companies purchase something about which they already know the assets and the profit that they produce, especially purchase not only tangible assets but also intangible assets like local brands or knowledge about the local needs and tastes, elements that in the case of Greenfield venture are absolutely unknown and that can create a risk for a new company really high considering the ignorance of the local national culture. At the same time, the disadvantages of the acquisition are several.

First of all, sometimes the acquiring firms overpay in comparison with the amount of assets that they obtain in exchange, especially if more than one firm is interested in the company that is element of the transaction, the manager, in addition, is sometimes too optimistic and this brings him to pay a lot. This is known as hubris hypothesis, approach that states that the manager overestimate the company that they are going to purchase also because they overestimate their position in the company and their ability to create and generate value.

Many acquisitions fail because of the different culture between the acquired and acquiring firms. For example the employees cannot agree with the new manager and so change their work and this create in the acquiring firm a high level of turnover and this can create a loss of talent employees and consequently a loss in the economic performance of the company. Other failures can be linked to a volunteer from the managers to create synergies that do not occur because the differences also in terms of management philosophy can create a slow integration and many problems.

Many issues are, in addition, caused by a not careful pre-acquisition screening, without an attention analysis about the potential costs and benefits that could arise, the expectations can be high and unrealized. The most important way through which a company can reduce these failures are the necessity to create a plan of integration next the acquisition.

Regarding the Greenfield Venture, the biggest advantage is the possibility for a company to build in the foreign market the company that they want in terms of culture, knowledge, technology and values, this is easier than purchase an organization and after deciding to change it. As well as it is easier to establish determined activities in a new firm rather than to change the process of a company that already exists.

The problem is that Greenfield Ventures are difficult to establish for the time necessary and especially the costs and the risk exposure required. A high level of uncertainty linked to future revenue streams and profit characterized this forms of investment, a risk more than compensated by the possibility to face with unpleasant surprise, element that, indeed, characterizes the acquisition.

At the end it is possible to say that do not exist the best way to enter in the market, but that all depends. If the firm wants to enter in the market in which already exists a strong competition the acquisition will be the best solution, indeed, if a company wants to enter in a market in which there is not any incumbent competitors to be acquired, will be better to choice for a Greenfield Venture.

1.5.3 Wholly owned subsidiaries

In the wholly owned subsidiaries, the firm is the only owner of the stock. This investment can occur through two different ways: the first is similar to the Greenfield Venture, while the second gives the possibility to the company to acquire a local firm in the host nation, using it in order to promote its products. Also in this case there are many advantages and disadvantages.

The first advantage is the possibility to enter in a new market without losing any kind of control over the own competences, this is the best way for the high-tech companies. This mechanism gives, in addition, to a company the complete control over all operations in different host countries and this permits the global strategic coordination. This way is also important if a firm wants to realize experience curve and location economies.

Through this mechanism the national subsidiary can, for example, focus only on determined part of production, exchanging parts and products with other subsidiaries in the global production system with a central control on it, system that takes decision about how much they have to produce, how they have to produce and at which price the product will be sold. The problem of this investment is that it is the most expensive mechanism in order to serve new market, expensive not only from the capital point of view, but also considering the risk at which the firm will be exposed, considering that it does not have any knowledge about the country in which it is going to invest.

1.5.4 Exporting

At the beginning, many companies start their global expansion as exporters. Exporting implies to produce in the home country and only then to decide to export, selling the products abroad.

The advantages of the exporting are, first of all, the possibility to avoid the high costs necessary in order to open new establishments and plants in host country, second the firms will be able to achieve scale economies thanks to global sales volume and at the same time experience curve and location economies.

The first negative element is, indeed, that exporting from the home country forces the producers to sell at the price that in the foreign countries could be high in comparison with the local costs for the similar products and then companies focused on the standardization strategy rather than differentiation one.

From this perspective should be more convenient to produce where the mix of resources required is cheaper and then to export, but from that place and not form the mother country. Another disadvantage is that exporting can require high transportation costs especially for bulk products, for which should be more convenient to produce them regionally, because otherwise it does not give the possibility to gain from scale economies.

Another drawback is constituted by tariff barriers that can reduce the possibility to sell the products abroad because this increases the costs. The last disadvantage arises when the company decides to a local firm its marketing, sales or other services in order to promote its products, but this does not do the work in the same way as the firm would.

