CO2 Emissions and Fuel Alternatives in Shipping

Info: 9247 words (37 pages) Dissertation

Published: 9th Dec 2019

CO2 Emissions and Fuel Alternatives in Shipping

The future of emissions from the scope of Alternative Fuel options adaptation

table of Contents

TABLE OF FIGURES

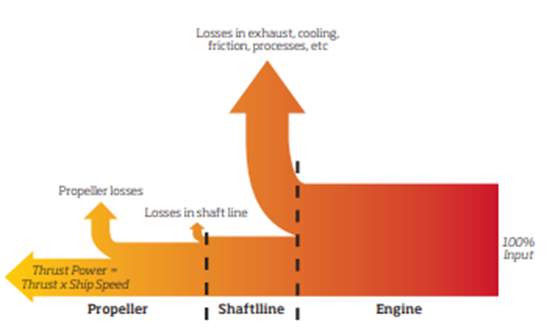

Figure 1: Typical power utilization in a tanker or bulk carrier

Figure 3: On-board hydrogen fuel system schematic

Figure 5: Eco Marine Power’s Energy Sail

Figure 6: LNG Fuelled fleet area based on AIS data from LNGi from 01.01.2018-11.01.2018

Figure 8: LNG Tank systems, source : TGE Marine Gas Engineering-Bjorn Munko, LNG 17 Houston

Figure 9: Small Scale LNG value chain (DNV-GL 2015)

Figure 10: LPG Terminals Europe

INTRODUCTION

Maritime is the business involved with the carriage of goods and people through sea all around the globe. As we know our planet is compromised mostly by water, around 71%, and people from the ancient years have used the oceans and the inland waterways as a means to move around goods and themselves. Transportation though requires thrust from most commonly an engine. This thrust produced in almost every situation nowadays comes from the burn of fossil fuel through a combustion engine.

Figure 1: Typical power utilization in a tanker or bulk carrier

The use of this is to produce energy that in its respective order is used to create a cycle of moving parts that provide thrust, and in the shipping industry specifically engines move the propellers that keep the ships going in our seas. From this combustion though we don’t always have only the much-desired production of energy. Many other biochemical constructions are released in to the atmosphere as collateral to the production of energy that can be harmful for humans and for the planet in the short run and also provide a long-term threat for the viability of our species and for the ecosystem of Earth as a whole.

One of the most important and harmful types of the side products of all engines that burn fossil fuels is CO2 or carbon dioxide. As it is widely known CO2 is a greenhouse gas that in normal conditions alongside with other types of gases are responsible for the regulation of the temperature of the Earth. This happens because those types of gases in the atmosphere are responsible for capturing the radiated heat from the sun that escapes the planet. With the artificial increase of those gases by human activity, mostly after the industrial revolution of 1700’s, the atmosphere is capturing more heat than it should to regulate the temperature and thus we observe a slow but steady temperature increase. Another largescale effect of the increase in carbon dioxide is the acidation of the oceans. This increase in the acidity has affected the life of sea organisms and if left unattended it is expected to rise even further creating un reversable damage to oceanic life. This climate change consists a devastating effect for the planet and there is increasing consciousness among global governments that measures should be taken, and regulatory framework should be implemented to avoid those catastrophic results.

In shipping specifically, the latest meeting of the International Maritime Organization in April 2018 was conducted with the purpose to discuss and create framework for the reduction of Green House Gasses (GHG) from ships by the year 2023. As it was discussed the emissions from the worldwide shipping industry accounted for almost 3% of the total anthropogenic emissions of GHG. In their research their expectations for the CO2 emission are about to grow at a rate between 50% and 250% if everything remains as is by the year 2050. The vision of the IMO is to take immediate action in order to decrease the emissions in three main stages and prevent the climate change and harm from CO2. The guiding principles of the strategy to be implemented is to provide non-discrimination and no favorable treatment as they will be ratified by MARPOL and IMO conventions. Another important aspect is the differentiation of responsibilities of the different countries as stated in the Kyoto Protocol and the Paris agreement. A straight timeline has been decided implementing three stages in the course of action to be implemented. The first one has to do with the period of 2018 to 2023 that will address short-term measures, then is the 2023-2030 period that will evaluate the short-term measures and implement what future changes should take place and third and final is the period from 2030 onwards that will officially mark the date that the measures will come in full force and GHG emissions will start reducing by the measures taken into consideration. From the main categorization of short-term measures as they were presented in the 72nd IMO committee, for the purpose of this project we will analyze the ninth and try to present possible solutions towards this scope. As it is stated those measures state “Initiate research and development activities addressing marine propulsion, alternative low-carbon and zero-carbon fuels, and innovative technologies to further enhance the energy efficiency of ships and establish an International Maritime Research Board to coordinate and oversee those R&D efforts;” Finally in term of timetable From January 2019 the IMO has initiated the data collection process with the data analysis and evaluation to take place by Autumn 2020 with phase three at Spring 2022 commencing in order to create a decision step for it to be implemented in Spring 2023.

Apart from many operational and other measures that can be undertaken to reduce the CO2 emissions produced by the shipping industry, one of the most important is the research for alternative low carbon or zero carbon fuel inputs for the ship engines. This although has to be undertaken as more of a long term project instead of a short term solution. During the last decade many researchers have undertaken the possibilities for such alternative fuel types and although the adoption of such researches needs time it is considered to be in the right direction with regards to the long term sustainability with the aforementioned measures coming in play until 2030. The most researched and mentioned alternatives for fuel consumption in the shipping industry are LNG, Biofuels, Hydrogen, LPG and other liquid or gaseous fuel options, Renewables and Nuclear Propulsion. Furthermore another incentive that could propel the movement toward the research and development of alternative fuel types for the shipping sector are the regulation to reduce the Sulphur emissions by 2020 and thus making the cleaner fuel types as more economically viable solution for the future.

Ongoing concerns for alternative fuel types does not have to do only with the fuel type and emissions reduction. There are multiple implications that must be taken under consideration in order to be adopted in the future or even to be actively researched towards that. First and probably the most important has to do with the ship storage on board and any technical solutions that have to be provided in terms of space and safety of each method. Secondly, one more implication would be the economies of scale or best the lack of it. As petroleum based fossil fuels are around us for multiple decades logistics and supply chain fundamentals have evolved to a level that can produce high economies of scale thus reducing significantly the cost for those types of fuels. As we would move toward new and unexplored alternatives cost would be higher until the point that adoption and R&D strives to a place that economies of scale can be achieved once more. Finally ongoing concerns have to be evaluated such as the longevity and the economical and financial profitability of such alternatives in the short and long run and the comparison of such alternatives in order to potentially get the most desired outcome in term of the regulations.

As it is understood to this point, those transitions and alternations are not to be considered separately or just under the scope of the regulatory framework and the emissions reduction. As in the 19th century the transition from steamships to stronger fuel engines meant a change in the whole system of shipping as an industry this transition to alternative fuel types can be regarded as such. Furthermore, shipping is not a sterilized organism and has to be regarded as in connection with general changes in the transportation such as the aviation industry and the mainland transportation.

HYDROGEN

The origins of Hydrogen as an element was discovered and separated in the late 18th century, and ever since it triggered scientists to try and take advantage of its use as a means to produce energy as it was considered produce substantial amounts during separation. Under thorough investigation many scientists have believed that through Hydrogen lies the solution for cheap and zero carbon energy production. As it believed, “due to hydrogen physical and thermodynamic properties, hydrogen-based technologies could find many applications within a decarbonized global energy system, and it is expected that hydrogen would have a key role in the near future (Winter and Nitsch, 2012; Andrews and Shabani, 2012; Barreto et. Al., 2003; Ekins, 2010). As discussed Hydrogen is a potentially considered alternative for powering ship engines in the future. This does not mean though that research and early prototyping does not exist in automotive, aviation and even in shipping.

First and foremost, it has to be stated what ship design implications the adaptation of such a technology will have in the long run. The particular and differentiated characteristics of hydrogen use as fuel for combustion engines carry a very important role in the adaption of such an alternative in the design of the ship. More specifically, the increased gravimetric energy density of the hydrogen in a liquid form allows a reduction of fuel mass in comparison with the currently used fossil fuels in the same sized ships. This might prove to be a huge benefit for ship designers since it will reduce the space needed for storage of fuel used to create propulsion and thus create higher financial benefits for adopters. Furthermore, another benefit could be seen in the increase of the speed of transit maintaining the carrying load and increasing the range. Increased transport efficiency  means a more profitable ship in comparison with the competition yielding a better economic valuation of such ship designs for cargo carriage by sea.

means a more profitable ship in comparison with the competition yielding a better economic valuation of such ship designs for cargo carriage by sea.

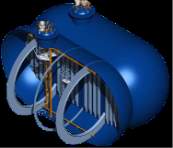

Another important consideration that has to be examined are the ship design alternations that are needed to store LH2 that is used for the combustion. Although for the purpose of this paper we do not want to dive a very technical aspect for the ship particulars there are significant hydrodynamic considerations to be researched and taken into consideration when we are talking about such modifications. Other sectors research has shown that the large fuel volumes needed for LH2 storage alternate the design schematics but in shipping it is not so evident, although it should be carefully considered. On the following figure, the on-board design of a hydrogen based fuel system of a prototype catamaran is presented as reference. In general, new ship designs would require substantial increased above water constructions to hold those storage units and therefore it could prove to be challenging to retrofit hydrogen fuel systems in existing ships.

Figure 3: On-board hydrogen fuel system schematic

A very important differentiation between conventional fuel types and hydrogen fuel systems is the very low temperature storage and the production procedure. Another important alternation between carbon fuels and hydrogen-based ones is the injection temperature of the fuel in the engine of either internal combustion ones or gas turbines. For conventional HFO a temperature increase at around 120 degrees is required to lower the viscosity of the fuel to let it pass through the injectors. Although in the case of LH2, that is a cryogenic fluid, stored in temperatures of below 20k, additional heating is required to ensure the vaporization and then pass into the combustion engine. Another less obvious but important difference is the fuel path of LH2 in comparison with HFO’s. The high concentration of different materials in the conventional fuels means that during the heating process more purification procedures are needed in comparison with LH2 that in general is a more pure and easy to manipulate type of fuel.

From the shore production of LH2 until the usage in the ship engine the liquified gas will pass many systems. Such systems consist of cryogenic storage tanks, liquid pumps and gas compressors, heat exchangers and long pipes specifically created for the transport of cryogenic gases. At this point in time the main input for an onshore production plant of LH2 is Natural Gas (NG). Although in the future other ways such as electrolysis might emerge for the production of LH2. For the use of NG to produce LH2 the production of CO2 from the plant is almost three times the mass of LH2 produced. Although this side effect of GHG produced is important on onshore production bases there is the technology and the space without the need to retrofit to capture the harmful GHG and reduce the negative effects for climate change.