1.5.5 Licensing

To talk about this form of investment, it is fundamental to explain what is the intangible property, specifically, the intellectual property right. The European Directive 2004/48/EC states: “The protection of the intellectual property is important not only for promoting innovation and creativity. But also for developing employment and improving competitiveness”[19]. The power of the patents is really high because they permit to the company the possibility to operate in the market with a monopoly power thanks to a protection from the legal forces.

This power is linked to a possibility to have incentive to innovate, in fact in the current period there has been the “patent explosion” with an “analogously unprecedented explosion in the amount and quality of scientific and technological progress”[20]. According to this latter state, there are two hypothesis, on one hand who sustains that the increase of patents has been the cause of the acceleration of innovation, on the other hand, indeed, there is who states that the increase of patents has been the effect of the continued growth of innovation.

Regardless this difference, it is useful to note how the intellectual property has in the current economic market an importance always higher, and the licensing agreement is exactly linked to this element and specifically to the case in which the licensor grants the possibility to exploit this right to another entity for a determined period and in exchange the licensor receives a fee from the licensee.

The first advantage is linked to a possibility to entry in the foreign market without sustaining the costs and the risks required, in fact this form of investment is attractive for whom that has not enough capital to penetrate in new market or however when a firm is unwilling to engage much financial resources for a risky market that could be volatile. This form is convenient also when the foreign market is prohibited by many barriers. Another and last advantage is that the firm has lot properties, but it does not want to develop them alone and so it decides to grants the license to other firm or more than one.

Regarding the disadvantages, the first one is, of course, the fact that this form does not give the tight control on the entire process that is necessary if the firm wants to realize economies of scale and location economies and experience curve. In fact, through this mechanism the licensee has to set-up the production process in a centralized location and this can delay the development of the location economies and experience curve.

Another drawback is the impossibility to use the profit that a firm has to earn in a country against the attacks that the firm faces in another country and through the licensing method the coordinated strategy is really difficult to apply. The last problem linked to licensing is that when the firm grants the property right loses its tight control on its know-how and consequently it loses the principal part on which it bases its competitive advantage.

In fact, nevertheless many companies believe that also with the licensing agreement they are able to preserve their power, this is absolutely not true and possible. The useful way in order to reduce this risk is to enter in cross-licensing agreement with a foreign firm, through this agreement the licensor wants to obtain not only the royalty fees in exchange of his right, but also that the foreign firm grants part of its know-how, through this mechanism the companies are not interested into opportunistically behaviour because in a moment in which one of these violates the agreement, the other will do exactly the same. Another way for reducing this risk should be the possibility to create a Joint Venture through this know-how where the two parties have an important equity share, this is exactly what has happened in the case of Fuji-Xerox.

1.5.6 Franchising

Franchising is quite similar to licensing, but it involves long-term commitments. In this case the franchiser not only grants intangible assets, but he undertakes to comply with strict rules to franchisee. In addition the franchiser receives the payment of fees.

In terms of advantages the franchising is exactly similar to the licensing, in fact through this method the firm reduces the costs and the risks of opening in new market, building profitable process as quickly as possible. Regarding the drawbacks, they are less pronounced than in the licensing. In fact, in this case the firm has not interest in creating location economies or experience curve and neither interest in sustaining the attacks in one country with the profit achieved in another one.

The only one important disadvantage of the franchising could be the possibility to lose the quality control and consequently to damage the image of the brand. In order to solve this great problem the only way should be the possibility to create wholly owned subsidiaries in the foreign market or at least to create Joint Venture with local firms in order to preserve always a determined degree of control.

1.5.7 Turnkey projects

The turnkey projects are more common in determined sectors like pharmaceutical, or chemical one, and the reason is that through this method the contractor creates every detail of the entire project for a foreign client, considering also the training for the employees and after he sells this project. At the end the client will have the “key” of the entire project that is now ready to be used in the market. Exactly from this characteristic that arises the name of this method.

The advantages are many. First of all, the know-how, in the sectors in which this mechanism is used, is really high and gives the possibility to earn high economics returns, this incentives to entry into the market through this form of investment rather than through the FDI because the interferences from the government should be really hard. In addition, the local firm could want to exploit their resources, but do not have the necessary technology required and for this reason that they decide to purchase its through the turnkey project. Another advantage is linked to the case in which for a firm enters in an unstable environment from the economical and political point of view could be dangerous and risky, while exploiting this method it could reduce the risk.