As discussed above the hydrogen marine fuel systems for ships are very much capable of completely eliminating the emissions of CO2 and SO2 in the atmosphere from ships. Although the problem of those emissions is transferred to the onshore production. This can be controlled by CO2 capture filters but needs further investment and procedures to take place to achieve optimal results. The LH2 as a marine propulsion fuel itself needs large amounts of investment if it is to be adopted by the industry. Another important thing to be stated is that the burn of LH2 as a fuel produces a large amount of fresh water that can be used for the on board needs during the voyage of a ship. Safety issues and measures have to be taken into consideration and regulatory framework has to be discussed and adopted in order for such a transition to be successful.

NUCLEAR POWER

From what known at this point, power storage and generation predominantly comes from the breakage of the chemical bonds between atoms. On the other hand, nuclear power comes from the fission of large nuclei into smaller products under controlled chain reactions. With this procedure a large amount of heat is produced that in its respective order is moved to a coolant to produce power through basic thermodynamic procedures. Therefore, nuclear energy produced represents a potentially high reward alternative for marine propulsion in terms of CO2 and generally GHG emissions.

When talking about nuclear power generation, there are multiple types of fission, coolants for the reactors and types of fuels to be used in the shipping industry. Although the most common one is the Uranium pressurized water reactor. Uranium in its natural form is compromised by three different elements: U239 at 99.3%, U235 at 0.7% and U234 at 0.005%. The basic component for the production of nuclear energy is the U235 when neutrons are emitted in the process and cooled down by the coolant, in this case water, and in continuation causing further fissions in U235 atoms. The actual power is produced when the energy from the coolant is moved to another steam cycle that then generates electricity or direct shaft power. Although the percentage of U235 is almost 5% it can be enriched to be more productive, although worldwide international regulations do not allow more than 20% enrichment to avoid miss use in nuclear weaponization.

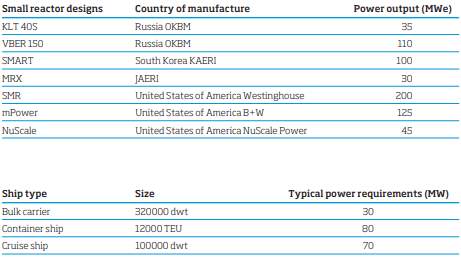

When nuclear reactors started emerging in the end of the previous century those reactors had a small MW production, although moving in the future economies of scale, specialization has payed merits and the production has been increased by much. For the use in shipping though, those reactors are far too large to be accommodated on board and by the increased demand small modular reactors are emerging. Those types of nuclear reactors are not just smaller in terms of MW production but also in size and this could mean potential use in smaller spaces such as a ship. The following graph presents small modular nuclear reactors and their power output compared with the potential needs in MW of vessel types and sizes. In the US currently, the Energy Department in co-sponsoring a program to evaluate the efficiency and financial and economic viability of such projects.

One of the most important considerations when we are considering nuclear power production is the ship design alternations and the regulatory framework that has to be very stringent. The whole procedure of the ship design and build would have to be driven entirely by safety measures in terms of operation, maintenance and decommission of the vessel. Not only the mechanical aspect of the shipbuilding would have to comply with nuclear regulations but also the electro-technical aspects and the naval architecture plans have to comply with extreme safety measure in mind. Those types of safety measure and procedures have to bring to the table all the involved parties in the process such as the builder, the flag states that vessels fly and are willing to undertake such projects, classification societies, insurance makers, the shipowner and international nuclear administration bodies. Furthermore the shipowner has to demonstrate in an independent regulator the ability to operate the ship in a safe manner and report to the International Atomic Energy Agency (IAEA) specifically adapted for marine use. The IMO and IAEA have to work together in the process to create an efficient and strict enough regulatory framework for such nuclear powered ships and assign critical control points in all the involved parties such as the ports and counties themselves. Although this would prove to be challenging because each nation has each own nuclear regulations it is absolutely crucial to be a centralized framework in order to avoid unpredictable scenarios.

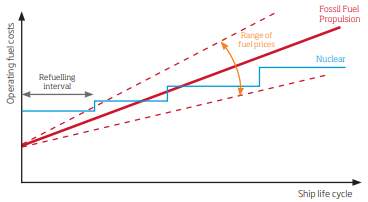

The cost of nuclear driver energy and conventional fuel types has also to be examined to provide accurate comparisons between the feasibility of such projects. Nuclear propulsion ships would require a much higher initial capital outlay for all the reasons mentioned previously the operating fuel costs show a much more competitive positioning over conventional oil type fuels as show in the graph below.

As it is to be expected because of the high oil price differentiations through the life cycle of a ship the gradient of line that present the conventional fuel costs is higher and more unpredictable than nuclear fuel costs. A move to nuclear powered ships would mean that shipowners become price takers since there would be close to zero control over the cost rates of such equipment and expertise. There are many other costs that have also to be taken into consideration, such as the port dues, through life fuel costs, pilotage costs, insurance and survey costs and most importantly maintenance.

Nuclear propulsion provides clear benefits in terms of CO2 and GHG emissions and the adaptation of naval ships and submarines has shows that also the technology is present and it is practical. Although as stated before there multiple limitations if this technology is to be applies in merchant ships. Crew and staff in general training has to take place, naval architecture of the next generation has to accumulate expertise, regulation formation has to take place and of course disposal measures have to be of extreme importance. For all those reasons this type of transition to nuclear powered merchant ships is somewhat a venture with a medium to long term horizon that needs expertise, regulations and public perception to be formed before any major changes are to adopted.

BIOFUELS

It’s a common fact that biofuels in the maritime industry are rarely used, although the global biofuel consumption is steadily increasing. However, since biofuels can replace or blend with petroleum diesel with little or no engine modifications, they are a viable alternative, leading many engine manufacturers to develop new technologies to accommodate their adoption in shipping. Indeed, according to experts, biofuels, have a large potential to combat climate change and reduce emissions over their life cycle.

Currently, a variety of ship compatible biofuels are manufactured globally, but the most widely used types of biofuel are bioethanol and biodiesel. Plant oil is another form of first generation biofuels that is mainly used for engines running on heavier diesel oil. Worth mentioning are the second generation biofuels, also called BTL process (Biomass-To-Liquid), which are produced from wastes, residues or novel feedstocks such as algae. The latter are “greener” than the first generation biofuels since they are made from sustainable feedstock. As a result, their impact on GHG emissions is much lower than that of the first generation. However, due to their underdevelopment they are not widely available for use. Another promising type of biofuel are the drop-in biofuels and they definitely show a strong potential to replace part of the fuel mix. These are liquid bio-hydrocarbons which are functionally equivalent to petroleum-derived fuels and fully compatible with existing petroleum structure. Furthermore, experts predict that in the future some sorts of wood-based products, such as pyrolysis oil and synthetic biodiesel will also be used.

MAN B&W Diesel along with Wärtislä, are the engine manufacturers with the biggest experience on biofuels and play an important role in the development of this alternative option in shipping. When using biofuels in vessels, all ship installations such as fuel storage, fuel treatment system, piping, centrifuges need to be evaluated for possible modifications. Once these modifications have taken place, a switch to biofuels is deemed rather uncomplicated (MAN B&W Diesel Press Release, 2007).

As far as the engine types are concerned, there are two main categories which can accommodate the use of biofuel. The low speed two-stroke engine and the medium speed four-stroke engine, both used as main and auxiliary engines. Low speed engines generally drive the propeller shaft directly while medium speed engines may drive the shaft via a generator/electrical motor (diesel-electric propulsion). Various investigations have proven that diesel engines which run on heavy fuel oil can also operate on vegetable oil without any malfunction, whereas engines designed for diesel or gas oil may show problems due to the higher density of the vegetable oil (MAN Diesel, 2006).

On the environmental aspect, use of biofuels not only reduces ship emissions on air quality, due to their zero sulphur content, but also it is a strong option to realize lower carbon intensity in the propulsion of ships. Although the combustion of carbon-based material will always lead to some level of emissions, biofuels can be considered as a renewable energy since the amount of CO2 that is released from their combustion has previously been taken up from the atmosphere as the plant grows, and as a result does not lead to any net increase in the concentration of CO2 in the atmosphere. Greenhouse gas emissions produced by biofuel feedstock are much lower than those produced by conventional type of fuels. However, it should be noted that some fossil-fuel energy is used when producing the raw material for biofuels. Furthermore, biofuels in 100% blends can even lead to an improved HSQE (Health, Safety, Quality, Environmental) result, in the case of spills to the marine environment due to their biodegradable nature, compared to the conventional fossil marine fuels.

On the other hand, it should be noted that biofuels face some significant obstacles as a maritime fuel replacement. Specifically, compared to petroleum-based fuels, their price is higher. First generation biofuels such as vegetable oil-based biodiesel or bioethanol from corn or sugarcane can typically compete with fossil fuels at oil prices around 60 USD/barrel. Second generation biofuels have higher production costs as they are newer and less optimized technologies. On the other hand, the taxation of fossil fuels like MDO and HFO is expected to be increased, fact which could balance out the cost gap.

Furthermore, their insufficient logistic support at ports is another issue which will likely limit them to niche applications involving smaller vessels operating in environmentally sensitive areas. In the above, we should also add the limited expertise in the handling of some biofuels, including long-term stability within the shipping sector. Shipping industry should be encouraged by outstanding examples of biofuel use, such as Maersk Group, who strive to achieve their corporate goal of reducing CO2 emissions by 60% from 2007 levels.

What is more, since most biofuels are extracted from plants and crops they will create in a way shortage of food supply and this situation will lead to a rise in food prices. A possible solution to the above could be the use of waste material from plants as a raw material. In addition, significant land areas need to be devoted to first generation biofuel production if they had to supply the whole marine market. In other words, in order to power the current worldwide fleet of merchant ships, it is estimated that it would require a land area equivalent to that of about twice the size the United Kingdom (MacKay, 2011).

The regulatory framework will also play an important role in the adoption of biofuels since the international maritime sector is currently not covered by any regulatory mandate on GHG emissions. Of course, the latest IMO convention will play a crucial role, but other measures should also assist For example, ship operators could be forced to comply with regulatory mandates and use cleaner fuels around densely populated areas. Ports of Rotterdam and Amsterdam are good examples of this effort as well as the cruise ships in Sydney harbour. Also, in countries such as the Netherlands, biofuels for both road and marine transport are considered as a part of national climate targets.

According to surveys, there is an agreement that biofuels have the potential to replace approximately 10-30% of the fossil fuels currently used. Estimates for the global biofuel production by 2020 are around 115 million tons oil equivalents. In addition, the formation of a global ECA as well as financial incentives in ports for ships that produce fewer emissions would increase the biofuel demand even further. To combat the problem of price competitiveness, biofuel production facilities should be located near major ports or bunker stations. Lastly, the key element for the successful implementation of this alternative, is the availability of marine biofuel in the long term.