Regarding the disadvantages, first of all the firm through the turnkey project demonstrates that has not long interest in the foreign country and this can create problem if during the time the country proves a good market for the entire process, so the possible solution should be the opportunity to maintain always an equity interest in the operation. In addition, a firm through this mechanism creates necessary a foreign competitor especially if we consider that the know-how sold through the turnkey project could be the dominant part on which the company has created its previous competitive advantage.

1.5.8 Strategic Alliances

Strategic alliances are seen as a sort of agreement between potential and actual competitors. This contract is based on two or more firms that have equity stakes, but for short-term, in order to operate on a particular project.

The first advantage concerns the easy to entry in a new market especially through the collaboration with local foreign firm.

In addition, this kind of collaboration helps the firm to share costs and risks linked to a new and great investment in developing new product.

The third advantage is the possibility to create synergies thanks to complementary assets of each, synergy and skills that neither firm is able to develop alone, at the end this could be an optimal mechanism through which the firm creates technological standards from which the firm itself will benefit.

At the same time many economists say that this method gives to “competitors a low-cost route to new technology and market”[21], exactly what happened between Japan and United State. The problem of the strategic alliances, is also that many companies can give more than what they receive. In fact, according to an economic study, it is demonstrated that a lot of alliances fail within two years of their formation.

In order to avoid these frequent failures, it is fundamental to do careful screening about the partners, in fact a good partner has to share the same goals and has to help the company in order to achieve these goals, sharing the costs and the risks. In addition, the partners has to have capabilities that the other part lacks in order to create synergies and exploit them and not have opportunistically behaviour, but create a familiar environment.

After a selection, it is fundamental to create the alliance structure, in the way that each part knows its rights and its risks and there is not the opportunistic risk also because the parties have to extracts in advance the know-how that each of these has to share. At the end, it is fundament to manage the alliance, having sensitivity to cultural differences and trying to maximize the benefits, stressing the concept of relational capital that is one of the most important point that helps to create trust and respect among the parties.

Chapter 2. Role of FDI for development of an economy

2.1 The global context: economic policies and new technology and the global supply chain theory

The Foreign Direct Investment has an important role in the entire world economy, in fact, it can reduce in the indirect and direct way the poverty that still exists in several countries. Through this mechanism, it is, also, possible to change the direction of welfare and capital flows. In fact, it is known that for reducing the poverty in some developing countries, it is possible to increase the employment and consequently the income of the employees that can, in this way, spend money and so to rise the entire country’s welfare.

If this latter tool should be considered as the direct element through which to reduce the poverty, the indirect one should be the necessity to increase the capital technology, to change the market structure, if necessary, and especially to increase the integration in the entire world context and consequently to operate and to trade with the other countries.

In order to discuss about the topic above stated, I think that is fundamental to introduce the concept of globalization, so as to understand the context in which we live.

Currently we are living in a world that is always more globalized, where do not exist boundaries, but where each country is more interconnected and integrated with the other one. In fact, “Globalization refers to the shift toward a more integrated and interdependent world economy”[22]. The concept globalization involves not only the globalization of the markets, but also and especially the globalization of the products.

The globalization of the markets is connected to the new trend that has fused the historically distinct national markets into one huge global one. This element characterized the company that have to offer the same basic product worldwide in order to create a global market, but the element that still characterizes the current market, is that the companies do not have the characteristic to be multinational giants and consequently do not benefit at all from the globalization market. In addition, significant differences among all countries still exist, along consumer preferences or distribution channel or again legal system and business regulation as well as the most important one that is the cultural and value system.

The globalization of the products, instead, refers to the place in which it is more convenient to purchase or to produce determined intermediate products, where this convenience is linked to cheaper cost and high quality. In this way the companies can offer their product in the market in more efficient way and consequently they can increase their competitiveness.

We are talking about what is defined as international economics and it is important to highlight how that braches is exactly the same of the national one because the purpose of this behaviour is the internal or international transactions in order to reap the benefits.

It is fundamental to underline a difference between the pre-globalized world and the current world. In fact, if during the past, each country produced exactly the amount of products that it was able to consume, now the condition is really different because the countries produce not only what they can consume, but also an amount of goods and especially services that they can offer abroad and export or however produce directly abroad.