RENEWABLE ENERGY

More than ever before, shipping companies are exploring mitigation measures to reduce GHG footprints through renewable energy. The motivating factor for that is the abundance of energy sources such as wind, sun, ocean waves and tides, river currents, as well as salinity and seawater temperature gradients. Renewable options can be used in ships of all sizes to provide primary, hybrid and auxiliary propulsion, as well as on-board and on-shore energy use. Renewable power production can also be exploited to produce electricity to power vessels at berth and to charge batteries for fully electric and hybrid ships and in that way contributes towards an improved energy management and fuel efficiency across the shipping sector. A wide range of innovative technologies are being developed for the marine renewable energy generation, with wind, solar and in-stream tidal energy generation facilities, being the most promising.

Several concepts and technologies have been constructed by innovative shipping companies which are expected to produce favourable environmental results using renewable resources. An outstanding example is a “Wind-Solar” ship constructed by Eco Marine (illustrated bellow), which offers both reduced GHG emissions and lower consumption levels. Also, NYK with their “Eco-Ship 2030” is planning to design a futuristic vessel which will produce zero emissions.

Figure 5: Eco Marine Power’s Energy Sail

As far as solar and wind power are concerned, one can argue that power derived from wind is free from exhaust pollutants and solar power has been demonstrated to augment auxiliary power. Furthermore, floating solar photovoltaic technologies can offer higher performance compared to land-based installations. That is because water provides better light reflection and panel cooling and consequently less shading and dust accumulation. On the other hand, the principal constraint is the ability to find a large deck surface area on the ship which does not interfere with cargo handling or other purposes for which the vessel was initially designed. In this context, car transporters are an obvious candidate for the application of such technologies.

Overtopping (reservoir) technologies, floating attenuators and point absorbers, located on shorelines, near-shore, or off-shore, are used to convert wave energy into electricity. Vertical and horizontal axis turbines on stream generators and barrage and lagoon technologies capture tidal energy, primarily in areas where the difference between low and high tide levels is maximised. New applications continue to emerge such as floating tidal installations, floating or underwater data ‘farms’ wave power for carbon capture and storage and high voltage lines connecting offshore and onshore installations.

According to surveys, the wave energy sector could potentially equal and even exceed the offshore wind sector, if we take into account that waves are a concentrated form of wind energy capable of travelling large distances with minimal losses. On the other hand, compared to other sources of renewable energy, wave energy is quite expensive. To succeed, R&D projects need to identify ways to reduce its cost and to find a suitable protection mechanism for these installations in order to survive the weather and the harsh, corrosive marine environment.

Regarding electricity for ship propulsion, energy storage devices are necessary, while they are also important for the optimization of the use of energy on board in hybrid ships. Currently, there are several energy storage technologies available. Battery powered propulsion systems are already being engineered for smaller ships, while for larger vessels, engine manufacturers have focused on hybrid battery solutions. Other energy storage technologies that can find application in shipping in the future include flywheels, supercapacitors, and thermal energy storage devices.

Significant growth in hybrid ships, such as harbour tugs, offshore service vessels, and ferries should be expected after 2020, and further applications for technology may be applied to power cranes for bulk carriers or even in ports. After 2030, improvements in energy storage technology will enable some degree of hybridization for most ships. For large deep-sea vessels, the hybrid architecture will be utilised for powering auxiliary systems, manoeuvring and port operations to reduce emissions in populated areas. Although the pace of technology is advancing at a fast pace, challenges related to safety, availability of materials used and their lifetime must be addressed to ensure that battery-driven vessels are competitive to conventional ones.

The main barriers to increased penetration of renewable energy solutions remain. Specifically, the lack of commercial viability of such systems and the existence of conflicting incentives between ship owners and operators result in limited motivation for deployment of clean energy solutions in the shipping sector. Some also argue that the electricity generation produced is not as large as that of traditional forms of energy and this effectively means that ships cannot rely solely upon renewables. Last but not least, the high capital outlay required in order to set up renewable energy generation facilities combined with their high maintenance expenses justifies why this alternative has not yet seen the recognition it deserves.

LNG & LPG FUELS

Figure 6: LNG Fuelled fleet area based on AIS data from LNGi from 01.01.2018-11.01.2018

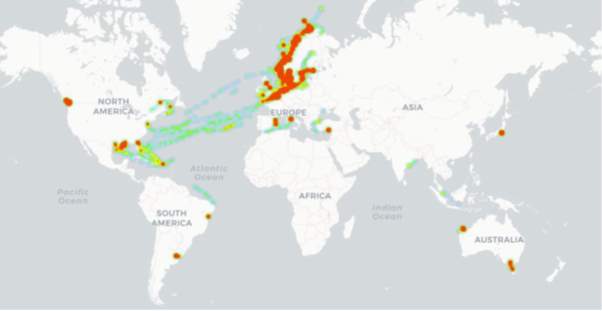

LNG’s popularity as an alternative fuel is gaining more and more momentum in the shipping industry. Not only that, infrastructure projects are planned or proposed to support this momentum. Either full-scale projects such as liquefaction facilities to big import terminals which are well established at the moment in various regions or small scale projects such as LNG distribution sources (import terminals) to support LNG Vessels as consumers. As of today, Europe is the continent with the highest LNG fuelled ships operated most of them in Norway. Currently 121 vessels are operated with LNG fuel and that number is expected to increase to 500 by 2020.

For the time being the type of vessels that use LNG as a fuel mostly are Car/Passenger ferry’s followed by Platform Supply Vessels, although the orderbook as of 1st of April 2018 indicates a major increase in Oil/Chemical Tankers and Container Ships. Moreover the majority of the vessels that are currently operating and those that are imminent to be delivered by 2020 have the option of dual fuel usage. As for the vessels that are currently powered by other means must either use more-expensive low-sulphur fuel oil (LSFO), or be fitted with an exhaust gas cleaning system, known as scrubbers, in order to continue to burn heavy fuel oil (HFO) or switch to gas or Dual-Fuel Engines.

Engine Specifications

LNG is a clear, colourless and non-toxic liquid which forms when natural gas is cooled to -162ºC. The cooling process shrinks the volume of the gas 600 times. In its liquid state, LNG will not ignite. LNG can be burned either into Lean-Burn gas engines or DF engines, although most new buildings are equipped with DF engines.

In Lean-Burn gas engines LNG is ignited by a spark plug(a device that delivers electric current from an ignition system to the combustion chamber of the engine to ignite the compressed fuel/air mixture by an electric spark).Lean-Burn gas engines are supplied with gas through a gas valve unit that filters and controls natural gas pressure .Gas engine cylinders are fed by individual pipes, which are connected to a main double wall pipe running along the engines. The mixture of air and gas contains more air than is needed leading to lower combustion temperature, resulting in lower NOx emissions and higher efficiency. (DNV-GL, 2015b, “LNG as a Ship Fuel”)

Propulsion systems using lean-burn gas engines present two applications, gas-mechanical and gas-electrical application. In gas-mechanical application, the engine provides propulsion power to the propellers via reduction gears and shaft lines, while gas-electrical provide electric power to propel the propellers.

Rolls Royce is the main producer of lean-burn gas engines and there are 2 series of engines Bergen B and C. Bergen B engines are mainly used to large ferries and Ro-Ro vessels whereas Bergen C are use to smaller ferries and Cargo vessels. The power output for the first one is from 3,500 to 7,700 kW while the latter provides output of 1,460 to 2,430 kW.

Osberg, T. G. (2008). Gas engine propulsion in ships. Retrieved from http://www.glmri.org/downloads/lngMisc/DNV-Gas Engine Propulsion in Ships (safety considerations)-Torill Grimstad Osberg- I.pdf

DF engines when working on gas mode, ignition is made through the injection of small amounts of diesel, and when they work on diesel mode they are based on the normal diesel cycle. DF engines are able to change from gas to diesel easily while the vessel is operating. The change takes less than a second and both engine load and speed remain unaffected. On the other hand, when the change is from diesel to gas, the process is slower. Diesel supply is gradually reduced while the amount of natural gas provided increases. The speed and the engine load remain unaffected as well through this process. As Lean-burn gas engines, DF engines mainly present two propulsion system layouts, DF-mechanic engines and DF-electric engines. The main producer of DF engines is Wärtsilä with engine power ranging between 0.9 to 18.3 MW. There are 4 types of engine series, from Wärtsilä20DF to Wärtsilä50DF based on their power output. The Wärtsilä50DF has the highest power output ranging from 11,700kW to 17,550kW and is used on large LNG carriers and ferries.

Lean-Burn Gas egnines comply with IMO Tier III regulations, whereas DF engines comply with IMO Tier II regulations when operating in their liquid fuel oil mode and IMO Tier III when operating in their gas mode.

LNG Fuel Tanksis where the LNG required for the voyage is stored. There are some problems regarding LNG Fuel Tanks. Firstly, LNG fuel tanks require more space in comparison with tanks used to store HFO, which are around 2.5 times bigger than HFO tanks. Secondly the temperature that LNG has to be stored is very low (-162°C) so they had to be fitted with insulation measures that increases the size as well.

Nowadays, manufactures of LNG engines have started to develop LNG storage and handling systems on board that are able to supply their engines. Those systems are designs in accordance with the International Code for the Construction Equipment of Ships Carrying Liquefied Gases in Bulk (IGC code) as well as with the IMO guidelines. There are several option regarding fuel tanks mainly based on the vessel size and the type of the engine which is the operational pressure of the engines (low-pressure engines or high-pressure engines).

Nowadays, manufactures of LNG engines have started to develop LNG storage and handling systems on board that are able to supply their engines. Those systems are designs in accordance with the International Code for the Construction Equipment of Ships Carrying Liquefied Gases in Bulk (IGC code) as well as with the IMO guidelines. There are several option regarding fuel tanks mainly based on the vessel size and the type of the engine which is the operational pressure of the engines (low-pressure engines or high-pressure engines).

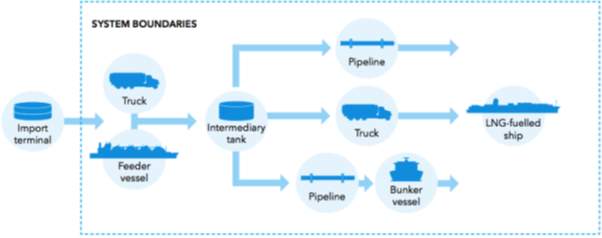

LNG maritime trade is an important segment in the global maritime trade, as for many years now LNG has been transported as a cargo by LNG carriers. From the production and liquefaction plants to import terminals and then to the local LNG pipeline grid via LNG carriers or directly through production plants, is a well establish supply chain with deep-rooted pricing mechanisms that have been proven over the last decades. On the other hand, the LNG that intend to supply LNG-fuelled vessels from export or import terminals is not as established as the transportation chain mentioned. This might change in the next years due to the air pollution regulations, and become and emerging industry.

Today, LNG infrastructure faces two major concerns. The first one is the cost required to build the facilities and in general the infrastructure to meet the safety standards and the high level of sophistication required. Second, prices of HFO used for bunkering are available on the internet ,whereas, LNG as a fuel is not at this point and differs from region to region.