This element is possible thanks to industrial revolution and especially in the 21st century, thanks to technological revolution, a revolution that has increased the communication and the possibility to transport a large amount of goods with a really few capital. In addition, the ICT revolution made possible to coordinate the complex production at distance because it facilitate the control, reducing the costs and the risks linked with the combination between the technology of more advanced countries and the labour of poor countries.

This combination was possible thanks to the wage differences between the developing and the developed nations. This trend characterized the world in the 19th the century, when there was a sort of converge between the North, formed by industrialized countries, and the South, formed by de-industrialized one, instead if we consider the 21st century, it is useful to note how there has been a converge between the North and the South and this has bring a de-industrialization for the North and a rapid industrialization for the South that has created an excellent performance along several countries, especially considering China.

What characterizes the 21st century, are different elements. First of all the international investment, but in sectors as training, technology, focusing on the long-term business relationships, secondly the cross-border know-how like intellectual property right and tacit form of know-how that can be transmitted only with the direct work abroad, and lastly the development of the infrastructure that has helped to coordinated the production worldwide. In order to talk about the global value chain and the global supply chain, it is important to talk about nations that have developed a deep industrial base in order to become competitive, we refer to these countries as emerging ones.

In fact, in order to talk about the globalization, it is more important to outline that the value chain and the supply chain have assumed an important role in the economic context, involving all countries, from the richer to the less advanced one. The trade and the investment openness, in fact, are the principal components of the policy reforms in G20 countries, where the purpose is to implement an effective framework for sustainable, strong and balanced growth in order to bring all countries to reap benefits.

In fact, I would like to talk about the global value chain and to try to understand who, in terms of country, is able to catch the benefit from that behaviour. Richard Baldwin talks, instead, about the global supply chain and how it has changed the world, creating a rapid growth due “in part to its impact and in part to rapid technological innovations in communication technology, computer integrated manufacturing and 3D printing”.

The concept supply chain is referred to a series of plants necessary in order to obtain the outputs, while the value chain is popularized since the past by Michael Porter as a broader concept. Porter, in fact, said that the companies spent a lot of their time to produce inputs or intermediate goods for which they had not competitive advantage. He focused a lot on the Ricardian principle of comparative advantage and so to produce what you are able to produce in order to reduce the costs and increase the profitability and for which you have abundant inputs at lower costs and consequently to purchase from abroad the products for which your costs are high and competitiveness low. This requires a careful analysis of supply chain that according to Baldwin, have to be divided into “four levels of aggregation: products, stages, occupations and tasks.

The first level is in the reality at the bottom of the chain because it concerns the last step and the after sales services, while the last one is at the top of the chain because it regards the all elements in order to permit that the good achieve the hand of the consumer. Considering the stages and the occupation levels are intermediate and while the first regards the tasks performed by each employee, the second one concerns the collection of occupations performed together.

Regarding these latter two levels are often steps that the companies prefer to give in off-shoring rather than to focus on individual tasks[23]. An optimal incentive to this, it is given by the ICT revolution, because it creates the optimal compromise between the specialization and coordination. In fact, this revolution, has reduced the costs of specialization, but at the same time the benefits too and this because increase the standardization.

In fact the communication technology increases the possibility to transmit ideas and information quickly and cheaper, but good coordination increases the costs favouring few tasks per occupation and at the same time few occupation per stages. At the end, as Bloom in 2006 said: “A better coordination technology reduces the cost of specialization, but a better information technology reduces the benefits of specialization”[24].

Nevertheless this trade-off, it is really important to say that this revolution has increased the global aspect of trade, first of all considering that the supply chain involves or producing abroad or invest in long-term relationships and rely in broader suppliers and secondly the importance to coordinate the production of the facilities. According to the importance of the technology, I would like to remind about the Moore’s Law which predicts that in the 21st century the power of the microprocessors would reach higher levels at really low costs and this would implied an increasing global communication with the costs that, thanks to which is called as WWW (World Wide Web), will be plummeted[25].

In addition, it is fundamental to say how more depends on the policy and its ability to give an incentive to the more productive activities, reallocating the resources and creating an improvement in the average wages and employment conditions and at the same time to develop training programmes or work-experience programmes, helping to dislocates the employees in order that they can have benefit from the new job opportunity, as it is discussed below.

2.2 The advantages and disadvantages of the FDI