What are the main requirements in order to develop LNG bunker facilities? First of all the LNG availability and feasibility. It must be near or easily approachable from an import terminal or a production plant resulting in reliable and safe logistical concepts. Secondly the legislation and regulatory framework compliance as well as the investment and taxation regime. Lastly but most importantly the public acceptance for this kind of projects followed by the assignment of personnel with exceptional knowledge and skills to the required positions.

Figure 9: Small Scale LNG value chain (DNV-GL 2015)

LNG-fueled vessels comply with the regulations that are set by the IMO. For some vessels segments though it seems to be an advantageous scenario to implement this technology both economically and environmentally. Retrofitting of existing vessels requires a high investment, as it is already mentioned, meaning that mostly new-buildings will be attractive for using LNG as marine fuel. All types of vessels are able to implement LNG, but there are some sectors that will definitely see more benefits through their operational characteristics. Some of those sectors are the vessels that operate in short sea shipping routes meaning that they spend more time inside ECAs. ECAs zones have stricter regulations but based on their operation they present more favorable Return on investment of the capital expenditures. Another sector is the coasters and local vessels that are working on a specific area doing a specific route. This would mean that the vessels even if they operate in ECAs, they could work all the time doing routes from one harbor to another without worrying about the air pollution regulations.

Fuel cost sensitivity is a factor that could affect a shipowners decision on whether to install an LNG fuel engine on their vessels. LNG fuel prices are more advantageous at this point and with addition to low OPEX and CAPEX costs the investment by provide more attractive results. This depends though on whether fuel cost are chargeable to charterers or shipowners.

Finally, vessels like cruise or passenger look for environmentally friendly values in order to boost their profiles but also other type of vessels in order to be more attractive to charterers and achieve competitive advantage over their competitors.

As it is obvious from all the above, LNG as a marine fuel is an attractive potential and technically feasible solution, mainly for new building vessels in order to comply with the IMO 2020 regulations. Not only that, but also the price is lower compared to other marine fuels, but the pricing differs from region to region. Infrastructure and mainly the lack of LNG bunkering installations is a huge question mark on how the whole market is going to adopt those projects and how attractive they are going to be as the payback period seems to be long. As of now, vessels mainly in Europe and types of Car/Passenger ferries seems to be more attractive to adopt LNG-fuelled system and more specifically using the DF engines as it was mentioned above, which provide them with the opportunity to be more flexible at the moment. The main question as of now is the emissions of CO2 as technology at this point does not decrease significantly the emission of CO2 from their combustion engines. Will that mean that the combustion engines must be replaced with alternative propulsion systems that does not emit CO2 or try to improve the existing ones in order to achieve the desirable levels? Time will tell.

The term “LPG”, Liquefied Petroleum Gas, is applied to mixtures of light hydrocarbons which can be liquefied under moderate pressure at normal temperature but are gaseous under normal atmospheric conditions.

It consist of propane, butane (normal and iso-butane), propylene and other light hydrocarbons and its chemical composition can vary.

The production of LPG is mainly from natural gas processing or from oil refining. LPG is a by-product of those processes. Over the last few years LPG production is increasing reaching similar levels to the fuel oil consumption in the marine sector. At this point, there is large network in Europe with import and export terminals and also US have developed export terminals to support the increased demand of LPG. As it can be seen by the picture below Europe has a lot of terminals that can be developed to support bunkering infrastructure in order to make LPG a viable solution as an alternative fuel.

LPG at this point is a proven engine fuel with excellent clean handling properties and low emissions. Not only that but the installation cost to run on LPG fuel is significantly lower than LNG.

LPG combustion results in lower CO2 emissions compared to oil-based fuels due to its lower carbon to hydrogen ration. Compared to natural gas emission are a bit higher, but some gas engines can suffer from methane slip, which will result in increased gas emissions. This depends on the technology of the combustion and the production. LPG meets the emission standards that were set by the IMO and seems potentially to be more eco-friendly than LNG.

In comparison with LNG as it was mentioned above is that there is a sustainable supply chain that could be developed to support the adoption of LPG as a marine fuel easily. Storage tanks are more economical making them more advantageous than LNG’s projects that were mentioned, as well as LPG tanks can be more resistant than LNG’s.

The type of engines used by LPG fuel vessels are similar to those of LNG. There are two main types again Mono-fuel engines that use solely LPG as a fuel and Dual fuel engines that have the option to use LPG and diesel. Again the main manufactures are Rolls-Royce, Wartsila and MAN.

LPG can compete financially with LNG and probably also with low sulphur fuel oil cap that was set by the IMO regulations. The technology is available for adopting LPG as a marine fuel and also the infrastructure is better that that of the LNG. Nevertheless, the development of bunkering systems remains a barrier. Safety issues must be addressed but there are similar to those of LNG. All in all, LPG seems to be an interesting opportunity for cleaner fuel for the future and it is as attractive as LNG with lower investment costs, shorter payback periods and less sensitive to fuel price scenarios.

CONCLUSION

Having analysed the main fuel alternatives which all lead to reduction of the devastating CO2 emissions, each at a different degree, it’s now worthwhile to discuss how can the shipping industry take the most of their use in the long term.

One interim solution until a viable alternative to fossil fuels is eventually found, could be Liquid Natural Gas (LNG), which is already in use today, provided that supply infrastructure can be further developed. However, experts should focus on minimizing its side effects and mainly the SO2 emissions.

Biofuels and renewable energy are strong candidates of shipping fuels in the distant future, although they require further development. Specifically, the net environmental costs including the social effects of biofuels as well as the impracticality of renewables for providing sufficient power to operate ships’ main engines should be dealt with decisiveness. Possibly, renewable energy sources could be used to meet some ancillary requirements, such as lighting on board ships.

Nuclear propulsion for merchant ships is technically possible, although safety and security implications as well as support infrastructure costs would require serious consideration(thanos)

Bibliography

Andrews, J. & Shabani, B., 2012. Re-envisioning the role of hydrogen in a sustainable energy economy. International journal of hydrogen energy, II(37 ), p. 1184–1203.

Anon., 2013. FUTURE SHIP POWERING OPTIONS ,Exploring alternative methods of ship propulsion, London: Royal Academy of Engineering.

Anon., n.d. LNG Fuelled Vessels Working Group, Tank types. [Online]

Available at: http://www.lngbunkering.org/lng/technical-solutions/tank-types

[Accessed 12 06 2018].

Barreto, L., Makihira, A. & Riahi, K., 2003. The hydrogen economy in the 21st century: a sustainable development scenario. International Journal of Hydrogen Energy , III(28), p. 267–284.

Bowyer, C. et al., 2015. Low Carbon Transport Fuel Policy, s.l.: ICCT.

Chryssakis, C., 2014. Alternative Fuels for Shipping, s.l.: DNV-GL.

Chryssakis, C., Balland, O., Tvete, H. A. & Brandsæter, A., 2014. Alternative Fuels for Shipping, s.l.: DNV-GL.

DNV-GL, 2010. he age of LNG is here. Most cost efficient solution for ECAs. Oslo, International Maritime Statistic Forum Conference.

DNV-GL, 2014. LNG as Ship Fuel : The future – today. [Online]

Available at: https://www.dnvgl.com/Images/LNG_report_2015-01_web_tcm8-13833.pdf

[Accessed 12 06 2018].

DNV-GL, 2015. LNG AS A SHIP FUEL. [Online]

Available at: https://www.dnvgl.com/publications/lpg-as-marine-fuel-95190

[Accessed 12 06 2018].

Dr. Negra, C., 2017. Marine Renewable Energy Assets and the Climate Bonds Standard, s.l.: Versant Vision LLC & CLARMONDIAL.

Ekins, P., 2010 . Hydrogen energy: economic and social challenges, s.l.: Earthscan.

Florentinus, A. et al., 2012. Potential of biofuels for shipping , Netherlands : ECOFYS Netherlands B.V..

Gilbert, P. et al., 2017. Assessment of full life-cycle air emissions of alternative shipping fuels. Journal of Cleaner Production, pp. 855-866.

Hsieh, C.-w. C. & Felby, C., 2017. Biofuels for the marine, Denmark: IEA Bioenergy.

Kantharia, R., 2017. www.marineinsight.com. [Online]

Available at: https://www.marineinsight.com/green-shipping/top-7-green-ship-concepts-using-wind-energy/

[Accessed 12 06 2018].

Lorenz Bauer, P. D., 2016. Ocean Going Vessels Going Green. [Online]

Available at: http://www.biofuelsdigest.com/bdigest/2016/11/22/ocean-going-vessels-going-green/

[Accessed 12 06 2018].

Methanol as a marine fuel – a low carbon alternative? (n.d.) Professor Karin Andersson.

Munko, B., 2017. Supply, storage and handling of LNG as ship’s fuel. [Online]

Available at: http://www.lngbunkering.org/sites/default/files/2013 TGE Supply, storage and handling of LNG as ship’s fuel.pdf

[Accessed 12 06 2018].

Opdal, O. A. & Hojem, J. F., 2007. ZERO Emission Resource Organisation. [Online]

Available at: https://www.zero.no/wp-content/uploads/2016/05/biofuels-in-ships.compressed.pdf

[Accessed 12 06 2018].

Osberg, T. G., 2008. DNV. [Online]

Available at: http://www.glmri.org/downloads/lngMisc/DNV-Gas Engine Propulsion in Ships (safety considerations)-Torill Grimstad Osberg- I.pdf

[Accessed 12 06 2018].

Rusu, E. & Onea, F., 2018. A review of the technologies for wave energy extraction, s.l.: Oxford University Press.

The World LPG associations, L. f. M. E. T. M. A. F. (., 2015. LPG for Marine Engines The Marine Alternative Fuel. [Online]

Available at: https://safety4sea.com/wp-content/uploads/2018/01/WLPG-LPG-for-marine-engines-The-marine-alternative-fuel-2018_01.pdf

[Accessed 12 06 2018].

Veldhuis, I., Richardson, R. & Stone, H., 2007. Hydrogen fuel in a marine environment. International Journal of Hydrogen Energy , XIII(32), p. 2553–2566 .

Welten, I., 2018. Commercializing Marine Biofuels, s.l.: GoodFuels – the sustainable fuel company .

Winter, C.-J. & Nitsch, J., 2012. Hydrogen as an energy carrier: technologies, systems, economy., s.l.: Springer Science & Business Media.

Cite This Work

To export a reference to this article please select a referencing stye below:

Related Services

View all

Related Content

All TagsContent relating to: "Maritime"

Maritime is something relating to the seas and oceans. The term is commonly used in nautical and seaborne trade matters. Not to be confused with “marine” which relates specifically to the seas, oceans and the life within them.

Related Articles

DMCA / Removal Request

If you are the original writer of this dissertation and no longer wish to have your work published on the UKDiss.com website then please: